Shedding light on digital banking and digital financial services

Digital banking refers to the digitization (online migration) of all traditional banking activities and programs that can previously only be availed by customers when they were physically present in a bank branch. This comprises of activities such as,

- Money Deposits, Withdrawals, and Transfers

- Checking/Saving Account Management

- Applying for Financial Products

- Loan Management

- Bill Pay

- Account Services

According to the State Bank of Pakistan (SBP), “Digital Financial Services (DFS) include a broad range of financial services accessed and delivered through digital channels. DFS can be a catalyst in improving living standards, reducing poverty, decreasing fiscal deficit, and providing equal income opportunity to all Pakistanis.”

Source: State Bank of Pakistan

Currently, financial markets are becoming more reliant on digitalization, as digitally integrated financial markets play a significant role in the development of the financial sector, increasing market competition, the performance of intermediaries, and the efficiency of their day-to-day operations.

Read more: Digital banking for a digital Pakistan

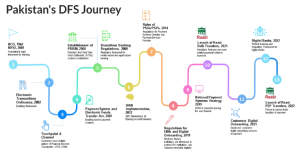

Pakistan has taken vital initiatives over time to develop and integrate a number of digital financial services systems.

Source: State Bank of Pakistan

What is Fintech?

Financial technology (Fintech) companies are reshaping the global financial services industry. FinTech enables the financial industry to serve customers in novel ways by unlocking innovation, facilitating them to provide higher quality services at lower prices.

Impact of Covid-19 on Digital Financial Services

Recent developments in Pakistan’s digital ecosystem have been remarkable. During the pandemic crisis, the significance of digitization has become more apparent; from cash transfers to telehealth, and e-learning to e-commerce, the ICT-led response assisted consumers, households, and government authorities in mitigating the socioeconomic consequences of pandemic-induced lockdowns and disruptions.

Research implies that lockdowns, resulting from the spread of COVID 19, have caused an increase in transaction volumes of FinTech. Some significant trends appeared during the year of coronavirus outbreak, both on the supply and demand sides. These include, increased digital adoption, changing user behaviors toward digital platforms, and increased regulatory focus on the Fintech sector.

Banks on their way to get digital license

Rapid transition from traditional to digital banking has encouraged banks to attain digital license from SBP. In this pursuit, central bank has received 20 applications for digital banking, but it has decided to issue only five licenses to step on the road towards digital banking.

1/2 #SBP issues Q3FY22 report on Payment Systems that shows growing digital adoption in Pakistan. Overall e-banking transactions volume grew by 2.6% whereas value by 6.5% while the overall growth was 32.7% in volume and 57.5% in value on YoY basis. pic.twitter.com/ITjzDZyCit

— SBP (@StateBank_Pak) June 16, 2022

Syed Irfan Ali, Managing Director of SBP subsidiary Deposit Protection Corporation (DPC) said, “due diligence (of banks and financial institutions which applied for the digital banking license) is underway and we will hopefully be issuing licenses pretty soon.”