JS Global Research|

It seems tensions in the Middle East have found a permanent spot in investment risks globally. Whether or not they are specifically mentioned, it seems these risks remain an underlying assumption. US-Iran relations, in particular, have been tense and the recent killing of General Soleimani just goes to show that one should always be braced for significant news-breaks.

With respect to Pakistan, we expect the unfolding events in the Middle East to supersede all other headlines on the mainstream media, at least for the time being

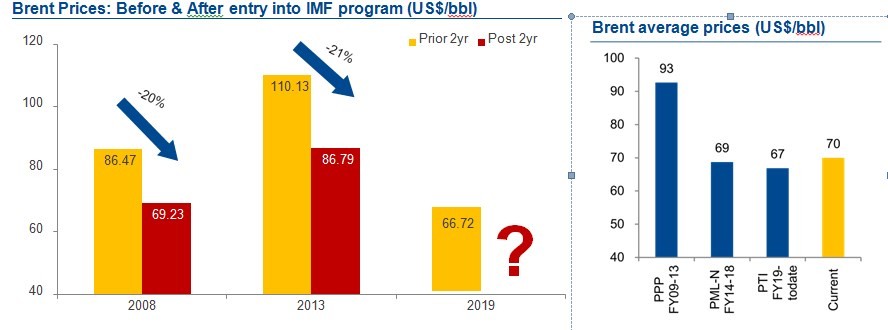

Naturally, commodities were hit by a raging bull; gold and oil in particular both shot up. Considering global geopolitical and economic risks, we feel gold could reach new highs in 2020 and could, therefore, provide a good hedge. However, we certainly do not wish the same for oil. Just to give a sense of where these currently stand, let us determine what levels should be viewed as ‘high’. In the past few years, Brent prices averaged under the US$70/bbl mark.

From another perspective, we see that oil prices tend to fall by ~20% 2 years post-entry into an IMF program from the preceding 2 years average. For history to repeat itself, general oil prices should fall to ~US$50/bbl. That is quite a fall considering the current price level of ~US$70/bbl. Here, we would direct your attention to a previous research note (titled Lower oil prices? Yes, please!) where we highlighted:

- As our economy treads on the edge, we find it necessary to state the obvious: we simply cannot afford higher oil prices this year

- Here, we should also admit that we are in a much worse tangle than we were in

- If history has taught us anything, it is that geopolitical tensions have a strong tendency of escalating through miscalculations. In any such scenario, our economy – and by extension, equity markets – are bound to suffer the consequences in collateral damage.

In fact, the way global leaders have reacted to the news gives an impression that event could be counted among the miscalculations stated above. After all who could have expected the situation to escalate to such heights so quickly from the US-embassy attack in Baghdad on New Year’s Eve? The event that transpired was by no means ordinary and could lead to grave geopolitical repercussions.

Read more: Kamyab Jawan: JS bank partners with UNDP to empower youth

Capital markets reacted in their typical fashion; The S&P500 came under pressure as did other global equity markets. With respect to Pakistan, we expect the unfolding events in the Middle East to supersede all other headlines on the mainstream media, at least for the time being. Having achieved the benchmark index levels of 40-42k that we had called for earlier in Nov-2019, it now seems as if the range could prevail (or even slip) for some time with higher volatility.

The recent market high was around the target we had predicted in our 2019 strategy report. With all the negativity built in, our view could not have been clearer.

- 2019 could be the bitter pill we have to swallow given our excesses in the previous few years… Technically, the market should find support at these levels. If not, it would not be a pretty sight

- In our view, equity valuations have still not fully absorbed the severity of the economic slowdown… Our universe has an earnings growth of 19% for FY19. If we exclude Banks and E&Ps, the growth falls to -2%. This is reflective of a slowdown in the economy which is expected to become more evident especially in the first half of CY19 earnings.

- This leads us to believe that a tipping point lurks round the corner, independent of the funding gap scenario. Therefore, buying on dips is an effective strategy to secure reasonable returns: we believe levels below 38,500 are prime investment opportunities.

(JS Global – Pakistan Market Strategy 2019)

Despite having anticipated the storm that was 2019, we admit the onslaught of numerous waves did frighten us to a great extent as well. Yet, it all somehow felt normal. And that is the beauty of stock markets. After all, what are markets but a representation of collective investor sentiments? The slightest signs of improvement lifted investor sentiments and the rest is history.

“The rally, which was broadly expected to start closer to the end of CY19 or somewhere in CY20 came in like a wrecking ball well ahead of time. On one hand, there was a series of back-to-back positive news flows, while on the other, fears that had previously gripped investors never saw the light of day. Not too long ago, many were apprehensive of highly stringent IMF conditions, minibudgets, a ~Rs200/USD exchange rate and 18% interest rates”

(JS Global – Pakistan Market Strategy 2020)

Read more: Financial giant JS Bank partners with Al-Haj FAW motors

This just goes to show that predicting the stock market in the short term is a tall order. We ourselves admit to getting short term predictions wrong more often than not. Lets see what Warren Buffett had to say during the depth of the 2008 crisis:

“Let me be clear on one point: I can’t predict the short-term movements of the stock market. I haven’t the faintest idea as to whether stocks will be higher or lower a month – or a year – from now.”

A quick market survey of the index targets reveals a somewhat leptokurtic distribution with a mean around the 50k level. This suggests a fear bias, particularly considering (1) the recent bull rally and (2) where we are coming from. On a side note, we sometimes feel that this phenomenon resonates with Keynes’ beauty contest. That said, the 60K target mentioned in our latest strategy report (one which we recommend investors to embrace with a long term view) is a suggestive target. We can’t possibly know where we will land in exactly a year or beyond. What we do know is the difference between mean reversion and re-rating. And we would like to invite investors to understand the same. Getting to historic averages should not be termed as re-rating.

That said, we would like to touch back on the risks. We mentioned oil prices could be a major threat to the economy. However, a front loaded IMF program, centered around a colossal FBR target has its own hazards. Apart from this target, the IMF program has been more or less do-able. In fact, in hindsight, we would step out on a limb and say that the first IMF Staff level report in Jul-2019 was a turning point for the market!

JS Global Capital Limited uses a 3-tier rating system i.e. Buy, Hold and Sell, based on the level of expected return. Time horizon is usually the annual financial reporting period of the company

Nevertheless, we would like to highlight that one should not confuse macroeconomic stabilization with growth in the real sector, at least in 2020. Fiscal austerity is expected to stay. After all, we are still in the first year of the IMF program. Besides, the improving long term forecasts that the IMF has shared in the staff level reports are contingent upon Pakistan meeting the set targets. We for one would keep a close watch on the debt to GDP ratio considering the underlying message: either we continue to generate high revenues, or we brace for the austerity of proportions unheard of in Pakistan.

And that is precisely why we prefer to look beyond 2020 for direction on the economy. Regardless, the impressions that we get from the current environment do kindle a light. We believe due time should be given for these impressions to materialize. After all, they could play a crucial role in putting the country on a path to great success!

Courtesy: JS Global Research published 6 January

Disclosure

JS Global hereby discloses that all its Research Analysts meet with the qualification criteria as given in the Research Analysts Regulations 2015 (‘Regulations’). Each Analyst reports to the Head of Research and the Head of Research reports directly to the CEO of JS Global only. No person engaged in any non-research department has any influence over the research reports issued by JS Global and/or no person engaged in any non- research department (other than the CEO) has any influence on the performance of the Research Analysts or on their remuneration/compensation matters.

The Research Analyst(s), author of this report hereby certify that all of the views expressed in this research report accurately reflect their personal, unbiased and independent views about any and all of the subject issuer(s) or securities, and such views are based on analysis of various information compiled from multiple sources, including (but not limited to) annual reports, newspapers, public disclosures, financial models etc. The given sources appear to be and consequently are deemed to be reliable for forming an opinion and preparation of this report. Such information may not have been independently verified or checked by JS Global or the Research Analyst, and therefore, all such information as given in this report may or may not prove to be correct. It is hereby certified that no part of the compensation of JS Global or the Research Analyst was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report.

Rating System

JS Global Capital Limited uses a 3-tier rating system i.e. Buy, Hold and Sell, based on the level of expected return. Time horizon is usually the annual financial reporting period of the company.

‘Buy’: Stock will outperform the average total return of stocks in our universe

‘Hold’: Stock will perform in line with the average total return of stocks in our universe

‘Sell’: Stock will underperform the average total return of stocks in our universe

Target price risk

Company may not achieve its target price for various reasons including company-specific risks, competition risks, sector-related risks, change in laws, rules and regulations pertaining to the business of the Company as well as a change in any governmental policy. The results of operations may also be materially affected by global and country-specific economic conditions, including but not limited to commodity prices, prices of similar products internationally and locally, changes in the overall market dynamics, liquidity and financial position of the Company and change in macro-economic indicators. The company is exposed to market risks, such as changes in interest rates, foreign exchange rates and input prices. From time to time, the company may enter into transactions, including transactions in derivative instruments, to manage certain of these exposures.

Research Dissemination Policy

JS Global Capital Limited endeavours to make all reasonable efforts to disseminate research to all clients (without any preference, prejudice or biasness) in a timely manner through either physical or electronic distribution such as mail, fax and/or email.

Disclosure Pertaining To Shareholding/Conflict of Interest

The Research Analyst has not directly or indirectly received any compensation from the Subject Company for preparation of this report or for the views expressed herein, and the Subject Company is not associated with the Research Analyst in any way whatsoever.

No other material information (other than the one specifically disclosed in this report) exists (for JS Global as well as the Research Analyst) which could be a cause of conflict of interest in issuing this report.

Disclaimer of Liability

No guaranty, representation or warranty, expressed or implied, is made as to the accuracy, completeness, reasonableness, correctness, usability, suitability or purposefulness of the information contained in this report or of the sources used to compile the information contained in this report.

All information as given in this report may or may not prove to be correct, and is subject to change without notice due to market forces and/or other factors not in the knowledge of or beyond the control of JS Global or the Research Analyst(s), and neither JS Global nor any of its analysts, traders, employees, executives, directors, sponsors, officers or advisors accept any responsibility for updating this report and therefore, it should not be assumed that the information contained herein is necessarily complete, accurate, reliable or up-to-date at any given time.

The client is solely responsible for making his/her own independent investigation, appraisal, usability, suitability or purposefulness of the information contained in this report. In particular, the report takes no account of the investment objectives, financial situation and particular needs of investors who should seek further professional advice or rely upon their own judgment and acumen before making any investment. This report should also not be considered as a reflection on the concerned company’s management and its performances or ability, or appreciation or criticism, as to the affairs or operations of such company or institution

Consequently, JS Global and its officers, directors, sponsors, employees, executives, consultants, advisors and analysts accept no responsibility or liability towards the Client, and assume no obligation to do (or not to do) anything with respect to the information contained in this report. Research Analyst(s) and JS Global shall also not be liable in any way and under any circumstances whatsoever for any loss, penalty, expense, charge or claim that may be suffered/incurred by the client as a result of receiving, using, or having complied and distributing this report.

Warning: This report may not be reproduced, distributed or published by any person for any purpose whatsoever. Action will be taken for unauthorized reproduction, distribution or publication.