The United States is the driver of the global economy with its dollarized global financial infrastructure. Currently, the entire western media machine is entirely focused on the war in Ukraine. But something significant is taking place inside the United States which has not received its due attention.

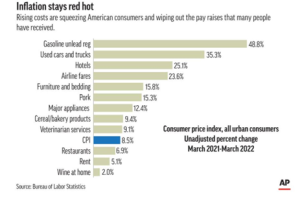

Inflation has been a global problem, including in the United States. United States Bureau of Labor and Statistics reported the inflation to 8.5% in March 2022, which is the highest increase since 1981 on year on year basis.

Read more: US economy shows meek recovery despite Trump’s claims

Many experts have even questioned this figure as the rise in the price of petrol, food, housing, etc., has been more than 20%. Hence the real inflation could be well above 20%. US consumers have experienced even higher prices than 20% in specific sectors. March was also the first month after the Ukraine War. Russia is one of the World’s largest energy exporters, and both Russia and Ukraine are significant suppliers of wheat and other grains.

This skyrocketing is multifactorial. United States has undergone a brutal COVID-19 Pandemic killing almost a million Americans. Federal Reserve has recently stopped its quantitative easing program (money printing) and is about to start quantitative tightening, which will go up to $95 billion per month.

Money printing has reached historic levels in the United States in the recent past

To understand its magnitude, the total M1 money supply (total paper notes) in circulation at the start of the COVID-19 Pandemic was 4.7 trillion dollars, and in March 2022, it was $20.7 trillion.

The United States roughly distributed $6Trillion during the COVID-19 Pandemic, described as helicopter money, while stopping most of its productivity. How this money was distributed also has raised many troubling questions as the actual amount that reached the ordinary Americans was much smaller than what was delivered to corporate America. This money ended up in the stock market, real estate, and cryptocurrency resulting in the “great American bubble” among all asset classes. Financial analysts have suggested that some of this money might also have some exposure to emerging markets.

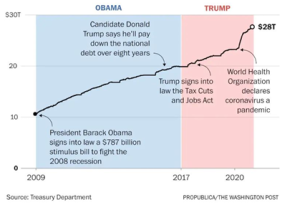

The United States is a debt economy. The national debt almost rose by $7.8 Trillion during Trump’s presidency and currently stands roughly at a whopping $30 Trillion.

During the great financial crisis of 2007-2009, US debt was $9 Trillion with a debt to GDP ratio of 62%, which rose to $11.9 Trillion in 2009 and a debt to GDP ratio of 82%, accounting for all the bailouts. In 2021, US debt stood at $29.6 Trillion with a debt to GDP ratio of 124%.

Total non-financial debt was $33.5 Trillion at the start of the great recession (2007-2009), which was 227% of the GDP, which has risen to $65 Trillion in 2022, which is incredibly 270% of the GDP. All of these numbers are mind-boggling.

United States Federal Reserve does not have many choices for course correction in 2022. More money printing is no longer an option. Continued Money printing could cause runaway inflation or hyperinflation and remind all Americans of Germany’s Weimar Republic, where hyperinflation reached 29500% in October 1923. Federal Reserve has already started quantitive tightening (taking money out of the system and burning it) and raising interest rates to curb inflation with no guarantees that it will work. Most economists predict stagflation in the near future (persistent high inflation with high employment in a stagnant economy). But some have indicated the possibility of “depression” in the US economy.

US stocks have reacted terribly to these recent rate hikes, and there has been a global blood bath in most stock markets in the last week. But, unfortunately, the worst is yet to come. The fat lady has just started to sing.

Another sign of a weak US economy and impending recession and financial trouble is an inversion of the 10-2 treasury yield curve. This inverted in March 2022 since September 2019. The 30-2 treasury yield curve also has inverted in March 2022 since 2006. Such inversions mean that the economy is fragile and headed for a recession.

Read more: Manufacturing growth ahead of Fed meeting, revival of US economy threatened by surging coronavirus

But this would be no ordinary recession. The inflation is 40 years high and displaying no sign of stopping. The non-corporate and corporate US debt is at an all-time high, with Federal Reserve burning up to $95 billion per month. All asset classes in the US are in a gigantic bubble, and we have a war in Ukraine raging on. Federal Reserve has also started to raise interest rates. This could equate to the US economy falling from a financial cliff.

In 2007 the global economy was rescued by the Chinese Growth

Unfortunately, China is also not in the same position anymore and has built a debt problem. However not as frightening as the US debt.

The gigantic bubble is about to burst. The United States has been “poking the bear” testing how much money Federal Reserve can print without consequences. The bear is fully awake and in attack mode. This will not be pretty, and not everyone will survive this financially.

All of this means that there will be a liquidity crunch. Moreover, there is a high likelihood of capital outflow from emerging markets to developed economies depending upon their exposure to this insane money printing.

This will also mean that there will be much fewer IMF bailouts and much more onerous conditions. Pakistan might be the first causality of the credit crunch if the decision-makers in Islamabad don’t wake up soon and smell the coffee.

Read more: US Economy future uncertain, warns Federal Reserve

There is a realist risk of default with widespread public unrest on the card for the foreseeable future.

The author is a graduate of the University of Oxford’s Said Business School and currently works as Faculty at Brown University in the United States. The views expressed in the article are the author’s own and do not necessarily reflect the editorial policy of Global Village Space.