The Ministry of Energy has failed to acquire RLNG in accordance with the country’s needs; even this year, only 900 Mmcfd of LRNG was imported, compared to the 1200 Mmcfd imported last year. This year’s 25% supply shortfall is due to the Energy Ministry’s inability to arrange supply hurting the very future of Pakistan’s export and economic future.

The textile sector of Pakistan has colossal potential for uplifting the teetering economy of the country, as clearly evident by its contemporary contribution to the country’s GDP as its largest manufacturing and exporting sector. The textile industry has experienced an unprecedented growth rate, as manifested by a 36 percent increase in exports in November 2021 over the same period last year. The industry has set a target of $21 billion for the current fiscal year and $25 billion for the coming fiscal year. This rapid expansion of the textile sector during the last year was due to enhanced competitiveness as a result of regionally competitive energy tariffs.

Read more: Tech, human Factor and gender parity: Prerequisites for economic growth

Another added challenge for Pakistan

Pakistan has faced significant challenges, owing largely to our inability to organize the availability of energy at a reasonable cost in a world where energy supply is abundant and evolving technology is making it cheaper. Our history is littered with episodes of ‘stop-go’ growth caused by energy shortages and exorbitant costs, both of which are the result of mismanagement, just as reflected by contemporary developments. Currently, the Government has raised gas/RLNG tariffs for Punjab-based industries but more perilously has imposed a complete gas/RLNG shutdown for the mills on 15th December 2021 as opposed to a promise made earlier not to do so.

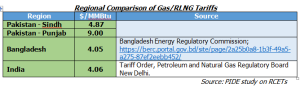

Surprisingly, the province that holds around two-third of the industrial base does not have the lowest tariffs. There is a huge differential in Gas Prices for Industrial Units in Sindh, KPK, Baluchistan and Punjab. The gas/RLNG rate for KPK and Sindh is Rs 852 ($ 4.87) and for Punjab is Rs 1575 ($9)/MMBTU. Not only is this patently discriminatory but it spells the end of the industrialization drive in Punjab.

The 85 percent increase in gas/RLNG rates is catastrophic for Punjab based export industry. The export industry in Punjab will have to face the negative consequences resulting from the recent gas/RLNG load shedding. This will result in a monumental disparity in the two prices for essentially the same product and will result in the closure of the industry located in Punjab, which accounts for 65-70% of the total installed capacity of Pakistan.

The exorbitant gas/RLNG tariffs will make the products uncompetitive domestically and internationally while load shedding will result in production losses and delays. The suspension of gas will push 80% of the industry to a complete halt coupled with the loss of orders subsequently which will be challenging if not viable to reverse. These steps have been taken despite the country having posted record growth and performance significantly exceeding anticipated growth in exports.

Read more: PIDE: A revolutionary think tank for Pakistan and beyond

Under these circumstances, who will purchase the products of Punjab based industry?

The competition in the world market will be fierce for any residual market so it is essential the cost of goods supplied should not be increased in any way. Any shortage or increase in energy pricing would definitely lead to the loss of the competitive advantage of Pakistani products. The major factors of production in textiles apart from the capital are raw material (i.e., cotton), energy and labor.

Due to intense competition among regional countries, a minor cost difference in relative terms brings an exponential impact on the international market. An increase in energy tariffs will undermine the entire industry’s efforts and offset the economic progress made over the past year, as the textile industry will struggle to remain productive under the pressure of unsustainable high energy tariffs. Our regional competitors are offering gas/RLNG at much lower rates than Pakistan.

At this stage, where Pakistan’s industry is in the midst of impressive expansion and is successfully attracting a healthy level of investments, a rise in costs coupled with gas suspension would directly result in a reduction in market share, once again leaving Pakistan far behind its regional competitors. The promising levels of export growth in the past few months, with positive impacts on industrial expansion and job creation, are a boon for economic stability in the country, and henceforth must be maintained through the continuation of the critical RCET policy across the country and entire value chain.

Most mills at present cannot fulfill the energy needs for power or gas alone and require both to function at full capacity. Furthermore, approximately 80% of the Gas/RLNG “Captive” plants are cogeneration and use steam & hot water in the production process. These mills do not have alternate sources of steam and hot water and cannot generate these from electricity now that the supply of Gas/RLNG is suspended to the Punjab-based industry which will close down as a result. The current momentum of exports will be lost leading to disastrous consequences which will be long-lasting as export orders lost will lead to the buying houses sourcing these from other countries on a permanent basis.

Read more: Anti-export bias that is stifling Pakistan’s growth

The power requirement of the textile industry is 650 MWs, currently, 350 MWs are being utilized and additional 300 MWs are required on account of ongoing BMR and expansion initiatives of industries as is evident from a large number of extensions of load applications available. The Energy Ministry needs to sensitize these serious issues in the power sector so that they may take all steps to continue the immediate supply of Gas/RLNG to the Industry across the value chain and without distinction on captive/Industrial/Cogen as all these uses are intertwined.

Understanding the issues regarding RNG-based plants

As far as switching the Gas/RNG-based captive plants to electricity is concerned, the issues in the enhancement of load, new connections and quality of supply at present seem to be intransigent and not resolvable in the short term. The electricity from the grid has been inconsistent and unstable. The industry is experiencing significant production losses as a direct consequence of the irregular supply of grid electricity. The latest machinery being used in the industry is equipped with electronics (electronic cards/chips) which are highly sensitive to electricity fluctuations.

The cards/chips installed in the machinery burn out or trip if there are variations in frequency/voltage/supply of electricity, halting the entire production line. The industry experience of utilizing grid electricity hasn’t been productive so far. Apart from production losses, the capacity and performance of installed machinery are also compromised – adding further maintenance and repair costs.

The cost of Regionally Competitive Energy Tariff (RCET) is less than 2 percent of exports. This foreign exchange does not have to be repaid or serviced at high-interest rates. The industry has delivered to the nation by investing Rs450 billion in machinery for capacity enhancement for export-led growth as per the commitment. Most analysts believe that if the cost of doing business/energy had remained stable, exports would have risen to at least $45 billion by now, rather than plummeting to such low levels in the past.

Read more: Tackling the issue of rising import bills in Pakistan

There is practically no subsidy on energy even though it is essential for the export sector without protection in terms of tariff, it would have to compete on a pure cost/ quality basis in the international competitive markets. The disparity in energy pricing and gas load shedding will seriously retard Pakistan’s bid to accelerate economic development as a major sector of the economy.

A systematic solution for equity in energy pricing and availability in Pakistan should be opted for on an urgent basis. Under such a mechanism, the government needs to announce a single industrial gas/RLNG tariff across the country. On the other hand, the economic benefits of uninterrupted gas/RLNG supply and uniform rates to the industrial sector will comprise enhanced exports, boost competitiveness, job creation and have a multiplier effect on the value chain.

Mr. Shahid Sattar, now Executive Director & Secretary General of All Pakistan Textile Mills Association (APTMA), has previously served as Member Planning Commission of Pakistan and an advisor to the Ministry of Finance, Ministry of Petroleum, Ministry of Water & Power.

The views expressed by the writers do not necessarily represent Global Village Space’s editorial policy