Cement is arguably the most important, and widely used, building material in the modern age. It’s used in homes, in office buildings, roads, bridges and infrastructure in general. The amount of cement consumed in a country each year is an indicator of its pace of socio-economic development and progress. Pakistan is the world’s 14th largest cement producer.

Nevertheless, its per capita cement consumption at 140kg is on the lower side in its immediate region (with China & India around) and much lower when measured against a global consumption average of 400kg. On a positive note: it indicates that the industry has significant potential to see growth with the development of the country.

Background to the Cement Industry

The cement industry of Pakistan has come a long way since 1947. Immediately after Partition, the annual production of cement in the country was 300,000 tons per year and total installed capacity was 470,000 tons per annum. The first cement factory, established in 1921, in the region, that is now Pakistan, was at Wah, Punjab.

By 1954, it became clear that demand for cement was much greater than installed capacity. A million ton was required annually but only about 660,000 tons were being supplied. To cater for the shortage, the Pakistan Industrial Development Corporation (PIDC) took the initiative of expanding production in the country.

Two cement factories were established at Zealpak and Maple Leaf, with installed capacities of 240,000 and 100,000 tons respectively. Today, the operational capacity of cement production in Pakistan is estimated to be between 46- 49 million tons, with an expected expansion to 76 million tons by 2020.

Read more: Inclusive Development Index: Pakistan scores higher than India

All Pakistan Cement Manufacturer Association (APCMA)

The APCMA, the apex body of the cement manufacturers of Pakistan, is helpful in terms of understanding Pakistan’s world of cement. It was incorporated on 14th of September 1992 under section 32 of the Companies Ordinance 1984.

Today, it plays an important role in coordinating activities of various cement plants with respect to government policies and represents all major policy-making bodies concerned with cement. It also maintains up-to-date data about cement usage, demand, capacity, and finances.

Cement Industry’s contribution to the Economy

The cement industry contributes billions to Pakistan’s economy. In 2016, it contributed approximately Rs. 20 billion to the national exchequer alone, over Rs. 40 billion is added to country’s GDP annually.

The Karachi Stock Exchange lists 21 companies in the cement sector with the net worth of these companies around Rs. 25 billion. Some of the companies operate multiple plants in various cities. As per APCMA, there are currently 24 cement plants in Pakistan.

Structure of the Industry

These cement plants are distributed across the country; mostly around the population centers. The Northern Zone consists of Upper Punjab, KP, Azad Kashmir and areas of Balochistan close to KP and Punjab. The Southern Zone, for the most part, is made up of Sindh i.e. the areas close to Karachi.

Demand for Cement

In Pakistan, residential and commercial property sectors and infrastructure projects are the key drivers of cement demand. Consumption is expected to increase in both areas.

Read more: Federal government will pay half of Balochistan’s development: PM Abbasi

Residential Demand

Pakistan is experiencing Asia’s fastest-growing urbanization and with that comes the need for more housing. One government study has shown an immediate need for housing units estimated at 9 million units.

These figures also reveal the uneven patterns of structural growth; for instance, from 2006 to 2016, the industry grew at a rate of 7% to 10% in the Northern zone whereas, in the South, it has grown at about 4%. The South is also more dependent on exports than the North. There are over 12 plants in Punjab, 5 in KP, 2 in Balochistan (for a total of 19 in the North Zone) and 5 in Sindh (Southern zone).

These plants are located in or near the major population centers in Pakistan. According to the Pakistan Bureau of Statistics, 32% of the people in Punjab, 47% in Sindh, (figures jump because of Pakistan’s urban jungle: Karachi) 17% in KP and 24% in Balochistan live in urban areas. In urban areas, the demand for cement comes mostly for new housing units.

The average cement consumption for a 5 marla Pucca house is over 540 bags, where each bag has a standard weight of 50 kilograms.

Studies by the Planning Commission of Pakistan show that by 2030, half of the population of Pakistan will be living in cities. This means over 100 million urban citizens, and these citizens will need houses to live in. Data from the Pakistan Bureau of Statistics show that there are currently over 19 million housing units in the country.

38% are single bedroom houses, around 31% are two-bedroom houses while the rest are three, four and five bedroom houses. 55% are Pucca houses (i.e. houses that are designed to be permanent dwellings), 11% are Semi-Pucca and 35% are Kacha houses (not permanent). Housing societies usually have Pucca houses.

The average cement consumption for a 5 marla Pucca house is over 540 bags, where each bag has a standard weight of 50 kilograms. New housing societies are sprouting up in and around all major cities of Pakistan. About 50% of the demand for cement comes from these schemes. There are over 5100 registered housing societies working across Pakistan.

As indicated above, these tend to be concentrated in and around major cities. 440 are in Karachi, 656 in Islamabad, 45 in Peshawar and 705 housing societies are in Lahore alone. But these figures may be misleading; according to one government official: According to the 6th population census in Pakistan conducted in 2017, Islamabad has grown by 149% since 1998, with an annual growth rate of 5%.

There has been a 60% increase in Karachi’s population and a 116% increase in the population of Lahore since the previous census. Similar percentages of the increased population have been documented in other major cities of Pakistan. These increases correlate with a need for an increase in production capacity in the country.

Prime Minister Abbasi is exploring the possibility of reviving the stalled Apna Ghar Housing scheme, a bold initiative set up to build 500,000 housing units per years. The formation of a new public limited company was discussed by the federal government in 2013, but the scheme was not launched earlier. The initiative will provide affordable housing on easy instalments to low-income groups.

Read more: Baloch Chief Minister approves Rs. 1 billion for Gwadar’s development projects

Infrastructure demand

In Pakistan, the network of roads has grown steadily, despite changing governments and political instability.

Portland Cement-one of the most Common Types of Cement used for Building Houses

According to the ministry of finance, 90% of national passenger traffic and 96% of freight movement in Pakistan occurs through roads. The transport and communications sector contributes about 10% of the country’s GDP.

As per the National Transport Research Center, the total length of roads in Pakistan is over 264,000 kilometers. It is estimated that about 900 tons of cement are required to lay one kilometer of a simple two-lane road.

Impact of CPEC

Probably no country has had faster industrial development and growth in modern history than China. It is no surprise then, that, the largest cement manufacturing industry today also exists in China.

In 2017, over 60% of the world’s cement was produced and consumed in China (population: 1.3 billion) followed by India (population: 1.2 billion) at 6% and then the USA (population: 330 million) at 2%. And the cement industry of China is 30 times larger than that of the US.

In 2016, 2400 giga-tons of cement (Giga equals a thousand million) were manufactured in China. After decades of double-digit growth, Beijing is now reaching outwards and expanding its economic influence. The Belt and Road Initiative (BRI) also referred to as OBOR (One Belt One Road) is a multi-trillion-dollar mega-project that will connect China with Europe, Eurasia, Africa and the Middle-East via road and sea-links.

China Pakistan Economic Corridor (CPEC) is its flagship project – and the only one that is seeing physical progress so far. The economic corridor comprises a network of infrastructure projects, energy projects industrial parks and more. The cement industry of Pakistan is expected to get a boost from this.

According to some experts, at least 3 million tons of demand will be generated through CPEC.

Pakistan’s cement industry is currently running at 95 percent capacity that has encouraged the domestic cement manufacturers to spend an estimated $2.25 billion on new production capacity. “The China-Pakistan Economic Corridor (CPEC), is expected to have the huge impact on cement production levels, with a Joint Cooperation Committee having been established to promote the construction of CPEC between 2013-30,” according to Cement.

A network of roads is going to connect different parts of Pakistan with each other and the port of Gwadar with Xinjiang province in China. It is the biggest infrastructure project in Pakistan’s entire history and will guarantee increased demand of cement. According to the International Cement Review, “robust construction activity has led to local cement producers increasing capacity at a break-neck speed.”

Read more: Telenor makes a contribution to Sustainable Development Goals- Agenda 2030

Cement manufacturers are thus eyeing new opportunities with CPEC. Pakistan’s Maple Leaf Cement Factory told the Pakistan Stock Exchange that the company had placed an order to Danish firm FLSmidth for the establishment of a new cement production line with a daily capacity of 7300 tons.

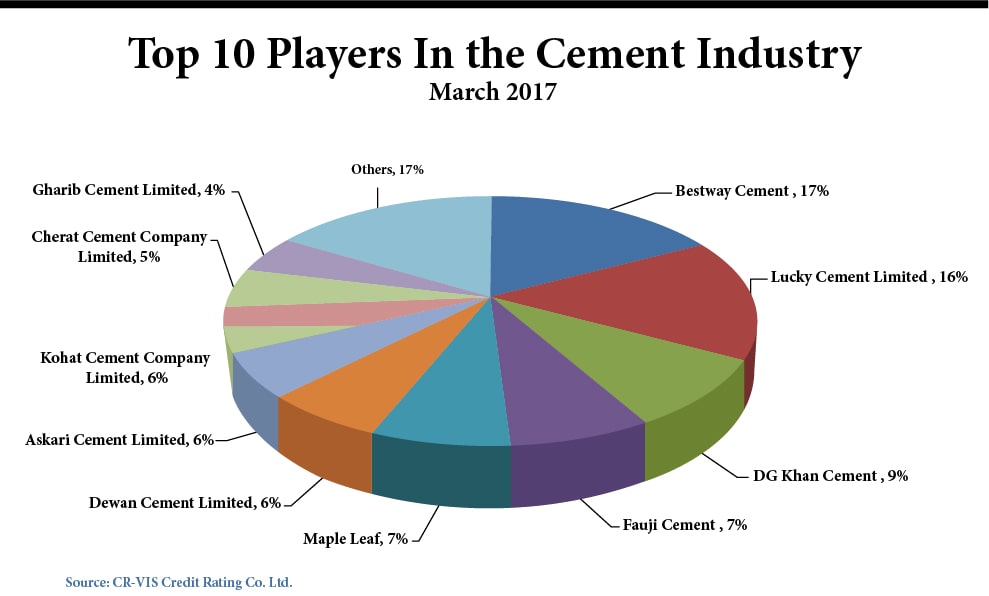

Similarly, Bestway Cement, a subsidiary of Bestway Group UK, the largest cement manufacturer in Pakistan, (with around 17% of the market) informed the Pakistan Stock Exchange in March 2017 that it will set up a brownfield cement plant with a capacity of 6000 clinker at its Farooqia site in northern Pakistan.

The CEO of Bestway Cement said in an interview, “CPEC will ensure that the economy will grow at a faster pace generating employment and business opportunities for many industries and the cement industry will be at the helm of it.”

Exports of Cement

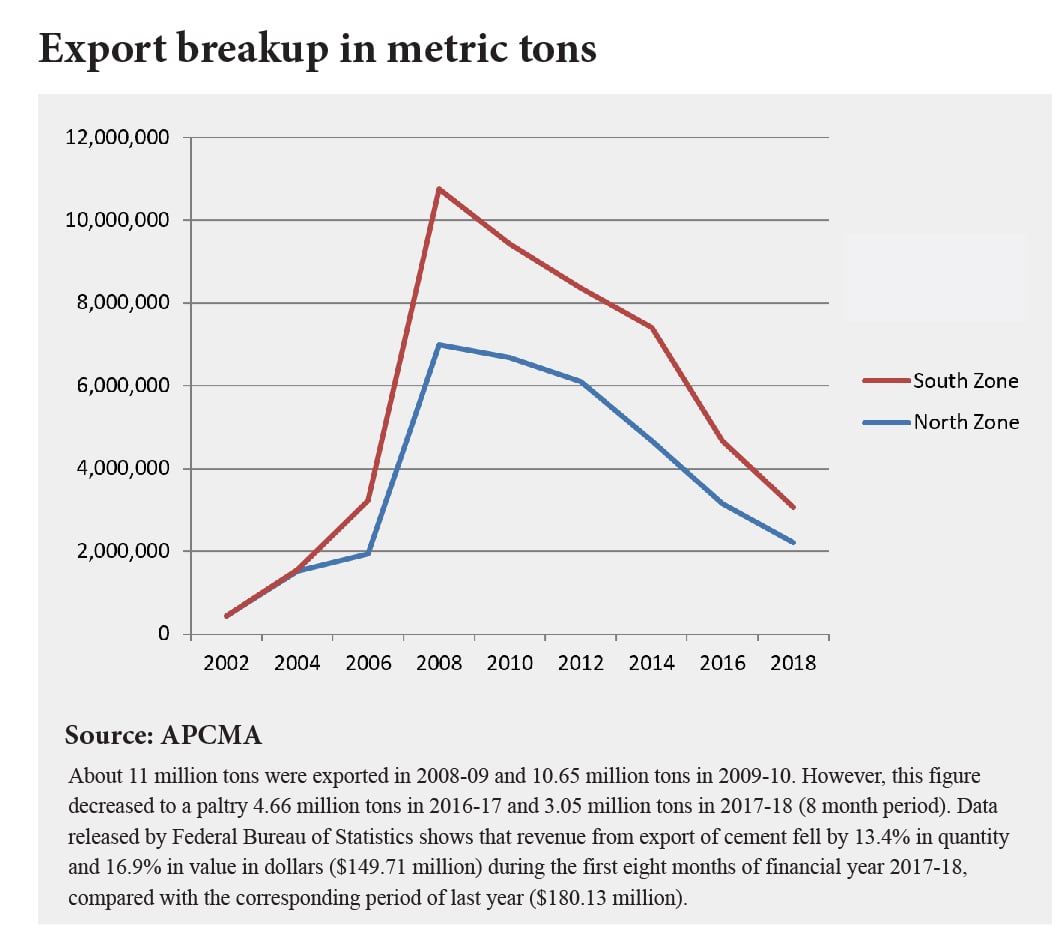

Both the North and South zones, in Pakistan, have distinct demand dynamics. Companies in the South, close to Karachi port, have greater revenue diversification as demand also comes from the export markets versus those in the Northern zone that benefit from stronger local demand.

Export dispatches represented around one-third of total dispatches for companies based in the South vis-à-vis only one-tenth for those in the North. However, the last several years has seen Pakistan’s exports hit in a number of countries (South Africa, other African countries, Iraq, India, Afghanistan). Many of these countries increased local capacity. South Africa had introduced a dumping duty in 2015.

Other reasons for the decrease in exports include increases in the cost of production and tax burdens. Nearly 60% of production cost is made up of payments that cement manufacturers have to make for procuring oil or imported coal, both of which are necessary for making cement depending on the manufacturing process. The federal excise duty, a form of the tax burden on the industry, has also been increased recently.

In the North, exports were mainly limited to Afghanistan, which has also been hit due to a number of reasons, the decline in Afghanistan’s GDP after the coalition forces left and spending decreased in the country, the influx of cheap Iranian cement into Afghanistan (which is of much inferior quality as compared to Pakistani cement) and the political relations between the two countries.

Issues facing the Cement industry

APCMA has been urging the federal government to impose a 20% import duty on cement from Iran, arguing that manufacturers from Iran are “dumping” their produce in border markets. Furthermore, contrary to APCMA hopes, the budget statement for 2018 by the government is not encouraging as far as the cement industry is concerned.

According to the budget in brief, funds allocated for Public Sector Development Programs (PSDP) were only increased from PKR 1,675 billion in 2016-17 to PKR 2,113 billion. At the same time, an increase to PKR 1.25 per kg from PKR 1 per kg in the levy of federal excise duty has been proposed, according to the tax memorandum by A.F.

There are long-standing issues that contributed to the woes of cement manufacturers. Since cement plants are concentrated in the North, they face high transportation costs if they aim to export cement, for lack of infrastructure across the country.

Ferguson & Co. This will not help the cement industry in the country. Freight subsidy to cement exporters in Pakistan would be highly appreciated by manufacturers across the country. In May 2011, the Chairman of the APCMA urged the federal minister of finance to release PKR 270 million in inland freight subsidy to help manufacturers export cement, since domestic demand was stagnant.

High transportation costs meant that cement factories could not easily export what they produced. This allows cement manufacturers from Iran and Tajikistan to penetrate the market in Afghanistan at a lower cost per bag of cement at the expense of Pakistani cement producers.

Read more: Environmental Degradation in Pakistan and its impact on Socio-economic development

Pakistan is the fifth most populous country in the world, (pop: around 220 million) with a middle-class comprising tens of millions. There is no question about the potential for growth in Pakistan and cement manufacturers will be keeping an eye on GDP growth and the corresponding demand for cement in the coming years. Indeed, capacity utilization has been picking in recently.

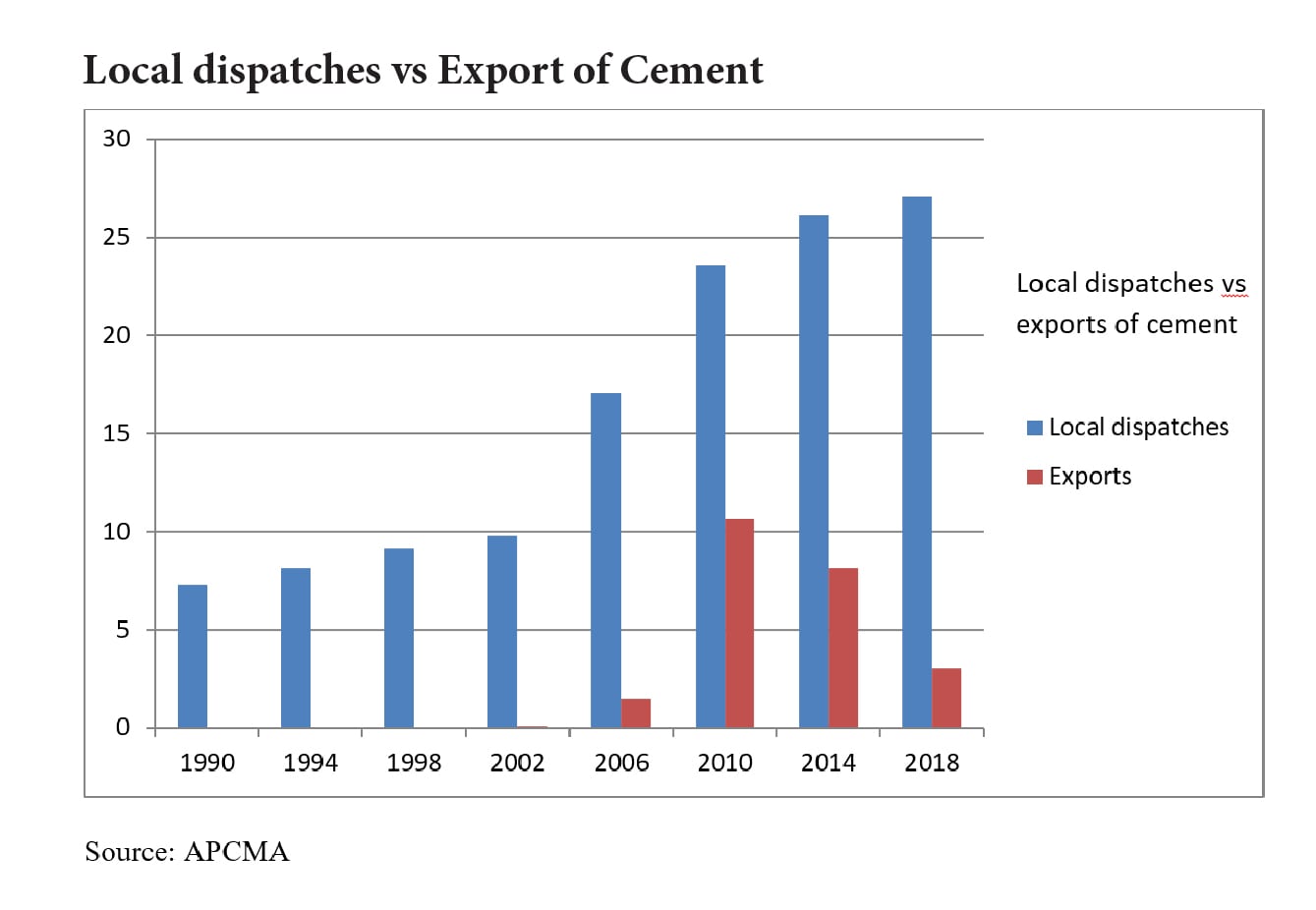

From 74% in 2008-09, it has increased to 85% in 2015-16, 86-90% in 2016-17 and 91% in 2017- 18. Capacity utilization means the industry can provide more cement if there is demand since all factories collectively are not operating at 100% capacity.

According to one study of 12 cement manufacturers covering 87% of the total market share, the production capacity in the country is set to rise up to 63 million tons in the financial year 2019-20 and 73 million tons in 2020-21. A lot of this optimism is a product of – apart from improved security situation and stable economic growth – China Pakistan Economic Corridor (CPEC).