A pension is a periodic payment made by the government in exchange for services rendered by a government employee per the rules. With a relatively low wage structure, job security and pension are the main draws that entice citizens to work in the government sector. Initial legislation regulating pension matters in the subcontinent was enacted through the Pension Act of 1871. Basic principles and conditions under which pensions are earned by service in public departments and the manner of calculation are laid down in the Civil Service Regulations (CSR). Major reforms introduced over the years include Pension cum-Gratuity Scheme 1954, Liberalized Pension Rules 1977, Revised Pay Scales 2016, and Revised Pay Scale 2017.

Pakistan’s civil servants’ pension scheme is a noncontributory, unfunded defined benefit scheme. If desired, an officer or official is entitled to a defined annuitized benefit at 60 or upon completion of 25 years of service. The benefit is calculated as the number of years of service multiplied by the accrual factor times the pensionable salary. The employer is responsible for all of a defined benefit plan’s planning and investment risk. Benefits can be distributed as fixed-monthly payments like an annuity or in one lump-sum payment. The federal and provincial governments are paying pensions to retired employees through their revenues on a pay-as-you-go basis.

Federal and provincial pension expenditure has touched around one trillion dollars, and the pension figure for the federal government includes military pensions as well. The pension system for public sector employees operates as an unfounded (pay-as-you-go) system, which places substantial financial pressure on budgetary allocations.

Read more: Pensions: A brewing disaster

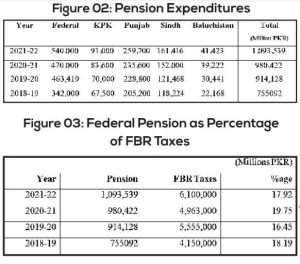

The budget for 2021–22 initially allocated 480 billion rupees for pensions or 6.3 percent of the total budgeted current expenditure of 7523 billion rupees, but with revised estimates projecting current expenditure at 8694 billion rupees, pension outlay is also revised up to 540 billion rupees as a percentage of current expenditure revised to 6.2 percent.

The tables below, which have been compiled from federal and provincial budget books, show the approximate expenditures of the last four years, which affirms that the crisis of pension expenditure is on the rise.

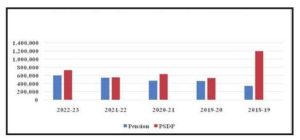

The graph shows that the federal expenditure on pensions is almost equal to the Federal Public Sector Development Program (PSDP). Although the ratio has slightly improved in the current financial year, the financial indicators are not very positive and a cut is expected in the development program.

In the financial year 2019-2020, federal government pension expenditures for civil and military employees increased by 1% and 2%, respectively, as the federal government did not announce any increase in the pension, which shows that the mushrooming expenditures are mainly occurring due to annual increments in pension.

The above numbers indicate that the problem is not an increase in the number of pensioners but the management of pension expenditures. The proportion of the increase in pension amount in relation to the rise in the number of pensioners is a point of concern.

At the request of the Finance Ministry, the World Bank prepared a comprehensive report titled “Pakistan Assessment of Civil Service Pensions (2020)” by using actuarial projections to evaluate the fiscal costs and adequacy of the existing pension scheme and its suitability. The report suggested that Pakistan’s civil servants’ pension schemes have growing budgetary expenses, which, if not constrained, threaten other development priorities. These costs have increased since 2012 from about 4.5% of provincial fiscal revenues in Sindh and 6.7% in Punjab to about 12% of provincial revenues in 2019. Actuarial projections in this report suggested that these costs and growing salary costs will continue to grow substantially in the coming years, crowding out other scarce public expenditures.

Read more: Rise in pension expenditure has the SBP worried

The problem is evident and is discussed at national and international forums. All studies conducted by the government, academia, and international institutions such as the IMF, World Bank, and Asian Development Bank have concluded that pension expenditure is a simmering crisis that has emerged as a new circular debt because the government will have to borrow money to pay the pensions. Further, the pensions will crowd out the expenditure on other social and development goals.

Regarding policy options, the PP&Cs of 2001, 2004, and 2009 worked on pension reforms and unambiguously recommended that the existing pension system be phased out for new government employees. The move from defined benefit to defined contribution for all new entrants needs an hour. The present pensioners also need to be rationalized in reducing the number of family members eligible for family pensions. Moreover, the inclusion of previous increases in pension is also creating a burden that needs to be removed.

Unfortunately, various governments have allowed pension design liberalization, significantly altering retirement and survivorship benefits. The unique balance in the pension system required to achieve equilibrium has been destroyed. Initially, the pensionable earnings were calculated as the average of the previous three years. This was changed to the last paycheck received. Likewise, family pensions were allowed for five years, which were extended to 10 and then for life. The survivorship beneficiaries were extended to grandchildren. The average payment of a pension to a retired person and his family extends for more than 40 years. Effectively, a pension is being paid for more years than the years served.

Another noteworthy point is the construction of pension committees. Pay and pension committees are, by and large, headed by retired bureaucrats and senior management of the bureaucracy. This is an odd committee with a tilt toward protecting the existing

pension system. All members had a stake in continuing the current system. Almost all the recommendations from all the committees were for the new entrants. There needed to be a recommendation for rationalizing the existing system and cutting some generous benefits. The membership of the present committee reflected the same.

Successive governments should have implemented the recommendations due to obvious political and institutional reasons and the absence of a roadmap. The political and bureaucratic will to implement the reforms needs to be improved to create the window of opportunity to implement the reforms because pensioners, government servants, and the armed forces are big vote banks.

Read more: Pakistan’s Unsustainable Pension Bomb

Indian experience in this regard is worthy of examination, as Indian authorities set out in the late 1990s to identify options to reduce the long-term cost of India’s civil service pension scheme and to expand private sector pension coverage. The New Pension Scheme (later renamed the National Pension System) started operation in 2004; the old civil service pension scheme was closed to new entrants, and all accrued rights under the old scheme were protected for existing civil servants. The new government scheme was a funded defined-contribution scheme with a 20% contribution rate (10% employer and 10% employees). The Indian authorities also established an independent regulator whose exclusive responsibility is for pensions, i.e., the Pension Fund Regulatory and Development Authority (PFRDA). A separate institution, the NPS Trustee Bank, was established to receive participant contributions and transfers. A central recordkeeping agency was established to manage members’ accounts and provide information on individual accounts.

It is suggested that the annual pension increase be indexed to the Consumer Price Index (CPI). The increase in pension will be 60% of CPI, subject to a maximum increase of 10%. For this purpose, the CPI of the immediately preceding calendar year can be used. This would give a reasonable raise in the monthly pension, which would compensate for the inflationary pressures and delink it from the salary increases.

Contributory pension schemes similar to those used in India may be implemented for all new entrants. The KPK government has initiated a scheme in this regard. This should be implemented throughout the country. With more than ten pension funds available in the private sector, the government should select 2–3 funds for investments and offer them to the new entrants. The officers and government should contribute 10% of each officer’s pay to a pension fund. The government’s responsibility should be limited to depositing the government’s share in the designated branch. The scheme should have some guaranteed return as the market can be volatile and result in losses. A hybrid model of guaranteed return and some variable rate of return can be devised to protect the government employee from market shocks. For this, the fund managers and actuarial office of the Finance Division have to develop a payment structure.

With each passing day, future pension promises are becoming more deeply entrenched, making reform even more challenging. We are at the point of “now or never.” The existing pension scheme in its present form is adding a multiplier effect to the already strained financial resources and requires far-reaching changes. The scheme will continue to cost money for the first 20 years as the previous ones are being phased out. But at the same time, the deposits would flow into the market and improve the country’s overall savings ratio.

Thus, tempering the existing pension system is indeed an uphill task, and it will undoubtedly be criticized when there is stress on the employees’ contribution; nevertheless, without such ostracized reforms, Pakistani taxpayers and administrations would be forced to allocate an increasing amount of money for pensions that would soon become even more financially unsustainable than at present.

Saud Bin Ahsen works at Lahore based public policy think tank. He has done MPA (Master of Public Administration) from Institute of Administrative Sciences (IAS), University of the Punjab, Lahore. He is interested in Comparative Public Administration, Post-Colonial Literature, and South Asian Politics. He can be reached at saudzafar5@gmail.com. The views expressed in the article are the author’s own and do not reflect the editorial policy of Global Village Space.