Gohar Ejaz, Shahid Sattar and Eman Ahmed

The majority of people in developing economies do not have bank accounts, creating an inequitable economic world that impacts the individual’s social and economic well-being (Donner and Tellez, 2008; Duncombe and Boateng, 2009). Financial inclusion in Pakistan is rudimentary compared to other countries that follow export-led growth models. The country’s regional competitors have performed better in most areas pertaining to access to finance.

Pakistan, a developing country with a population exceeding 220 million, boasts a high mobile phone penetration of 73% (Pakistan Economic Survey, 2014/15). However, 88% of the total population is unbanked and financially marginalized, out of which 63% of the population resides in rural communities (World Bank, 2014). There is a consensus amongst policy-makers to increase financial access through financially inclusive banking practices (Anwar, 2013).

Understanding the matter better

In addition to financial exclusion, there are other roadblocks to entrepreneurship and innovation that need to be mitigated so that we can empower our youth and our disenfranchised talent to bring about a grassroots level economic revolution. We must rid our policymaking of the economic formula whereby interest rates are raised in order to stabilize the economy, as this can only be effective in certain Highly Developed Economies: a title which Pakistan’s economy is a long way off from attaining.

HDEs tend to have surplus currency tied up in mortgages or consumer financing. Therefore, it is only logical that such a formula be limited in its application to those economies which are in a similar state, while a policy more suited to developing economies should be used in Pakistan’s case. The best mechanism is through supply-side interventions, bringing more individuals into the economy and increasing the labor supply – for which entrepreneurship and financial inclusion is critical.

Read more: Effective Energy Allocation for Export Growth

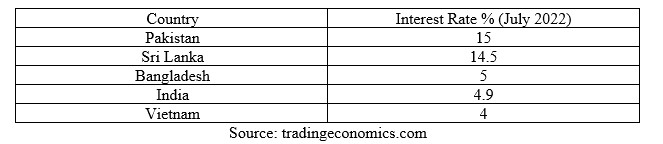

High interest rates belie the impression of a stable economy in the short run, while long-term economic health continues to be endangered due to the volatile nature of an economy with an interest rate as high as 15%. Furthermore, high interest rates not only curtail investment, but also make it virtually impossible for the concerned industries to remain profitable. The spike in interest rates has all but put a complete stop to investment, upgradation and technological advancement in various industries. Pakistan’s interest rate is now the highest in the region – even higher than that of Sri Lanka, which is reeling from a default on its debt.

Subsequently, the low level of investment has worsened the state of affairs, particularly for productive sectors which are now struggling to maintain productivity and. The abrupt rise in factory shutdowns and closing of textile businesses are causes for concern. The cost of doing business increases indefinitely with the rise in interest rate, which also implies hindrances in access to capital, leaving businesses to fend for themselves and struggle to make ends meet with no fallback option. Investors are also less likely to put money into active projects as the high interest makes these options volatile and high-risk.

All these factors result in a spillover effect with mass downsizing, stifled economic activity and stagnation in GDP growth. Thus, it comes as no surprise that technological advancement is rendered a distant fantasy for an industry facing an economic crisis.

A more adaptive financial model and a focus on more productive capital investments, particularly in technology, will have a wide, far-reaching impact that will bear fruits for generations to come. It will allow for a much-needed increase in our presently abysmal level of exports, and will also tackle the increasing burden of unemployment at the root.

Read more: Pakistan’s balance of payments crisis to worsen: APTMA warns

When a bank account is opened, it’s a step towards joining the economic mainstream. It is a sustainable mechanism to fast-track grassroots entrepreneurship, innovation and economic stimulus from the bottom up. With financial inclusion as the ultimate goal, Pakistan’s government should follow in the footsteps of Modi’s PMJDY, whereby the State Bank of Pakistan opens up accounts with a pre-approved overdraft facility of PKR 10,000 that can be used as seed money for entrepreneurship. It is proposed that the State Bank may also provide overdraft facility and debt moratorium for those unable to repay the loan in time.

In order for Pakistanis to be eligible for this scheme they must currently have no bank account. The only document required to be presented when opening the account should be the individual’s CNIC, verifiable through NADRA biometric. As for cases of overdraft, interest can be charged on the PKR 10,000 amount. However, in case of default, the government should step in to cover the amount. If this scheme is successful, an estimated 50 million accounts will be opened, with a potential disbursement of PKR 500 billion. The current scenario wherein charges are applied to accounts with balances below a certain minimum is detrimental to efforts for financial inclusion, so this scheme will be free of any such charges.

Investing PKR 500 billion into the people of Pakistan who are currently unbanked and at the lowest rung of the economic ladder, is bound to have a multiplier effect on the economy, simultaneously enhancing opportunities for employment, entrepreneurship, value addition, education, gender parity and effective resource allocation for economic growth – enabling a sustainable exit from the path of recession upon which the country is currently treading.

Read more: Removing structural inefficiencies in Pakistan

The impetus behind this proposal is the success of India’s revolutionary banking scheme, which continues to improve financial inclusion even now. In 2014 Indian Prime Minister Narendra Modi launched a plan to provide a bank account for every household, in a landmark initiative to help the poor. (BBC) Pradhan Mantri Jan-Dhan Yojana (PMJDY) is India’s National Mission for Financial Inclusion to ensure access to financial services, namely, a basic savings & deposit account, to access remittance, credit, insurance, pension in an affordable manner.

Under the scheme, a basic savings bank deposit account can be opened in any bank branch by persons not having any other account. Under the banking scheme, account holders receive a debit card and accident insurance cover of up to 100,000 rupees ($1,654; £996). They also get an overdraft facility of up to 5,000 Indian rupees.

Benefits under PMJDY:

- One basic savings bank account is opened for unbanked person.

- There is no requirement to maintain any minimum balance in PMJDY accounts.

- Interest is earned on the deposit in PMJDY accounts.

- Rupay Debit card is provided to PMJDY account holder.

- Accident Insurance Cover of Rs.1 lac (enhanced to Rs. 2 lac to new PMJDY accounts opened after 28.8.2018) is available with RuPay card issued to the PMJDY account holders.

- An overdraft (OD) facility up to Rs. 10,000 to eligible account holders is available.

As per latest government data, PMJDY now has 42.89 crore beneficiaries (basic bank account holders) with ₹1,43,834 crores total balance. More than half of the beneficiaries are women (23.76 crore) while 28.57 crore are from rural and semi urban areas.

Read more: Free market mechanism will boost Pakistan’s economy: APTMA

A senior official of State Bank of India said the average balance in the accounts which is hovering around ₹3,000-3,500 across banks is ‘an indication’ that the scheme has now become a channel for savings for the low income families. The Global Findex data base of the World Bank has also shown ‘substantial’ increase in financial inclusion in the country after 2014. As per the index, 80 per cent of people above 15 years of age in the lower-middle income group have a bank account now compared to 53 per cent in 2014.

Morawczynski et al. (2010) argues that financial inclusion success should not only be limited to the withdrawal of payments from bank accounts. The term should also incorporate the usage of accounts for undertaking economic activities. Therefore, ‘full financial inclusion’ entails participating in a wide spectrum of financial transactions, such as depositing savings, accessing credit/insurance and making payments in the banking sector (Ehrbeck, 2011; Bold, Porteous and Rotman, 2012).

Meanwhile in Pakistan, penetration in the financial sector is extremely low, with only 2.4% of the population having access to credit from formal financial sources. Out of the total adult population of Pakistan, the financially excluded population make up 53%.

Although financial inclusion is usually categorized as access to formal financial services, in developing countries including Pakistan, a significant proportion of people prefer and have access to informal finance. Informal access can occur through the organized sector (though committees, shopkeepers, moneylenders etc), or through friends and family. An estimated 19 percent have voluntarily excluded themselves through lack of understanding or need, due to preference, poverty or religious reasons.

Read more: APTMA Chairman dubs PTI’s ousting as cruel

BISP holds the largest database of underprivileged families in Pakistan – recorded by the National Database and Registration Authority (NADRA) after conducting the largest and first ever door-to-door poverty survey. Since we seek to propose a similar scheme, it is important to analyze the benefits and constraints of BISP so that we are able to utilize an upgraded version of a tried and tested model for Pakistan.

Dr. Atika Kemal’s research paper, titled “Mobile Banking in the Government-to-Person Payment Sector for Financial Inclusion in Pakistan” provides a comprehensive framework for us to develop a new and improved model based on an understanding of the impacts of BISP.

The poverty score card survey assisted BISP in identifying 7.7 million households categorized as the ‘poorest of the poor’ (BISP Report, 2014). Primarily funded by the Government of Pakistan, BISP disbursements crossed PKR. 70 billion (USD $667,908,500) by 2015. It continues to receive unprecedented financial and technical support from multilateral and bilateral donor agencies such as the World Bank and DFID as well (BISP Report, 2014).

Known for being the country’s main safety net program, BISP provides transfers of Pakistani Rupees (PKR) 26000 per person annually (approximately $113/year) that are received by around 5.3 million women from low-income households.

Many governments in developing countries have set financial inclusion as a fundamental policy goal, in digitizing G2P flows (Bold, Porteous and Rotman, 2012). A case study of the BISP in Pakistan showcased that transparency in delivering G2P payments was the primary objective for digitizing BISP payments, while financial inclusion was a secondary goal.

Therefore, digital innovation is not always the perfect solution or ‘silver bullet’ for development.’ Incentivizing the disenfranchised segments to open bank accounts and enter the formal economic system, thereby boosting entrepreneurship is a sustainable mechanism to enable an uplift to the economy.

Read more: Textile sector’s gas suspension to cause $1B loss: APTMA

The need for a long-term policy featuring lower interest rates cannot be underestimated, and its implications for a brighter economic future which generates foreign currency, jobs and international recognition cannot be denied. We need more investments in Pakistan, alongside holistic policy reforms that lend confidence to investors and the markets. This need cannot be met with an interest rate of 15%.

Mr. Gohar Ejaz has served as Chairman of All Pakistan Textile Mills Association (APTMA), elected unopposed in the year 2010-2011, the premier textile industry association of the country. He is the Chief Executive of “Ejaz Group Of Companies” comprising Ejaz Spinning Mills and Ejaz Textile Mills Limited. Mr. Gohar Ejaz was awarded Hilal-e-Imtiaz, in the year 2011, the highest civilian award. Moreover, he was recently conferred with an Honourary Doctorate from the University of Punjab.

Mr. Shahid Sattar, now Executive Director & Secretary General of All Pakistan Textile Mills Association (APTMA), has previously served as Member Planning Commission of Pakistan and an advisor to the Ministry of Finance, Ministry of Petroleum, Ministry of Water & Power.

Eman Ahmed is a Research Analyst at APTMA.

The views expressed by the writers do not necessarily represent Global Village Space’s editorial policy