Written by Shahid Sattar and Sarim Karim

Following the Information and Communications Technology (ICT) revolution of the 1990s, the international economy entered a second phase of globalization. Characterized by the offshoring of different elements of the production process, otherwise known as the Global Value Chain (GVC). The trend for developing countries within the GVC world has been to compete as suppliers within the production chain, usually at the lower value-added segments. Developing countries engage in fierce price-based competition to gain a ‘slice of the pie’ within the textile chain.

However, the GVC world has also ushered in new patterns of development. Specifically, it has changed the incentives for development from ‘deep’ industrialization to ‘shallow.’ This means that creating entire industries (deep industrialization) is no longer preferable compared to slotting into specific segments of the fragmented value chain (shallow industrialization). With this new dynamic arise two observable trends for industrialization within developing countries. These processes are stalled by industrialization and the looming threat of premature deindustrialization. This means that the social and economic gains from manufacturing-led development are exhausted earlier than precedent, leaving developing nations in a stunted growth bracket.

Read more: Is Pakistan moving towards a dollarized economy

Pakistan has experienced only limited industrialization, with its major obstacles being resource constraints, especially in energy supply, a distortive regulatory environment, and restricted export orientation. Before Pakistan can enter the virtuous cycle of industrialized development, premature deindustrialization is already a material concern. Since 1990, Pakistan’s economy has become inward-oriented, with exports’ share of GDP falling from 16% to 10% between 1990 and 2020 (World Bank, 2022). Complex and cascading import duties stifle growth, as firms lack competitive incentives to increase efficiency.

These duties also prevent better intermediate inputs from entering the economy, hindering partial factor productivity growth. Though the situation seems dire, Pakistan has the potential to reverse this pessimistic outlook. The World Bank estimates that Pakistan ought to be able to quadruple its export value. The role of the textile sector is particularly instrumental. Textile exports represent 60.81% of all exports, the sector recorded the largest trade surplus in 2021, and textile products (knitted and unknitted) made up Pakistan’s second and third fastest-growing exports in the same year (PBS, 2023). Pakistan’s 26% expansion during FY2022 in overall exports is significantly due to textile exports. Therefore, for Pakistan to shirk the specter of deindustrialization, export-led growth through investment in textiles guarantees the most gainful use of resources.

The General Trend of Deindustrialization

The phenomena of stalled industrialization and premature deindustrialization occur when the manufacturing sector begins to stagnate at lower levels of either relative employment shares, value-added shares, or per capita income shares following a peak. As this happens, the development potential of manufacturing to generate employment, growth, and investment is exhausted prematurely. In response to a stagnant or contracting manufacturing sector, urban labour shifts to either services or informal manufacturing.

This creates a bloated service sector, which experiences depressed wages and increasing income inequality between high-skilled and low-skilled labour. Those segments of the working population that cannot find urban employment, may move back to agriculture or fall into poverty. The long term outcome of these processes result in increased income inequality, decreased manufacturing output, and the loss of the ability to compete in export markets. These risks become especially likely given unstrategic and distorting regulatory environments.

Read more: Sustainable water management in Pakistan’s textile industry

Manufacturing output as a percentage of GDP has been falling since its peak of 15.71% in 1994, as shown in the graph below (World Bank, 2023). In the last twenty years, Pakistan has experienced meager manufacturing growth of 10.22% in 2000 to 11.91% in 2022. Pakistan’s industrial production index growth rate has been stagnant at approximately 4.2% since 1998, with only a sharp decrease and corresponding increase during and after the COVID-19 pandemic (CEIC Data, 2022). Moreover, GDP from manufacturing is approximately half of the GDP from agriculture, and approximately one-fifth of the GDP from services (State Bank of Pakistan, 2022).

This composition is worrying, as manufacturing is historically the engine of development due to its potential for productivity gains, capital accumulation, and value-added production. The path to development must involve a sectoral shift from the relatively less productive agricultural sector, towards the more productive manufacturing sector. Pakistan’s shift has been incomplete, and the evidence is clear given the aforementioned shares of GDP per sector. This untimely exhaustion of manufacturing growth has also meant the premature growth of the service sector and the informal economy.

SMEs and the informal economy are characterized as an ‘in-between’ sector in development literature. This refers to their low productivity, higher inequality, and limited avenues for technological change (Sumner, 2018). While quantifying variables in the informal sector is difficult, it is estimated that SMEs and the informal sector comprise 72% of manufacturing in Pakistan (SMEDA, 2022). World Bank observations show that firms in the formal economy only account for 13% of value-added (2022). SMEs and the informal sector also dominate in employment shares. Manufacturing SMEs and informal producers have 90.27% of shares in total manufacturing employment (SMEDA, 2022).

The rise of the manufacturing SME, especially in textiles, takes place simultaneously with the decline of formal manufacturing. The informal sector and SMEs are acting as a sponge for unemployed labour. However such conditions cannot be a viable driver of industrialization. Firstly, the informal sector has limited capacity for economies of scale, due to its limitations in size, dispersed production, and lack of leverage to extract higher returns from trans-national corporations. This results in limited investment confidence, which is evidenced by the State Bank’s regulations for SME financing being limited to medium-scale financing and risk management (2021).

Secondly, SMEs and the informal sector are generally oriented towards the domestic market. This can be helpful during stages of transition, where a nation intending to orient production towards exports can utilize the informal and small economy to fulfill domestic demand. However, while Pakistan’s SMEs have a 30% share of total exports, upwards of 80% of those exports are low-value added (SMEDA, 2022). Therefore, there are limited returns especially compared to formal manufacturing.

Read more: Barriers to renewable energy transition for Pakistan’s textile industry

The above analysis can be granulated to capture the trend in Punjab

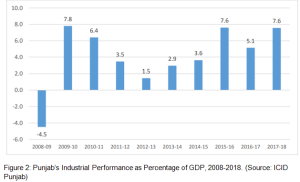

The province has a smaller share of large-scale manufacturing (8.1%) compared to the national average (10.8%). Large-scale manufacturing’s share in value-added for Punjab is even smaller, averaging at 51% while the national average is 80%. Simultaneously, SMEs have a larger share of GDP contribution at 3.4% while the national average is only 1.9%. The inconsistent overall industrial performance of Punjab over the last 15 years is the greatest cause for concern. Punjab has been unable to maintain consistent growth over consecutive fiscal years, and declined following a peak of 7.8% of GDP (ICID, 2018).

Notably, the years Punjab has seen growth have been during export-led growth in textiles coinciding with sufficient energy provision. This fact will be returned to later. To summarize, Punjab represents a microcosm of the overall trend for development in Pakistan. Given the precarity of industrial performance in the province, Punjab is especially vulnerable to irresponsible government policy but also stands with the most to gain from industrialization.

Another avenue to observe Pakistan’s development has been long term productivity gains. According to the World Bank, Pakistani firms do not capture productivity gains as they mature. Advances in productivity have slowed particularly in the post-1990 period (World Bank, 2022). State investments in R&D have fallen from 0.32% of GDP to 0.28% of GDP, and national and domestic savings are declining as a share of GDP. Pakistan is exhibiting signs of stalled industrialization.

The current response and simultaneous driver of this process has been early tertiarization, wherein the service sector and informal economy enlarge to act as sponges to absorb the large surplus of urban labour that is unable to find work. The service sector is a highly polarized labour market, which is driving inequality between the small segment of high-skilled labour and larger segment of low skilled labour (Sumner, 2018). The large amount of surplus labour stagnates wages, and distorts capital use efficiency. In order to prevent a downturn towards premature deindustrialization, a revamping of policy and development strategy is necessary.

Export-Led Growth

Export-Led Growth

Within this context, the fate of the textile industry is consequential to the overall outlook of Pakistan. Textiles comprise the nation’s largest export (60.81%), its largest source of employment in manufacturing (40% share in employment), and have the highest weight of 20.91 in the quantum index of manufacturing (Finance Ministry, 2022). This means that the performance of textiles has the greatest impact on the overall performance of the large-scale manufacturing sector. However, the size and share of the textile sector in GDP is shrinking, and has consistently been shrinking post-1990.

In 2020, textiles’ share of GDP was only 1.8%. Gains in investment, productivity, and production within the textile sector is highly elastic to consistent, motivating government policy. Therefore, regulatory decisions that reduce the capacity for textiles to remain competitive in the highly competitive GVC world threatens the long-term development trajectory of Pakistan.

High tariffs on imports limit the capacity of the sector to attain better quality intermediate inputs. Inconsistent export promotion schemes, and the lack of long-term financing, prevent investments into capacity expansion. The incentives for diversification, especially into value-added or niche products, is also hampered due to export incentives being allocated towards ‘traditional’ goods (World Bank, 2022). The exclusion of indirect exporters from financing and promotion schemes also hinders development of backward linkages within the value chain. One of the largest contributors to declining textile competitiveness has been energy cost.

Read more: Inclusive and green pathways crucial for Pakistan’s industrial progress

Across all provinces, energy comprises the largest conversion cost in the sector. The reversal of the regionally competitive energy tariff (RCET) has thus been particularly detrimental. It has created unevenness amongst producers provincially, as Punjab pays higher costs for energy than Sindh. And has undone the progress in employment, investment, and capacity growth witnessed upon its introduction in 2018. Conversely, its removal makes downstream sectors regionally uncompetitive and upstream sectors lose their price rankings (Hussein, 2021). Given the level of price-based competition within the region, especially from Bangladesh and Vietnam, such a loss is untenable.

As previously mentioned, textiles have the largest weight in the quantum index of manufacturing. Implying that stagnation in textile growth can have externalities for the industrial sector as a whole. This is visible given that textiles have the longest production chain of any industry in Pakistan, and also the greatest potential for value addition at each step in the chain. Textiles also support numerous ancillary industries, from cotton to ready made garments. Therefore, the potential for deep industrialization and the ability to capture competitive advantage in higher value added segments of GVCs is achievable through the textile sector. Conversely, if the current policy regime continues, reversal in textile sector growth will lead to a loss of gains in development.

Pakistan is currently experiencing a difficult paradigm. Responsible economic decisions have allowed activist states such as South Korea and the East Asian Tigers to direct the initial growth spurt attained from GVCs towards investments in value-added production, industrial expansion, and sustainable growth. If Pakistan does not engage or incentivize the similar capacity building, it cannot make tangible gains towards sustained industrialization. Instead, the nation is edging closer to a perennially unsustainable balance of payments crisis, and the pitfall of deindustrialization.

Mr. Shahid Sattar, now Executive Director & Secretary General of All Pakistan Textile Mills Association (APTMA), has previously served as a Member Planning Commission of Pakistan and an advisor to the Ministry of Finance, Ministry of Petroleum, and Ministry of Water & Power.

Sarim Karim is currently an internee researcher at APTMA, with a bachelor’s dual degree in Economics and International Relations from Hobart and William Smith Colleges.

The views expressed by the writers do not necessarily represent Global Village Space’s editorial policy.