By Shahid Sattar and Sarim Karim

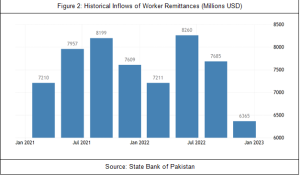

Pakistan is the sixth largest recipient of remittances in the world, with the State Bank declaring a total of $29 billion received in 2022. Remittances play an important role in Pakistan’s economy, contributing 8.99% of its GDP, outpacing the global average of 5.32% (World Bank, 2021). The Pakistani diaspora is also the sixth largest in the world, with migrants located in virtually every continent.

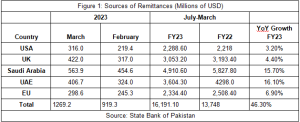

The majority of remittance earnings arrive from Saudi Arabia ($5.7 billion), followed by the United Arab Emirates ($4.3 billion), and the United Kingdom ($2.9 billion). The nation’s earnings outcompete Bangladesh and Vietnam, whose received remittances were $21 billion and $19 billion respectively for the same year. However, these were still below the Philippines at $38 billion and India at $100 billion.

Read more: Future at Stake – Deindustrialization

Understanding the matter better

Pakistan’s remittance earnings have been increasing over time, coinciding with the establishment of the Pakistan Remittance Initiative in 2009 and subsequently increased outreach of banks in the remittance market. In 2021 the Planning Commission recommended initiatives to increase remittances, which focused on making it easier for Pakistani laborers to gain employment abroad. This initiative should be approached with some caution, as little is mentioned about the use of remittances domestically to promote growth. As the nation attempts to expand this inflow, important questions arise, both macroeconomic – its relationship to economic growth, investment, and trade balance. And also microeconomic – its role in determining consumption patterns and labor supply.

The existing research is divided on whether remittances have a net positive or negative impact on Pakistan’s political economy. What can be said with certainty is that the relationship between remittance inflows and long-term economic growth is highly heterogeneous. While remittances definitely increase consumption amongst recipients, that consumption does not necessarily translate into long-term, non-volatile growth. The State Bank of Pakistan’s (SBP) empirical analysis shows a positive correlation between remittance growth and economic growth.

The findings indicate a 1% increase in remittance flows results in a 0.15% increase in GDP growth as of 2017. However, more recent econometric analyses in 2020 from the World Bank, Asian Development Bank (ADB), and independent research from economic institutes, have all shown that increases in remittance flows actually decrease economic growth for Pakistan. Perhaps this contradiction can be resolved through the one conclusion all the literature holds in common – remittances have a negligible negative impact on investment.

Read more: Is Pakistan moving towards a dollarized economy

This conclusion is supported by the fact that nations that have consistently shown a positive link between remittances and economic growth, such as India and Singapore, have placed considerable resources into channeling remittance flows towards investment into the industry. Pakistan must shed its reliance on remittances because while they may work as a short-term tool for poverty alleviation, they entail a host of negative externalities that hurt the nation’s long term growth potential.

Research conducted in 2008 by the Social Science Research Network and in 2016 by the International Journal of Organizational Leadership has found that remittances do contribute to unemployment. Even when migration flows are excluded from the equation, remittances decrease incentives for labor force participation among recipient households. Furthermore, a slight linkage exists between remittances and decreased working hours. Implying that those households which do work, have incentives to work for fewer hours knowing that wages can be substituted.

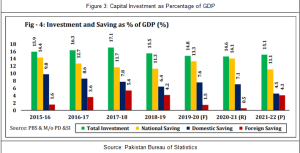

The only caveat being that when remittances are directed towards productive investments, such as small-scale enterprises, then unemployment decreases. However, the consumption patterns in Pakistan do not support this argument. Pakistan’s average ratio of investment to GDP has been 17.2% since 1960, one of the lowest in the world, standing at 151 out of 175 countries. As of June 2022, the ratio of investment to nominal GDP was 15.2%. Compared to regional competitors, Pakistan’s savings are less than half of India’s (30.2% of GDP) and Bangladesh (36% of GDP).

A limited amount of research under the State Bank has shown that remittances are mainly used to acquire consumer durables and plots. Research by the ADB has shown that remittances are majorly utilized for consumption as well. Increased consumption is generally favourable, as it stimulates demand and generates employment. However, the larger pattern is one of dependency. Both at the household level, where remittances depress labour-force participation, but also at the policy level where the state is less motivated to promote job expansion. Therefore, though remittances can help alleviate poverty, they cannot eliminate its structural determinants. Unless they are paired with long-term growth through promotion of industry, remittances only exist as a short-term solution for the nation’s balance of payments crisis.

While increased consumption on its own is beneficial for economies, remittances pose an opportunity cost that must be highlighted. Remittance inflows lead to exchange rate appreciation, decreased trade competitiveness, and a deteriorated balance of payments. The simplest way to understand this process is to envision remittances as a type of capital inflow. Economies become vulnerable to Dutch disease when there are large, uncontrolled surges of capital inflow towards a particular sector. Dutch disease is characterized by a rapid increase in one sector at the cost of other sectors. Firstly, the income shock and subsequent spending increase can drive demand-pull inflation. For many developing countries, prices in tradable are determined largely by international markets.

However, the non-tradable sector is relatively more influenced by domestic demand. Pakistan already experiences higher inflation in the non-tradable sector (SBP, 2019) compared to tradable and the ‘spending effect,’ of remittances exacerbates that. The consequence of this demand and price shift is more factors are allocated from tradables towards non-tradable, otherwise known as the ‘resource movement effect.’ Therefore, increased factor prices, decreased tradable output, and overall increase in goods prices results in an appreciated currency. Ultimately decreasing the competitiveness of export-oriented sectors, and widening the current account deficit.’

Read more: Sustainable water management in Pakistan’s textile industry

Such a phenomenon has been witnessed in many Latin American economies

Similarly, a study in 2006 found that Pakistan’s exchange rate experienced growth in accordance with increased remittance inflows (Hyder and Mahboob, 2006). This implies that there is a tradeoff between reliance on remittances and export-led growth.

Remittances also share a positive relationship with rising import bills. Studies conducted in 2007 and updated in 2019 found a significant and positive correlation between rising remittances and rising import bills (Hussain and Yan, 2019). These results align with investigations by Hernandez and Toledo on eight Latin American countries, where it was found that remittances increase imports. This creates another avenue towards Dutch Disease, as a shift in the balance of trade toward imports weakens export competitiveness. However, this dynamic can be mitigated if resources are moved towards raising productivity in tradable.

Given the tenuous relationship between remittances and economic growth, it would help to explore how remittances can positively impact investments. As previously stated, remittances have a negligible impact on investment growth in Pakistan. Research conducted in Bangladesh, which exhibits similar patterns of consumption and investment from remittances, has shown a non-linear relationship between remittance flows and economic growth in the long term (Hassan, 2017). In other words, remittances have diminishing returns and can eventually hurt growth potential in the long term if incentives for investment aren’t established. Conversely, there may be a reverse causality, where better economic conditions are the precursor for remittance growth to translate to GDP growth.

In this regard, India stands as a positive example. Investigations from the World Bank and International Journal of Economic Policy Studies, have shown that despite being the largest receiver of remittances globally, India has sidestepped the issue of dependency and translated remittance growth into economic growth. This is due to the creation of financial infrastructure orbiting remittances specifically.

Read more: Barriers to renewable energy transition for Pakistan’s textile industry

The Reserve Bank of India has pushed for the proliferation of microfinancing, electronic banking, and community financing schemes especially in rural areas. The Ministry of Overseas Indian Affairs also launched a series of schemes in 2009 that incentivize the diaspora to invest in Indian development programs with generous interest rates on remittance-linked loans. Similarly, El Salvador’s Banco Salvaderno offers loans of up to 80% of the amount received via remittance. This motivates households to engage in capital accumulation, driving growth at the macro-level. These programs all exist in tandem with projects that increase access to banking and financial services.

Pakistan can employ similar strategies to make productive use of this resource. Firstly, the government should invest in expanding financial accessibility. The State Bank estimates that 53% of the population is financially excluded. Thus, over half the population is unable to engage in formal investment. Making bank accounts easier to open, introducing e-banking, and expanding rural access can all mitigate this problem. Secondly, transaction costs need to be reduced to make full use of remittance inflows. There is considerable variability in costs for sending remittances through different countries. For example, sending money from Kuwait has a 1.66% cost but doing the same from Singapore has a 12.43% cost (UNDP, 2021). This decreases the potential earnings based on where the migrant is located.

Similarly, there is variation based on the medium of transaction

There is no standardized fee amongst banks facilitating transfers, with some charging a fixed rate and others using a percentage system. Money Transfer Operators (MTOs) are also a source of inconsistency, as their integration with banks is still relatively low. There is also the issue of regressive transaction costs, as it is 39% pricier to send $200 rather than $500 (UNDP, 2021). Data from the International Growth Center found that 43% of migrants are employed as low-skill labour in the Gulf states, and send small amounts in the range of $200 back to their families. When earnings are already low, marginal propensity to save is decreased. These transaction costs restrict existing inflows from being used to their full potential. Thirdly and most importantly, the government must create incentives for investment.

Read more: The Snake Bites Once Again – Energy

Diaspora financing is a growing and innovative field of development economics. Policy recommendations and tools of diaspora financing are diverse and worth exploring for Pakistan. These include capital market instruments based on remittances in India and East Africa. Remittance-linked loan packages advertised towards the recipient can capture their interest, as is done in India. Similarly, Ethiopia and Kenya managed to accumulate $400 million and $154 million respectively via the issuing of sovereign bonds targeted towards remittance senders. Mexico was particularly innovative with its 3*1 and 1*1 financing scheme. In the 3*1 program, state, municipal and local governments would match the funds sent by remittances to finance infrastructure projects. Resulting in 31% of road infrastructure and 20% of energy infrastructure being aided by remittances.

Under the 1*1 scheme, migrants could provide a business plan to apply for a matching three year loan. Instead of repaying the loan to the local government, part of their remittances were channeled toward the 3*1 infrastructure development projects. Other programs involved matching pre-existing enterprises looking for investors with either remittance senders or recipients, offering generous interest rates for those who chose to invest. Pakistan can employ similar financing schemes and direct remittances towards exporting industries or infrastructure that aids their competitiveness.

Remittances are and likely will remain a resource for Pakistan. However, if the government continues to use this inflow as a crutch, the gains will diminish. Instead, Pakistan should utilize remittances to promote investment into export-led industrialization. This would draw in foreign direct investment, expand employment, and reduce the current account deficit on a sustainable basis. The panacea to Pakistan’s balance of payments crisis has always been and remains export-led growth.

Mr. Shahid Sattar, now Executive Director & Secretary General of All Pakistan Textile Mills Association (APTMA), has previously served as a Member Planning Commission of Pakistan and an advisor to the Ministry of Finance, Ministry of Petroleum, and Ministry of Water & Power.

Sarim Karim is currently an internee researcher at APTMA, with a bachelor’s dual degree in Economics and International Relations from Hobart and William Smith Colleges.

The views expressed by the writers do not necessarily represent Global Village Space’s editorial policy.