Najma Minhas Global Village Space Managing Editor spoke with Zaigham Mahmood Rizvi, Chairman of the Prime Minister’s Task Force on Housing. He is responsible for setting out the ground work for one of the key initiatives of the PTI government’s agenda. This will not only fulfill its promised 5 million houses for the middle and lower-income segments in the next five years but will also play a key role in creating the promised 10 million jobs in the next five years. Mr. Zaigham Rizvi is currently the Secretary-General of Asia Pacific Union for Housing Finance (APUHF) and earlier has served as Chairman and Managing Director of House Building Finance Corporation.

Pakistan’s population in 1965 was around 50 million. Today it is more than 208 million, which means it has increased by four folds. But the supply of food, clothing and shelter has not grown proportionately. While, people have managed food and clothing [on their own], housing is unmanageable for them.

This is why Zulfiqar Ali Bhutto made housing a part of his political slogan of Roti, Kapra, aur Makaan in 1971. PM Gilani, in his 100-day agenda, announced they would build 1 million houses every year, which would make up to 5 million in 5 years, but nothing was done. Then-Prime Minister Nawaz Sharif announced that his government would build 0.5 million houses every year, which would have made up to 2.5 million houses in 5 years.

This also went unachieved. Two essential things were missing in both cases: the lack of an administrative setup and an institutional framework. The disparity between the rich and the poor has created oppression in terms of housing development.

The rich do not need somebody to finance them and the middle-income class waits and looks for affordable locations to build a house. But the lower end of the population need financing and low-cost schemes to own a house, and this is exactly where the state intervention is essential.

Najma Minhas: Past governments also announced housing schemes for the poor. Why couldn’t they achieve anything?

Zaigham Mahmood: I personally believe there was a lack of sincerity of purpose towards the cause. For instance, Prime Minister Nawaz Sharif set up a task force, with five working groups. I came back from the U.S. and volunteered to work with them and we worked a lot. But then none of the recommendations by the task force was implemented.

After November 2013, the government never even talked about housing. I wish they had done something; the next government would have found it easy to take it forward. Prime Minister Imran Khan seems to be different. He sees housing not just as shelter, but also as a direct employment generator and as a multiplier in the economy in terms of the 42 downstream industries – construction, material and other – industries.

So Imran is committed that through one essential sector, a lot can be done for the overall economy. For example, $1 invested in the housing means $1 invested in the construction sector, which is multiplied by 8 as the employment multiplier; this is the case with countries with more mechanized construction. In countries like Pakistan and India where the construction is mostly done using unskilled labour, the employment multiplier is much higher.

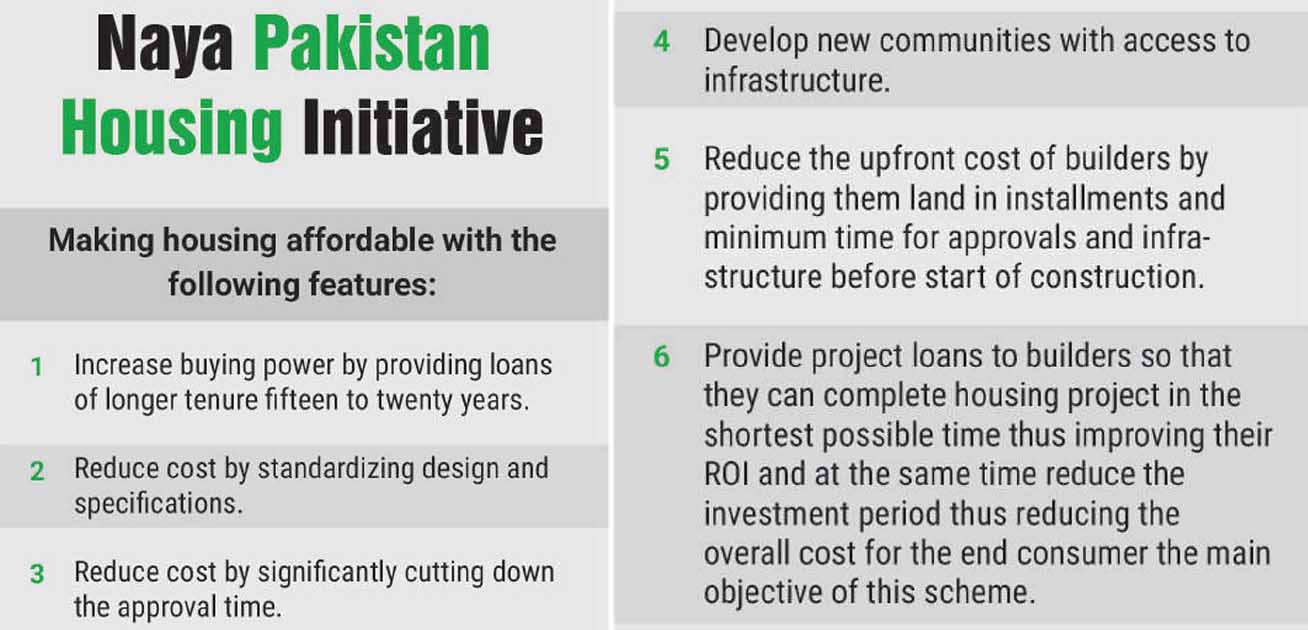

This is why PM Khan has created this taskforce. We have already had a total of 12 meetings and each time he is pushing for things to be sped up. Housing development is not going to happen like a miracle. An institutional set up with housing authorities at the federal and provincial levels is needed to promote low-income housing.

Read more: GVS exclusive interview with Fereeha Idrees

Najma Minhas: Have you conducted an international country analysis as to the best model that could be followed in Pakistan?

Zaigham Mahmood: Yes, we have done that. We can learn things but we cannot do them the exact same way. Every country has its unique land issues, legal issues, and processes of approvals. The Indian model is quite similar to Pakistan, but if you look at the much-lauded Singapore model, it’s very different to the ground realities present in Pakistan.

In 1967, Singapore passed the land acquisition act, meaning the entire land was acquired by the state. Then all this land was available to the state for developing public housing in Singapore. Within two years an entire institutional set up was created. Three things happened there: the housing development authority was set up; the financing side was instituted; the land was acquired.

In Singapore 90% of the population now owns homes. However, for us the model that is most appropriate to follow is the Indian model, because of similar socio-economic and cultural background and land revenue systems. However, India is more prepared in terms of an institutional setup, which Pakistan currently lacks.

The housing program launched by the PTI government focuses on urban housing, rural housing and peri-urban housing. For the first time, a program is being launched that also focuses on rural housing.

Najma Minhas: Do you think the 5 million number of houses the government is stating it will build in 5 years, as a realistic or an idealistic number?

Zaigham Mahmood: When you look at the history and the past housing policies, it seems a very challenging target. But when something similar has not been done previously, it is as much a challenge as an opportunity. For example, if we look at rural housing, we plan to construct 20 lac houses in the rural area – 40% of the total target.

The housing task force has been around for roughly two months and one area we have worked on extensively is rural housing. We have involved the academia and we are setting up housing research centres in universities. Students were sent to villages to study the rural population’s lifestyles and develop appropriate housing models.

Punjab alone roughly makes up two-thirds of the country’s population, we are working on a model where we develop 50 houses in each village, we have 25,500 villages in Punjab, which means 1,275,000 houses only in Punjab. Then there are of course similar projects in Sindh, Baluchistan and Khyber Pakhtunkhwa.

All these houses will be proper cemented structures made from scratch. From a cost perspective, it’s not much, because the land is available free of cost in the villages. Once the housing program consolidates, we will also help villagers make existing houses better.

Read more: ‘Pakistan sixth largest country in the world cannot be ignored by…

Najma Minhas: Will these model villages include electricity, gas and other utilities?

Zaigham Mahmood: No, an ideal model cannot be created all at once. These model villages will be three to five acres of land, with proper houses, designed in a simple manner, but these houses will have an inside kitchen and toilet, 2 bedrooms. As we move gradually ahead, other ideas such as solar panel housing will also be incorporated.

Najma Minhas: What is your definition of a house?

Zaigham Mahmood: As of now we are defining houses in terms of cost and the area. We are talking about 120 sq. yards up to 126.465 sq. yards (5 marla). Covered area will be around 700 sq. feet. And the cost we are talking about is 30 lac (upper limit in all forms of housing).

PKR 5 billion has already been allocated to the project. The PKR3 million is the upper limit of how we will define low-income housing. However, there will be all types of housing, some for 3 lac, some for 5 lac, and some for 15 lac and so on. Beyond the 3 million, we define middle-income housing.

Najma Minhas: How much do you think it is going to cost the government to build 5 million houses?

Zaigham Mahmood: This is something I would rather avoid saying because this depends on how many houses we make for 3 lac, 5 lac, 10 lac, etc. Sometimes, what happens is that people come on the media and simply multiply 5 million houses by PKR 3 million and conclude that it’s impossible to build.

We do have cost estimates for planning purposes, but we are not stating these estimates publicly yet. The State Bank is working on the house financing element. Some people want to pay 20 percent down payment, while others want to pay a larger amount up front.

People have different mindsets about how to pay off their mortgages; some want Shariah-compliant loans, others want to avoid loans altogether. Some prefer mobilizing money through committees, while others sell their jewellery or borrow from relatives.

The culture is such that most people don’t like borrowing large amounts. So I personally believe that up to 50 percent of people, who say buy a 12 lac house, will put down at least 5-6 lac from their own resources as a down payment.

Read more: Explaining Pakistan’s media: GVS exclusive interview with Yousaf Baig Mirza

Najma Minhas: Can you explain the changes you plan to make in terms of the regulatory framework to help build more low-cost housing?

Zaigham Mahmood: There are a couple of areas which we are addressing, including fiscal incentives to banks, which will encourage banks to provide housing finance to low-income people. This housing portfolio income will be taxed at a much lower rate as compared to the normal banking income which is taxed at 35 percent.

If this tax is reduced to 20-25%, banks will have a higher incentive to enter this market. Similar measures will be introduced to encourage banks to finance developers in construction side financing.

Najma Minhas: Will you also give banks a target on the loan portfolio?

Zaigham Mahmood: The State Bank is also working on setting targets on housing loan portfolios for the banks, for this preferred sector. There are two or three models for this. Under preferred sector lending or direct lending, banks may be asked for 5-10% to be given out in loans in this segment.

Or the State Bank can give the commercial banks exact targets under the regulated targeted approach, and in return, banks will get incentives such as better capital adequacy ratio, etc. Banks will soon be advised on these measures.

Najma Minhas: The average person’s salary in Pakistan is about PKR 20-25,000 a month. What have you defined to be low income in terms of the housing scheme? Is it defined in terms of housing provided or in terms of salaries received by the individuals?

Zaigham Mahmood: We have not done it in terms of an individual’s income but have used the cost side for defining low-income housing. Why? Because in Pakistan and in most of the region, the husband earns the family income but often the wife and children are also working.

In addition, they often also have informal sources of income so we have clubbed all these incomes to assess the total household income. At the moment Pakistan’s culture is that only salaried income is considered eligible for assessment for loans by banks. However, we will use whatever the total household income is, and they can prove it from different sources.

Najma Minhas: So the way you’re going to encourage these people to take mortgages is through the banks?

Zaigham Mahmood: Naturally, the financing side to buying the houses will only be through banking services; through banks or other specialized housing financing institutions. We do have one institution called the House Building Finance Corporation, but over the years its performance has deteriorated and its presence in the housing finance market is very small. We are trying to restructure HBFC, but more than that the government is going to incentivize the private sector to develop more specialized housing finance institutions.

Read more: GVS exclusive interview with Imran Khan; his vision and his priorities.

Najma Minhas: How will you incentivize the banking sector to give cheaper mortgages? Interest rates are extremely high in Pakistan. Has any work been done on how to subsidize mortgages for the poor?

Zaigham Mahmood: Interest rates at this moment are high, but at this moment I cannot say that we will be subsidizing interest rates, as that would not be the sustainable thing for the government to do.

Interest rates are driven by economic management of the economy and the markets are driven by the economic policy. Good financial measures are being taken by the finance minister and I expect interest rates to stabilize at lower levels in the next few years.

Najma Minhas: Is it something you are thinking about in the future?

Zaigham Mahmood: Not really. The problem is when you give interest rate subsidies, it’s not that easy. Loans are for 20-25 years. How can a government ensure that the people are provided interest rate subsidy for the next 20-25 years?

How can the banks make an assessment about the decisions of future governments? A model of interest rates subsidy was considered in the past too, but the banks asked that the subsidy be given to them upfront for the next 25 years. These are the technical issues in this market.

Najma Minhas: The Indian government is actually using this subsidy model. They are subsidizing interest rates for low-income people. They have set a level of about 6.5%.

Zaigham Mahmood: India is doing it but it is only guaranteeing it for the next 2-5 years of the loan. Also, they are doing it for very low-income housing of up to Rs6 lac or so. Our economic condition is very different from India, so I would not like to recommend something which economic managers at this moment in time may not be able to sustain.

Read more: Set on a Journey of Undefeated Dreams – Interview with APS…

Najma Minhas: What is the government doing on the legal issues that often make mortgaging difficult for banks and developers such as land titling?

Zaigham Mahmood: A Naya Pakistan housing authority will be announced shortly which will be responsible at the centre for execution of the housing policy. We will also have housing authorities in the provinces because land is a provincial subject. In Punjab, there is already an authority (Punjab Housing and Town Planning Agency) that’s doing a very good job.

Were they don’t exist, the provincial governments will have to set up a new entity, or improve the existing one to work better. The second thing we are developing is the Real Estate Regulatory Authority. At the moment there is no regulatory body for real estate building in Pakistan.

Third, we are working further on the foreclosure laws. Section 15 of FIRO has already been revised which has made it very effective, but at the same time, our task force is working with the law division to bring out more successful housing specific foreclosure laws.

At the moment if you give a loan to somebody and they don’t pay back then I am stuck. I cannot give that amount to someone else. So that one person, the defaulter, got the benefit but he damaged the benefits of others. So foreclosure laws and recovery of money laws have to be very effective, on which we are working. Then we are also looking at tenancy laws to see how these can be improved.

In this case, titles will not be an issue because most of the land which will be developed is either federal or provincial government land or the developers who have bought land from the market with titles. The Real Estate Regulatory Authority will ensure that all the developers under this scheme, availing government incentives, will be registered with RERA and it will ensure that the developers have the legal titles before any work starts.

Najma Minhas: Under current scenarios, the developer runs around getting up to 19 NOCs to develop private housing scheme and needs to grease palms to ensure everything is done on time. Will RERA ensure that there is a specific time in which this has to be completed?

Zaigham Mahmood: There is definitely a timeline to get better administration, but there are many approving authorities when you go for development of land, like KDA/CDA, etc. utility companies, water companies and all that takes a lot of time for the developer before his project is launched.

We have asked the provincial governments to ensure that we develop one platform where this can be done easily. RERA will ensure that the developer doesn’t go to market unless and until he has all these clearances. The one-window facility is where the developer will go and submit his application and this will be moved to all the authorities concerned to get requisite approvals.

The provincial authorities will set up the one window facility according to their own local institutional setups. There will also be some mechanism to ensure that delivery time is reasonable. In India, they have one office where all the relevant departments sit together to facilitate the real estate developers.

Read more: Interview with Marvia Malik – Pakistan’s first transgender anchorperson

Najma Minhas: How will you incentivize the private sector to develop low-income housing schemes, estimated profits on the large housing schemes are quoted in the region of 200-300% as compared to 15% on low-income housing?

Zaigham Mahmood: This is a question which is generic to many countries – Pakistan, India, and Malaysia. India has around 30-35 very large developers. They have learnt over the years that they need to treat low-income housing as a high-volume, high-turnover and low- margin business.

High-end houses have a very low turnover but have high-end margins. But that market is maturing now. So what is happening now is that these developers are automatically being incentivized to go into low-income housing segment?

At the moment in Pakistan, we don’t have that kind of large scale developers. In Punjab, the culture is horizontal development of housing and slightly higher rise development in Karachi. Not many developers can do really big projects – 100 acres to 500 acres of habitat.

Najma Minhas: Has the government decided whether it will encourage high-density, high-rise development or lower-density horizontal development? You talked about Singapore earlier, most of their public housing is high rise. In fact, many economists and urban planners now also recommend this as being a better way to create a thriving community, homes interplayed with business and industry units.

Zaigham Mahmood: It’s become a naturally developing phenomenon. In Lahore, we never saw high-rises in the past. Now you see many. Even the low-income habitat being developed like in Karachi’s Khayaban-e-Ameer, they themselves have decided that they will also be developing high rise.

So the model we are working on as I said is that 50% plus will be the low-income sector housing, 30% plus will be the middle-income and 20% will be the higher-income segment housing because we would like to develop a mixed habitat and mixed communities.

This is very important because if we only develop one kind of community then the economic prospects of the area will be downgraded. High-rise has a different definition in this country. Low-income segments culturally don’t like high rise buildings.

They like walkable apartments. Ground plus one or two floors will be created, maybe three maximum, to ensure that we don’t need elevators. However, we will be the standardizing size of the doors and windows and the tiles, so that manufacturing will be easier and overall cost cheaper.

In every habitat, there will be a commercial area, which may vary in size from 5 percent onwards. The housing authority will be clearing any housing project eligible for all the incentives the government will be announcing.

Once a project is eligible for those incentives such as the developer, community and mortgage incentives, then they have to agree on what the government’s basic guidelines are. And that’s where the housing authority will clear them according to those standards.

Najma Minhas: Are you going to try and introduce sustainable and green housing, with things like solar panelling?

Zaigham Mahmood: At this stage, no on the solar panels due to cost, but green housing, our architects tell us, includes maximizing the use of the air or sunlight – this we will try and incorporate.

At some stage, in rural areas, we might incorporate solar panels in the village housing, but in our urban housing we will ensure that the design of the structure will maximize the wind and sun elements and if this is complied with, it will make housing 25-30% energy efficient.

Read more: Security Council Expansion; opportunities & risks: Exclusive interview with Ex-Brazilian Foreign…

Najma Minhas: Where will you get your land from?

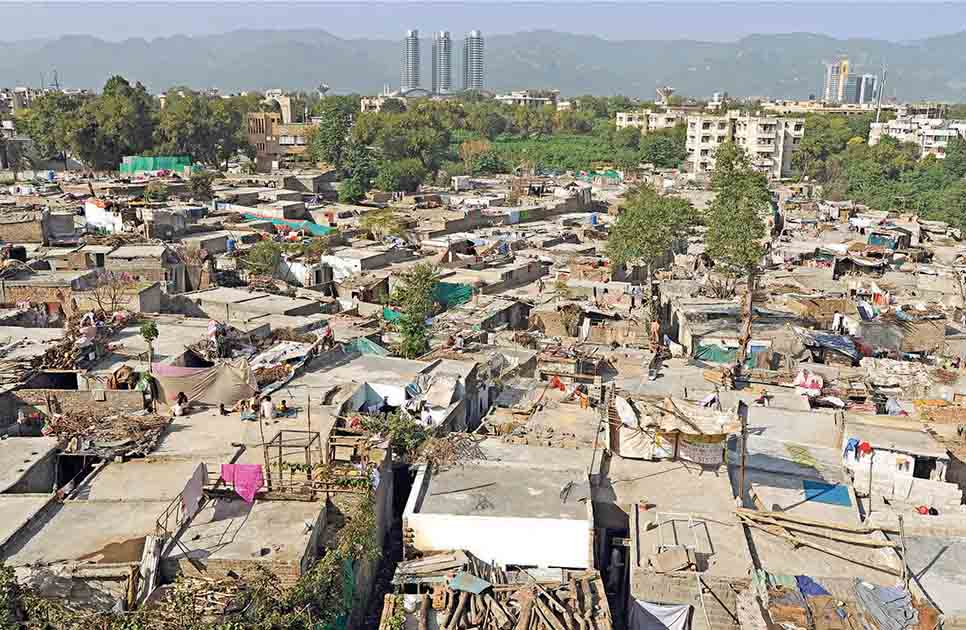

Zaigham Mahmood: The land is where the housing starts and this is where the issue was. We discovered that a lot of land is being grabbed by illegal habitat and slums development. Over 55% of Karachi is illegal habitat such as slums. That is not private land; it is state land, which has been occupied by land grabbers.

For example, the Punjab government is already doing a survey; they have huge parcels of land. The federal government has land and railways has lots of land. Evacuee Trust Property Board also has lots of land all over the country which if not used will also be grabbed. Slums are the most inefficient use of land, as horizontal housing colonies benefit only a few.

Najma Minhas: Will the land being recovered in anti-encroachment drive be used for housing?

Zaigham Mahmood: I am not sure if that is the land where you develop large habitats. These are small [pockets] here and there. For example, Karachi’s Empress Market area has been recovered, but it will be used to restore the original culture of Empress Market. At other places, the recovered land is being used for widening the streets.

Najma Minhas: Have you put any estimates on the number of jobs that you think will be created as a result of this?

Zaigham Mahmood: We think that if we could achieve this target on housing then we should be able to meet the target of ten million working opportunities overall for five years. This depends on the technology used and so on.

Najma Minhas: When do you realistically see the first project getting off ground?

Zaigham Mahmood: I would say hopefully the first project would be in Punjab, about 3-4 cities. More will be coming definitely, maybe somewhere in the first half of February.