All Pakistan Textile Mills Association (APTMA) Patron-In-Chief Dr. Gohar Ejaz wrote a letter to Finance Minister Ishaq Dar, highlighting the measures the government needs to take to ensure the growth of Pakistan’s export sector.

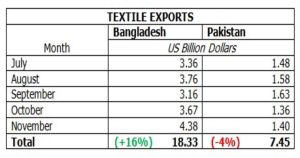

Bangladesh Readymade Garment sector exports witnessed a growth of 16 percent year on year basis by exporting RMG worth $ 18.33 billion as compared to $ 15.86 billion last year, while Pakistan’s textile sector witnessed a decrease of 4 percent in exports as compared to the same period from $ 7.76 billion to $ 7.44 billion.

Bangladesh’s significant export earnings are attributed to capitalizing on market availability, something Pakistan is not doing at the present. Currently, Pakistan’s industry is struggling with cost and production issues, which include the realized ‘value of exports’.

Increases in Pakistan textile exports (in recent years) have been wrongly attributed to a commodity price increase. On the contrary, the textile export data for the last five years showed that volumetric textile exports are the primary driver with a double-digit increase in value-added items (Annex-A). The current drop in exports is entirely volumetric.

The following issues need to be addressed for the textile sector to maintain & grow exports to contribute at par in line with capacity towards a sustainable Balance of Payments.

- Working Capital Requirement / Zero Rating

- With the withdrawal of Zero-Rating (SRO 1125) and the implementation of a 17 percent General Sales Tax (GST) on export-oriented sectors, the cost of doing business has increased to unsustainable levels as a consequence of increased working capital and the much higher interest rates.

- In FY22, the total amount retained by FBR as sales tax on domestic sales was only Rs 50 billion out of the Rs 249 billion collected. Approximately, Rs 250 billion of the industry remains with the FBR at all times as a result of this collection and refund mechanism. This indicates that 80 percent of production is being exported while only 20 percent is being consumed domestically.

- Sales tax is consumption-based, which inflates inventory and capital costs, serving as an impediment to new projects and expansion of exports as capital cost increases by 20 percent and refund can only happen after commercial operations.

- Because of the high rate of sales tax, trade volumes outside the Sales Tax System have expanded, resulting in smuggling, outright fraud, and the import of used clothing into the country. Pakistan is among the top importers of used clothing.

- When collecting sales tax on domestic sales, it should be deducted at the Point of Sale. This will subject any product sold domestically from any source to a 17 percent sales tax, including smuggled goods (ANNEX-B).

Under these circumstances, APTMA requested the immediate restoration of SRO 1125 i.e., Zero Rating for the entire textile value chain in order to make available working capital.

Read more: APTMA raises alarm over textile sector shutting down

- Gas Priority for Export Sector

- Pakistan’s favoring of domestic over industrial consumption is a classic case of prioritizing short-term consumer satisfaction over long-term economic stability. Subsequently, the present allocation of gas resources is highly unsustainable for the economy in the long term.

- In order to ensure sustainable gas supply and competitiveness, the priority of gas supplied to different sectors of the economy should be reviewed in a way that productive sectors of the economy that add more value to GDP be given preferential priority in domestic gas allocation and supply. That means allotting first priority of gas supply to the industry including captive power ahead of the domestic sector and creating a two-tier allocation for the industry in which export-based industry should be given preference.

- The economic benefits of prioritizing the export sector in the first place will comprise of enhanced exports, boost competitiveness, job creation and have a multiplier effect on the value chain.

A change in gas allocation priority is requested.

- Pricing Reforms in the Gas Sector (WACOG)

- The export sector in Punjab is being provided gas at $9/MMBtu even under the RCET, while households’ basic tariff was $1 and about $2 on average per MMBtu. Similarly, gas prices for fertilizer start from $1/MMBtu, signaling a non-transparent and inefficient subsidy to the agriculture sector.

- Gas/RLNG being supplied to Punjab is priced at 9$ for less than 50% of the average consumption of mills last year. This formula irrationally excludes the new plants/expansion that has been made during the last 2 years. The Gas/RLNG being supplied to mills in Punjab is less than 1/3 of the required quantity of 200 MMCFD. At present gas supply to Sindh, the export industry is supplied at $ 3.75/ MMBTU (Rs 840) and at a quantity meeting 80% plus requirements. This is contrary to the commitment that the differential in gas / RLNG pricing within the country will be less than 2 $ to keep the Punjab industry competitive. This huge differential means that the Punjab-based industry is paying for gas at 9 $ and electricity at 20 Rs. /kwh while the bulk of Sindh industry is generating their own electricity at 4 cents / kwh.

Read more: APTMA rejects asking govt. to lift ban on Indian cotton import

This kind of differential and encouragement of non-productive use of a scarce commodity must be curtailed, and the government must make the much-needed pricing reforms in the gas sector, through a weighted average cost of gas (WACOG) and pricing reflecting the true economic value addition through the gas.

- Refund of Detention and Demurrage Charges

- Textile Mills are facing difficulties since banks are not clearing import documents and the Collector Customs is refusing to waive port detention and demurrage charges.

- The industry had already purchased raw materials at higher rates, and the imposition of nearly 40% demurrage and detention charges as the delays are long and have rendered the industry uncompetitive.

- These are charges incurred/paid by importers due to a lack of dollars in the country that is not the importer’s fault. So far, the total cost of demurrage and detention is almost Rs 1.5 billion (ANNEX-C).

- Furthermore, shipping companies will receive payment for demurrage in US dollars which will reduce the number of already shrinking dollars on hand.

The demurrage and detention charges as a consequence of the non-availability of forex may be refunded from Export Development Fund (EDF).

- Cash Against Documents

- The import issue is not only pertinent to chapters 84 and 85, but also to imports of raw material through cash against documents. The issue of raw material clearance subject to cash against documents remains unresolved due to the non-availability of forex and there is no other procedure in place to release the raw material from ports.

- Mills are currently unable to obtain cash against documentation and are closing owing to a shortage of raw materials.

Instruction to banks to make available forex for cotton and other raw materials as first priority.

Read more: APTMA seeks govt. attention towards issues facing Pakistan’s textile industry

- Provision of RCETs for Industrial Estates (LIEDA, FIEDMC, and SUNDAR)

- This refers to the lengthy correspondence on the issue whereby LIEDA, FIEDMC, and Sundar Industrial Estates-based industries were denied the concessional power tariffs previously allowed by the ECC and Cabinet over the last 3 years (ANNEX-D).

- Despite a multitude of meetings, letters, and commitments, the issue is still pending and the export industries are suffering from a huge financial burden. We have taken this matter up many times with the Ministry of Energy and related stakeholders and it is unfortunate that it has not been resolved yet.

This issue has been delayed for quite some time causing great financial hardship to our members who are eligible for EOU power rates since 2019. It is requested to resolve this long pending issue as early as possible.

- Extension in Submission of Duty Drawback Claims for FY21

- Many of our members, as well as other associations such as the Towel Manufacturers Association, the Pakistan Knitwear, and Sweater Exporters Association, Pakistan Textile Exporters Association, and the Pakistan Hosiery Manufacturer Association, have contacted us since a huge number of manufacturers failed to submit their Duty Drawback claims by the deadline due to delays in collation and availability of documents. Each year, the government has extended this deadline for filing claims due to procedural and documentation issues (ANNEX-E).

An extension in the claims submission date is requested so that all claims may be processed for ease in the liquidity position of exporters.

- TUF Refunds

- Many of our members have already been waiting for TUF refunds for almost a decade. Most of our members have also submitted bank guarantees as per the procedure. Bank guarantees have been submitted for the past 1 to 2 years, but mills have yet to receive the TUF refund, so their bank guarantees and liquidity are tied up as a result.

- They are incurring additional costs in order to keep the records and communicate with the relevant authorities, while the value of the claim, which was due 10 years ago, has decreased by half (ANNEX-F).

TUF Refunds may be released so that the liquidity position of exporters may be eased.

Read more: Bold steps needed to achieve IMF targets: APTMA Chief’s advice to PM Shehbaz

- Long Term Financing Facility (LTFF)

- SBP has not yet approved the limit for the Banks and the Banks have categorically refused any indication for approval of LTFF limits, thereby, forcing the customers to retire their L/Cs for machineries at a prohibitively expensive rate as the mark-up allowed may render the projects unfeasible (ANNEX-G).

- The tremendous goodwill and investment crystallized due to Temporary Economic Refinance Facility (TERF) and LTFF. Other favorable governmental policies will be dissipated if this practice is not followed.

Approval of these facilities, at least for projects for which banks have already signed financing agreements with their customers, is sought as soon as possible in order to resolve this issue and continue the drive toward export-led growth.