United Nations, adopting “Universal Declaration of Human Rights”, in 1948 had stipulated that housing is a fundamental need for a family unit. But seven decades after the country’s independence from British India, owning one’s own house is still a distant dream for most Pakistanis from low- and middle-income groups. The country’s yawning gap between the demand and supply of housing units has been steadily widening. Though reliable statistics are hard to obtain, yet most estimates point out that an accumulated shortage of around 10 million housing units is ballooning by almost 400,000 more each year. Shortages are compounded by increasing house prices turning the issue into a national challenge of gigantic proportions that is multiplying slums, increasing the political divide, and causing national instability.

Read More: Pakistan’s Failure to promote Low-Cost Housing? A Historic Overview

Several governments, since 1947, have attempted different solutions to meet the housing challenge, but these were mostly half-hearted efforts without a clear vision, comprehensive plan, or determination. The emphasis of the current government on housing finance is a key pillar of its social and economic agenda, government’s policy initiatives including implementation of foreclosure laws, persuading banks to keep 5% commercial loans for the mortgage market, SBP markup subsidy scheme, subsidies through Naya Pakistan Housing and tax incentives for developers – have for the first time created hopes for a sustainable housing market for low-income segments of society. It is this enabling environment that now provides House Building Finance Company Limited (HBFC) an opportunity to play a larger role capitalizing upon its legacy of seven decades, its extensive experiences, and its unique strengths.

HBFC: First Mover of Pakistan’s Housing Finance

In July 2007, it was restructured as a limited company and its assets and liabilities were taken over by the new reorganized HBFC. The State Bank of Pakistan (SBP) and Government of Pakistan (GoP) jointly hold the capital of HBFC with 90.32% and 9.68% shares respectively. HBFC’s governing vision is to be the prime housing finance institution of the country, providing affordable housing solutions primarily to low- and middle-income groups of population by encouraging new constructions in small & medium housing (SMH) sector. And its mission is to be socially responsible housing finance institution.

Read More: What are the issues with Pakistan’s housing market! Expert Views

HBFC: Unique National Institution with local strengths

HBFC being the first public sector specialized mortgage finance institution in Pakistan has developed certain unique strengths which distinguish it from the commercial banks. With branch network across 48 cities, it covers around 80% of the “Bankable Urban Housing Markets” across the country. Unlike commercial banks that primarily sell depositary relationships, HBFC thrives on deposit accounts and maintains mortgage portfolio in all cities. This experience of seven decades, of extending housing loans across small to moderate size towns, has converted HBFC into a financial institution of national reach with local strengths. HBFC divides the country into three zones: North, South, and Central. Sindh and Baluchistan form the south region is South, Punjab falls into Central Zone and North consists of areas north and west of Rawalpindi extending into Gilgit, Hunza, Chitral and it also covers AJK.

Biggest challenges in Pakistan’s housing finance are “title verifications” and “title transfers” and HBFC officials have over decades dealt with diverse administrative setups, local courts and tribunals, that apply different laws, interpretations, and conventions to the issues of title. Today this legacy and experience is HBFC’s unique strength over standard commercial banks that were never active in low-income housing market and don’t understand the challenges. HBFC also encourages female borrowing to prevent gender discrimination and lend financial support. And it is no mean achievement that every fifth borrower at House Building Finance Company Limited is a female.

HBFC also serves the high-end market and has inked several MoUs with some of the leading companies of Pakistan including Byco Petroleum Pakistan Limited, Ismail Industries Limited, Descon, Lucky Knits (Pvt) Limited, IGI Life Insurance Limited, Pakistan Security Printing Corporation (PSPC) and Civil Aviation Authority (CAA) to name only a few.

Read More: Why the Naya Pakistan Housing Scheme is a game changer

Mera Pakistan Mera Ghar Scheme (MPMG) – HBFC’s Role

House Building Finance Company Limited – given its legacy, reach, experience, and strengths – is thus uniquely positioned to seize the opportunities in the low-income housing market especially after the launch of the government’s markup subsidy scheme, “Mera Pakistan Mera Ghar (MPMG)”. HBFC’s footprint is so entrenched in this low-income housing market that State Bank of Pakistan’s data in end October 2021 revealed that out of the Rs. 18 billion disbursed in housing market, till that point, 7% came from HBFC – even though HBFC represents only 0.1% of country’s financial system. Earlier end 2019 data showed that out of a total of 60,000 housing loans that currently exist on books, almost 40,000 (or 66%) have been extended by HBFC. Given its focus on low-income housing, size of these loans’ ranges from Rs. 1 million to Rs. 30 million; however average loan size is around Rs. 3 million.

During 1980-90’s, HBFC was considered the sixth major financial institution along with the big five (HBL, NBP, UBL, MCB and ABL). With new opportunities in housing market, it aims to reclaim its leadership position in the mortgage finance sector – when its name was synonymous with family house construction. Now inspired by Prime Minister’s vision and under a new management, House Building Finance Company Limited (HBFC) has been working on designing solutions that directly address public’s housing finance needs. HBFC has fairly covered the accessibility part of the challenge by expanding its network of branches throughout the country. Moreover, it has been imparting relevant knowledge and skills to its servicing staff in order to make the consumer experience more meaningful.

Read More: General Anwar Ali Hyder Chairman (NAPHDA): Unpacking The Low-Cost Housing Initiative

HBFC: Strategic Outlook towards Future!

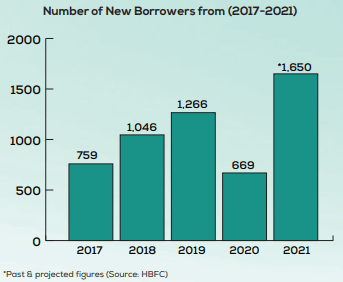

As Pakistan’s economy shows signs of recovery from the adverse effects of pandemic and government pushes ahead with its vison for low-cost housing, HBFC is strategizing to make its housing loan products more widely accessible. Its earlier emphasis on branch expansion, digitalization, work force efficiency and improved customer service had already made it possible to extend Rs. 2800 million in housing loans in 2019, however pandemic hit reduced its credit lending to around Rs. 1800 million in 2020. Now HBFC is poised to add 1600-1700 fresh loans by December 2021 crossing the total lending of Rs. 4000 million (PKR. 4 billion). This will be 100% more than 2020 and 40% more than its earlier record of Rs. 2.8 billion in 2019.

HBFC’s strategic thinking is being shaped by the changing market forces around it. Macroeconomic conditions such as interest rates, changing customer expectations, government initiatives, growing competition from commercial banks and rapid digitalization are some of the factors, institution has taken into consideration for formulating its own strategic agenda.

As digitalization continues to transform Pakistan’s financial sector, the institution has formulated strategies for becoming more customer-driven and efficient. The institution took several initiatives to achieve this objective including onboarding of Autosoft’s loan management system across HBFC’s network of 51 branches for better customer experience. This redesign & expansion strategy will enable the institution to continue its initiative of providing access to housing finance services to the growing population of the country with diverse needs.

With this strategic vision, HBFC is now poised to leverage the power of digitalization to produce new levels of workforce efficiency, productivity, customer experience and growth