Arsalan Ahmed & Ali H. Zaidi |

48 days to IMO-2020 & the clock is ticking… Refineries should brace for impact!

A Major International Event for Refineries

While Pakistan still reels from the domestically brewed crisis of Furnace Oil (FO) based power generation, there is yet another story that could be devastating for FO. This time however, the dark clouds have risen in the form of a change in international regulations sparked by a drive for environmental sustainability, something that Pakistan cannot reasonably avoid. Earlier in Mar-2018, the International Maritime Organisation (IMO) decided that the marine sector will have to reduce sulphur emissions from the then applicable 3.5% cap to a maximum of 0.5% by Jan-2020. It is expected that the regulation, now widely known as IMO-2020, will result in the largest reduction in the sulphur content of a transportation fuel undertaken at one time. This is only possible by way of installing scrubbers or by shifting from heavier fuels such as High Sulphur Furnace Oil (HSFO) to Very Low Sulphur Furnace Oil (VLSFO). Non-compliance with IMO-2020 requirements could result in serious repercussion such as the ship being detained at port, penalties and being required to obtain compliant fuel.

With consumption levels of FO around the 3.8 million bpd mark in 2017, the marine sector alone generated half of global demand, as per Forbes. The International Energy Agency (IEA) estimates that demand for HSFO will drop from 3.5 million bpd to 1.4 million bpd in 2020. Needless to say, IMO-2020 has the potential to be highly disruptive for the pricing and availability of compliant fuels.

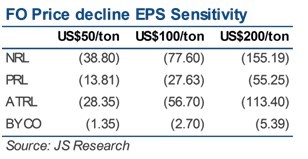

A fall of US$50/ton in prices of Furnace Oil results in a ~Rs27bn loss to the refining sector, keeping other margins constant

FO Prices Barrelling Towards an Abyss

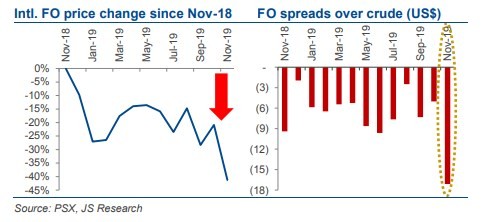

Following the implementation of the regulation from January 1st, 2020, FO prices in the international market (and by extension in Pakistan) are expected to plunge as a significant portion of its demand virtually evaporates on new-year’s eve. And the impact has already become visible: domestic prices of FO have fallen by~33% MoM in Nov-2019. It should be noted that FO is already a negative margin product (GRMs have averaged at -US$6.4/bbl in CYTD) and after this change, the margin is expected to worsen significantly. It should be noted that refinery margins FYTD have been relatively better as these had improved owing to the widespread refinery turnaround ahead of the IMO-2020 deadline. However, these are expected to cool off post Jan-2020.

By Failing to Prepare, You Are Preparing to Fail

While refineries across the globe have been adapting to the changing regulations, Pakistan’s refineries continue to operate on the out-dated hydro- skimming technology which could pose serious challenges in the wake of IMO-2020. We feel it pertinent to point out that not too long ago, on the direction of the government, the sector invested billions of Rupees in Diesel Desulphurisation and Isomerisation projects. Now, with the new regulations, the only viable solution is to again invest humungous sums just to survive in the evolving industry dynamics. So do we take this to be just another day in the capital intensive industry or a massive failure in planning?

Read more: Renewable energy: JS bank partners with Hadron Solar

As far as funding for the requisite investment is concerned, looking towards the government would be a dead-end street considering the on-going fiscal challenges. For instance, a cracker unit requires not only 3-4 years but a massive investment of US$500-600mn for a 50k bpd refinery. To give perspective, this amount is even larger than the upcoming tranche from the IMF. That said, the sector will have to find its own route. In this regard, Pakistan Refinery Limited (PRL) has plans to invest nearly US$1bn in a deep-conversion refinery. The best that the sector can expect and reasonably demand from the government is incentives on the installation of cracker units. Even if work starts today, by the time these units come online, larger and more advanced refineries with a combined capacity of 1.1mn bpd (as per media reports) that are already in the pipeline may be operational. It should be noted that the sector currently has a capacity of 0.4mn bpd.

To Make Matters Worse…

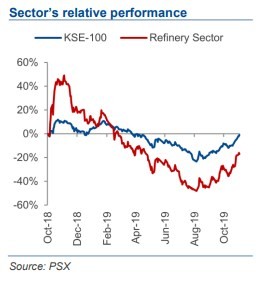

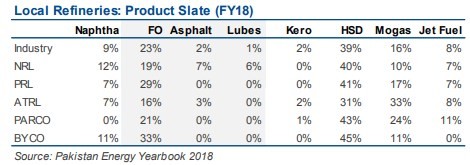

A glance at the product mix of the local refineries reveals that FO constitutes about 23% of the aggregate. The fall in FO prices will trickle down on other products, such as Asphalt and Lubes, to which FO is a raw material. In this case, National Refinery Limited (NRL) is expected to take the biggest hit considering its product mix which comprises of 19% FO, 7% Asphalt and 6% Lubes. In terms of market performance, even if we assume that the considerable correction in the oil refining stock prices in recent years reflects the impact of the regulation, the actual impact on earnings is yet to be seen.

Other Considerations

- The spread between light crude and heavy crude will naturally rise as refineries across the globe flock towards obtaining lighter crude. The impact of this increased demand for lighter crude has already started to translate into the spreads. Bloomberg has reported that Arab Extra Light premium over Arab Heavy ballooned to US$4.65/bbl for Asia for Dec-2019 from US$1.05/bbl in Sep-2019.

- The increased fuel costs are likely to translate into higher freight charges. In such a scenario, imports will become slightly more expensive for businesses using imported raw materials. This may lead to inflationary

- Coming back to the issue at hand, what will be the outlook of FO in Pakistan? Needless to say, the power sector will happily embrace the falling prices of FO as a fuel choice would automatically climb the merit-order list. However, whether or not the refineries will be able to sustain selling at such low levels remains the major question.

- On the other hand, Pakistan has already signed contracts for import of RLNG on a take-or-pay basis. If FO surpasses RLNG on the merit order list, it could be catastrophic for the country’s gas infrastructure, particularly when the country’s existing network has repeatedly been overfed to dangerous levels in the recent past, as per media.

Read more: Fighting Climate Change: JS Bank gets accredited by Green Climate Fund

We believe the gravity of the situation demands emergency action from the government. Industry experts (both local and foreign) should be consulted to formulate a strategy to tackle the issue at hand. There are 48 days and the clock is ticking!

This research piece was published from JS Global Capital’s research team.

Disclosures

JS Global hereby discloses that all its Research Analysts meet with the qualification criteria as given in the Research Analysts Regulations 2015 (‘Regulations’). Each Analyst reports to the Head of Research and the Head of Research reports directly to the CEO of JS Global only. No person engaged in any non-research department has any influence over the research reports issued by JS Global and/or no person engaged in any non- research department (other than the CEO) has any influence on the performance of the Research Analysts or on their remuneration/compensation matters.

The Research Analyst(s), author of this report hereby certify that all of the views expressed in this research report accurately reflect their personal, unbiasedand independent views about any and all of the subject issuer(s) or securities, and such views are based on analysis of various information compiled from multiple sources, including (but not limited to) annual reports, newspapers, public disclosures, financial models etc. The given sources appear to be and consequently are deemed to be reliable forforming an opinion and preparation of this report. Such information may not have beenindependently verified or checked by JS Global or the Research Analyst, and therefore, all such information as given in this report may or may not prove to be correct. It is hereby certified that no part of the compensation of JS Global or the Research Analyst was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report.

Rating System

JS Global Capital Limited uses a 3-tier rating system i.e. Buy, Hold and Sell, based on the level of expected return. Time horizon is usually the annual financial reporting period of the company.

‘Buy’: Stock will outperform the average total return of stocks in our universe ‘Hold’: Stock will perform in line with the average total return of stocks in our universe

‘Sell’: Stock will underperform the average total return of stocks in our universe

Target Price Risk

Company may not achieve its target price for various reasons including company specific risks, competition risks, sector related risks, change in laws, rules and regulations pertaining to the business of the Company as well as a change in any governmental policy. The results of operations may also be materially affected by global and country-specific economic conditions, including but not limited to commodity prices, prices of similar products internationally and locally, changes in the overall market dynamics, liquidity and financial position of the Company and change in macro-economic indicators. The company is exposed to market risks, such as changes in interest rates, foreign exchange rates and input prices. From time to time, the company may enter into transactions, including transactions in derivative instruments, to manage certain of these exposures.

Research Dissemination Policy

JS Global Capital Limited endeavours to make all reasonable efforts to disseminate research to all clients (without any preference, prejudice or

biasness) in a timely manner through either physical or electronic distribution such as mail, fax and/or email.

Disclosure Pertaining To Shareholding/Conflict of Interest

The Research Analyst has not directly or indirectly received any compensation from the Subject Company for preparation of this report or for the views expressed herein, and the Subject Company is not associated with the Research Analyst in any way whatsoever.

Subject Companies’ related parties are clients of JS Global. JS Global has provided brokerage services to Subject Companies’ related party(ies) in the past 12 months and is expected to continue to provide them with the said services in the next three months as well. For rendering such brokerage services, JS Global has received compensation by way of commission from the subject companies’ related party(ies).

No other material information (other than the one specifically disclosed in this report) exists (for JS Global as well as the Research Analyst) which could be a cause of conflict of interest in issuing this report.

Disclaimer of Liability

No guaranty, representation or warranty, expressed or implied, is made as to the accuracy, completeness, reasonableness, correctness, usability, suitability or purposefulness of the information contained in this report or of the sources used to compile the information contained in this report.

All information as given in this report may or may not prove to be correct, and is subject to change without notice due to market forces and/or other factors not in the knowledge of or beyond the control of JS Global or the Research Analyst(s), and neither JS Global nor any of its analysts, traders, employees, executives, directors, sponsors, officers or advisors accept any responsibility for updating this report and therefore, it should not be assumed that the information contained herein is necessarily complete, accurate, reliable or up-to-date at any given time.

The client is solely responsible for making his/her own independent investigation, appraisal, usability, suitability or purposefulness of the information contained in this report. In particular, the report takes no account of the investment objectives, financial situation and particular needs of investors who should seek further professional advice or rely upon their own judgment and acumen before making any investment. This report should also not be considered as a reflection on the concerned company’s management and its performances or ability, or appreciation or criticism, as to the affairs or operations of such company or institution

Consequently, JS Global and its officers, directors, sponsors, employees, executives, consultants, advisors and analysts accept no responsibility or liability towards the Client, and assume no obligation to do (or not to do) anything with respect to the information contained in this report. Research Analyst(s) and JS Global shall also not be liable in any way and under any circumstances whatsoever for any loss, penalty, expense, charge or claim that may be suffered/incurred by the client as a result of receiving, using, or having complied and distributing this report.

Warning: This report may not be reproduced, distributed or published by any person for any purpose whatsoever. Action will be taken for unauthorized reproduction, distribution or publication.

Arsalan Ahmed: arsalan.ahmed@js.com

+9221 111-574-111 Ext: 3096

Ali H. Zaidi: ali.zaidi@js.com

+9221 111-574-111 Ext: 3103