Just as we stopped talking about the current account deficit, a new monster has appeared on the scene: Pakistan’s pension time bomb that is dangerously ticking away. The fact it found its way into Prime Minister Imran Khan’s speech last month says a lot about its importance and also about the prime minister’s attention to topics that most PM’s would not have found exciting enough to talk about.

In the last ten years whilst Pakistan’s tax revenues increased by 2.7 times, the pension bill from the federal government which includes military pensions (36% or less of the annual pension liabilities) increased by 5.2 times. The provincial toll is said to be even higher with numbers estimated at 7.1 times.

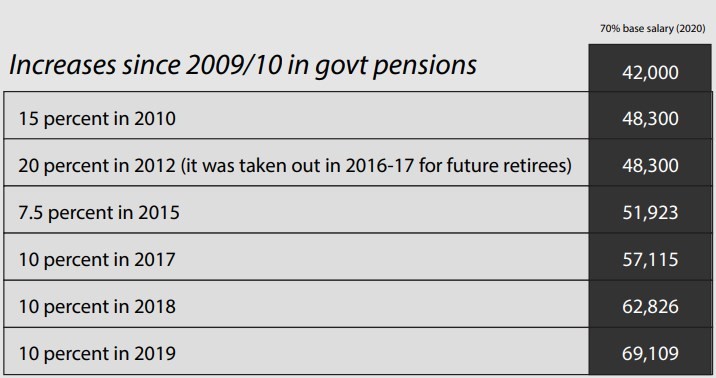

A small line added in 2009-10 when the federal government increased pensions; that all the increases would be applicable to future retirees has become the straw that will break the camel’s back. It means that a government employee retiring in 2020 is entitled to all the previous increases (from 2010 onwards) in pension pay.

Read more: Pakistan’s way forward out of recurring economic crises

Assuming that an individual receives Rs 60,000 as their base salary and they retire today. Their pension was to be 70% of their final salary (42,000). However, they are entitled to all previous increments in pension and hence their base pension is actually around Rs 70,000 (medical allowances have also seen increases and are given to pensioners but for this example, we have excluded). What they get as pension at retirement is greater than the salary they received when they were working.

Implications

In 2010, the pension expenditure of federal (including military) and four provinces was Rs164 billion, FY21 it is estimated at Rs988 billion. Future pension liabilities run in the trillions, Hasaan Khawar, a development expert, estimates these at Rs. 35 trillion.

Since 2013, numbers of government retirees have increased by 25 percent; however, the pension expense has increased by 432 percent from Rs 55 billion to Rs 238 billion. The total pension liabilities of the federal and provincial governments last year claimed a quarter of revenues collected by FBR.

What makes matters worse is that the government funds all pension costs through its annual budget; currently, there is no provision for funding pension liabilities

This year the cumulative annual pension payments are expected to touch a trillion rupees – in the next decade, it is expected to become the single largest item in the government budget after debt payments. These pension liabilities are separate from the huge pension payments in various state-owned enterprises that also fall under government responsibility and do not appear in these numbers.

Read more: Pensions: a never ending flow of money from the exchequer?

This law incentivizes early retirement. The same time, with more money, can be spent employed in the private sector, or even indulging in leisure. In 2006-10 the figures for early retirees to total retirees in Punjab were around 22 percent, by 2019 this number stood at 63%. The percentage of pensioners to employees in Punjab grew from 1.7% in the ’70s to 48% in 2019.

There is further aberration to be found in the pension schemes of the government:

- A government servant qualifies for post-retirement pension after 25 years of service.

- It continues till the pensioner’s death and is then converted into a family pension for the heirs.

- Under the Punjab Pension Rules, the family pension goes to the widow of the deceased.

- After the death of the widow, it can be claimed by the surviving sons not above 24 years of age, unmarried or eldest widowed daughter, or even by the eldest widow of the deceased son of the pensioner.

- If or when no qualifying person from the second generation remains, the family pension is then paid to the eldest surviving son or the unmarried or widowed daughter of the deceased son of the pensioner.

- This peculiar system makes it possible that a government employee in the service of the Government of India at the time of First World War could have a family pension running even today.

What makes matters worse is that the government funds all pension costs through its annual budget; currently, there is no provision for funding pension liabilities.

Read more: ‘Best of times, worst of times’: PTI government completes two-year economic recovery

What to do?

- Eliminate all retroactive increases.

- Remove all family members – only employee and spouse after death.

- No more defined benefits pension but rather defined contribution.

- Funding provisions as is standard throughout the world – both employer and employee must contribute.

- Money to be invested in stock market or long term assets.