In line with its global counterparts, the Pakistan Stock Exchange (PSX) performance has been outstanding since it bottomed in March. The benchmark KSE100 Index touched an extremely oversold level of 27,228.08 points on March 25th, 2020 (CY20TD low) as surging coronavirus cases and lockdown measures triggered a risk-off environment.

Since then, the benchmark has returned 49.6% on the back of a number of factors including, first the strong coordinated policy response by the government (relief package of PKR.1.2tn or 1.5% of GDP which was fully implemented) and the State Bank of Pakistan (lowered key policy rate by 625bps to 7% and offered various incentives to the industry) which provided a floor to the index and resultantly buoyed market sentiments.

Second, the government adopted gradual ease of lockdown restrictions from mid-April to September coupled with additional government measures supporting economic growth (e.g. construction sector package, an agriculture package, incentives/protection for banks as well as lobbying for deferment of debt) brought visibility to an otherwise clouded corporate earnings outlook.

We saw that in this backdrop, many corporates reported earnings in the Sep-Quarter, significantly above market consensus estimates (market analysts under- corrected themselves to properly account for the impact of Covid-19 and the subsequent recovery) with overall earnings up 51%YoY for the KSE100 Index companies.

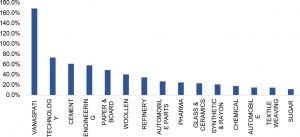

The economy saw an aggressive demand resurface post-government stimulus where domestic cement sales are up 19%MoM in Oct’20 and up 18.7% in 4MFY21, OMC sales are up 6.1%YoY in Oct’20 and ~9% in 4MFY21, while Auto sales have also started reflecting a rebound from its lows. As a result, cyclical sectors (cement, up 61% since late Mar’20) have been the first to bounce back as share prices have reacted before the turnaround in fundamentals.

Three different vaccine trials with an encouraging efficacy rate have signaled a sooner than expected return to normality which is also being reflected in the benchmark KSE100 Index. Overall, better global economic prospects post-vaccine availability has acted as a catalyst for the price performance of global commodities coupled with an improved outlook on exports has triggered a sector rotation back into the laggard heavyweights in Oil & Gas, Banks and Textiles which were negatively impacted by the coronavirus related economic slowdown.

Furthermore, the FATF’s decision to keep Pakistan on its grey list till next February, watering down threats of blacklisting in the immediate term, helped to support the PSX. The government is scrambling to become fully compliant with FATF’s action plan in this regard.

Macro-Economic Environment Supporting Stock Market

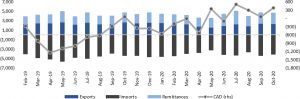

The market performance also reflected the improved macro-economic environment. Take the external side first, the current account (CA) witnessed a marked improvement in the first four months of the current fiscal year, with CA balance recording a net surplus of US$1.16bn (1.3% of GDP) vs a deficit of US$1.4bn (-1.6% of GDP) last year. The key driving factor was workers’ remittances – which grew 27%YoY (around US$2bn higher than last year).

Read more: Will the resumption of IMF program harm or help the economy?

While the authorities may credit themselves for higher flows, various exogenous factors such as unavailability of informal channels and laid-off workers sending back their savings to home countries were at play. This is also evident from regional trends. Almost all our regional peer countries such as Bangladesh, Sri-lanka & India recorded healthy growths in inward remittances. The other important driver behind improved external account position was abnormally higher other current transfers -70%YoY (around US$0.5bn higher than last year) – reflecting potentially higher inflows from NGOs in the wake of the COVID crisis.

Considering the idiosyncratic nature of the increase in dollar earnings (i.e. remittances and other current transfers), the trend would likely reverse going forward, with the current account returning to deficit albeit a more manageable one. That said, the overall outlook is still hazy. On the one hand, we are seeing a massive increase in textile export orders, with order books full for next 4-6months.

Read more: Pakistan’s forex reserves surge as economy makes speedy recovery

Exporters are mulling over expansions following a recent surge in export demand. On the flip side, the job losses in key remittance-exporting countries cannot be ignored. Normalization of the job market in these countries will probably take some time to come back to the pre-COVID level fully. Also, the visa restrictions and job nationalization policies adopted by these countries in response to the pandemic could all weigh on remittances, adversely impacting the CA balance. Further, factors such as historic low-interest rates, trillions in US fiscal stimulus, recovering pandemic-struck economies across the globe, supply chain disruptions, and growing vaccine optimism create a near-perfect backdrop for commodities to rally.

The same backdrop poses a key risk to the external outlook. Just to put things into perspective, a 5% increase in key imported commodity prices from current levels could increase full-year import bill by around US$1bn (~US$0.3bn from oil alone).

The other key risk is the need for higher food imports following the domestic shortage of key staple commodities, which is both because of poor output this year and authorities’ mismanagement. Food imports are already up 33%YoY in the first four months, courtesy wheat imports and rising edible oil prices.

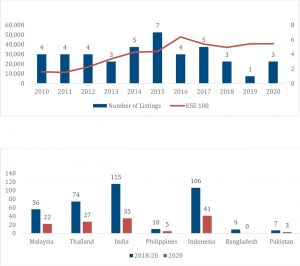

IPOs in Pakistan this year

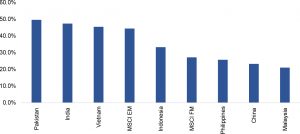

Three companies have successfully raised fresh equity through listing at PSX in 2020, and at least two more are in the final stages of listing, which would probably be listed by the end of this or early next year. While the recent trend is encouraging compared to the last two years, new listings are still abysmally low compared to the regional markets.

Read more: A Locked down Economy: Where Can You Invest In The Midst Of A Storm?

Over the last two years, only seven companies got listed at PSX vis-à- vis 106/74/56 in emerging regional economies of Indonesia, Thailand, & Malaysia, respectively. Uncertain market conditions, high regulatory standards w.r.t financial reporting, governance and other disclosures, lack of corporatization, and sponsors’ unwillingness to cede control are amongst the many reasons behind abysmally low fresh listings.

Foreign investors Activity

Foreign investors have sold net US$455mn in equities this year as risk premiums have heightened due to the coronavirus-related global macroeconomic slowdown. Even though valuations have become relatively attractive, redemption pressures (funds looking at this region have also reduced in size by ~40%) and rotation out of Emerging/Frontier markets have exacerbated the selling pressure.

Like Pakistan, policy response in other global markets (particularly the G-7) has provided a boost to liquidity which been reflected by the surge in the capital markets of developed countries. We expect foreign investors to gradually start building fresh positions in Pakistan early next year as visibility on the vaccine rollout improves and credit markets start taking stock of the sizable debt build-up in private and public sectors in developed markets.

Read more: Manufacturing growth ahead of Fed meeting, revival of US economy threatened by surging coronavirus

In this backdrop, we are already seeing foreign funds and allocators of global capital starting to take a fresh top-down look at Pakistan on the back of expectations that the macroeconomic profile will remain stable (lower external account stress – trade deficit remains under control and inward remittances do not witness a sharp fall – improvement in forex reserves, better debt servicing capacity and Pakistan remains in the IMF program).

Additionally, fund flows should significantly improve in the region overall once the USD starts weakening over the course of the next twelve months. Resultantly, the current valuation gap between Emerging/Frontier (EM/FM) and Developed Markets (DM) should start to narrow as portfolio flows to improve in EM/FMs.

Weak Integration with Global Markets

Akin to its economy, Pakistan’s stock market performance during normal times has largely been driven by domestic political, security, and macro-economic factors. This is partly due to weak integration with the global economy and financial system. With the weak foreign investors’ participation over the recent few years, the performance has been even more dictated by local factors. That said, correlations across the globe tend to move to +1 during the times of ‘black swan or once in a century’ events. The globe stocks move in tandem during such periods, with varying risk perceptions driving the market performances.

Pakistani rupee third-best performing currency in Asia

Sizeable CA surplus in particular and positive sentiment with respect to economic recovery, in general, have manifested into domestic currency appreciation, with Rupee appreciating 4% against Greenback – making it third best-performing currency in Asia. COVID-19 has also played its part, bringing international travel to almost a halt. This has markedly reduced the dollar demand in the open market, pushing the exchange companies to surrender their dollars. This, coupled with enhanced monitoring following FATF mandated tougher regulatory environment, has contributed to the leaner demand for dollar in the open market. Note that the SBP has barred non-filers from operating a dollar account. It has also mandated banks to report dollar deposits exceeding US$1000.

Stock market vs Real economy

The relationship between stock prices and the real economy is complicated. So the criticism that the stock market is not reflective of the real economy is both justified and not. There’s no straight answer to this. The relationship is at best tenuous in the short term. Take recent market performance; the market staged recovery way before we saw an improvement in macro-economic fundamentals. Looking at the early recovery cycle, one can argue there is a disconnect between the stock prices and the happenings of the real economy and ‘the market is not the economy’. But the stocks cannot sustainably perform without tangible improvement in underlying macro-economic fundamentals. Stock prices reflect the macroeconomic environment over the long term.

Umer Farooq is currently working as an Economist/Investment Analyst at AKD Securities Limited (AKDSL) – the largest brokerage firm in Pakistan. He has close to four years of working experience as a sell-side equity analyst, covering Pakistan’s Economy, Textiles, and Steel. Academically, Umer is an ACCA Affiliate and a CFA level III candidate.