The development of the housing ecosystem in any economy is a complex undertaking which requires fostering an enabling environment for both the supply of and demand for housing. A myriad of policies affects housing.

The provision of infrastructure, the regulation of land, the organization of the construction and materials industry, and the involvement of the public sector in the provision of housing, etc. All these factors have a direct bearing on the production of housing and its responsiveness to shifts in demand.

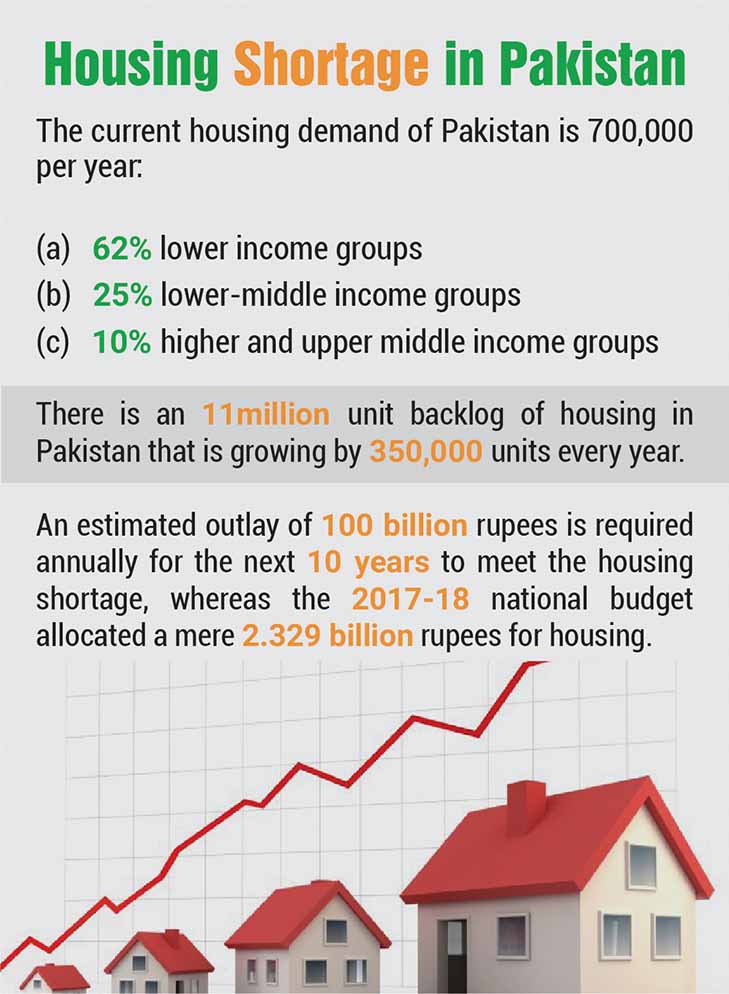

The housing gap in Pakistan is huge and growing dramatically. In 1998, the housing stock was 19.2 million, while the shortage was 4.3 million.

But other policies – which, for example, affect the security of tenure for housing and hence the ability to use it as an asset for securing long-term financing – directly impact the desirability of and demand for, real estate and housing as an asset.

In turn, all these policies affect the quantity of housing available to meet the needs of final consumers, housing sector prices and hence their affordability. These policies also heavily influence the costs, availability, quality and production of informal housing, which accommodates most of the population in developing economies.

Read more: An interesting plan to ‘sell Pakistan to the world’ – Chairman…

Governments should be encouraged to adopt policies that enable housing markets to work. Governments have at their disposal multiple enabling instruments, some that address demand-side constraints, some that address supply-side constraints, and one that improves the management of the housing sector as a whole.

The Demand-Side Instruments are

(i) developing property rights: ensuring that rights to own and freely exchange housing are established by law and enforced

(ii) Developing mortgage finance: creating healthy and competitive mortgage lending institutions, and fostering innovative arrangements for providing greater access to housing finance to the poor;

(iii) rationalizing subsidies: ensuring that subsidy programs are of an appropriate and affordable scale, well-targeted, measurable, and transparent, and avoid distorting housing markets.

The Supply-Side Instruments are

(i) providing infrastructure for residential land development: coordinating the agencies responsible for the provision of residential infrastructure (roads, drainage, water, sewerage, and electricity) to focus on servicing existing and undeveloped urban land for efficient residential development;

(ii) regulating land and housing development: balancing the costs and the benefits of regulations that influence urban land and housing markets, especially land use and building, and removing regulations which unnecessarily hinder housing supply;

(iii) organizing the building industry: creating greater competition in the building industry, removing constraints to the development and use of local building materials, and reducing trade barriers that apply to housing inputs.

These instruments are to be supported and guided by developing the institutional framework for managing the housing sector: strengthening institutions which can oversee and manage the performance of the sector as a whole; bringing together all the major public agencies, private sector, and representatives of non-governmental organizations (NGOs) and community-based organizations; and ensuring that policies and programs benefit the poor and elicit their participation.

Read more: Pakistan’s PM takes a new initiative: Homes for Homeless

Current Situation of the Housing Market in Pakistan

The housing gap in Pakistan is huge and growing dramatically. In 1998, the housing stock was 19.2 million, while the shortage was 4.3 million. According to the population census of 2017, the housing stock is now 32.2 million, of which 39 percent is urban. Over the next 20 years, the annual urban population increase is expected to be about 2.3 million per year (around 360,000 households at 6.35 individuals per household).

In turn, all these policies affect the quantity of housing available to meet the needs of final consumers, housing sector prices and hence their affordability.

A decline in family size and increased household formation rates (stemming from the large cohort of young people) are expected to further increase the demand for housing. The gap continues to increase by roughly 350,000 units per year, as new housing production falls short of the rate of household formation and existing housing units become obsolete.

The quantitative housing shortage is exacerbated by qualitative deficits such as overcrowding, low quality, and continuous deterioration. Around 47 percent of urban households live in substandard housing, often located in informal settlements called Katchi Abadis, which lack basic urban infrastructure and have poor health conditions. The existing housing stock is also extremely overcrowded.

Overall asset ownership, as well as homeownership, is highly skewed towards the male population, and estimates indicate that only 2 percent of women aged 15-49 own homes and only 2 percent own land. Joint ownership is higher but still, only 8 percent of homes are jointly-owned and 2 percent for land.

Read more: Competition Commissions of Pakistan catches housing scheme lies red handed

World Bank Support for Pakistan’s Housing Market

The World Bank Groups support for housing in Pakistan has been very broad-based and has been designed to tackle multiple inefficiencies in the housing market; this has ranged from land titling initiatives, to ease of doing business in construction, to the foreclosure law for housing, to low-income housing policy support etc.

The World Bank’s most recent engagement is the USD 145 million Housing Finance Project (IDA credit) with the Ministry of Finance and the Planning Commission of Pakistan. This project became effective in June 2018. The development objective of this project is to increase access to housing finance for households and support capital market development in Pakistan.

The Housing Finance Project has Three Components

(i) Supporting the Pakistan Mortgage Refinance Company (PMRC): PMRC is expected to foster access to both mortgage finance and capital markets. PMRC has been established as a development finance institution (DFI) with majority private sector ownership (51 percent private commercial banks) and 49 percent public sector banks and the GoP/Ministry of Finance. IFC, the World Bank’s sister institution is also a potential equity investor into PMRC (the terms of the investment are currently under negotiation).

PMRC is expected to address several market failures to improve mortgage affordability by: (i) supporting lending at a fixed rate, (ii) facilitating the standardization of origination and servicing standards of mortgages and enhancing their quality; and (iii) providing an efficient capital market long-term funding channel.

(ii) Supporting the expansion of mortgage loans: This component aims to provide incentives to commercial banks to increase access to mortgage loans to a larger segment of the population.

The mortgage product can be made more affordable and better secured by offering fixed rather than variable interest rates and by lengthening the tenor beyond 15 years. By helping banks offer loans as small as PKR 0.5 million, the project can help reach down-market to low-come households, and underserved market segments such as women.

(iii) Capacity building for housing policy and analytics: The objective of this component is to enhance analytical capacity and policy formulation for sound national housing policy and for addressing supply-side constraints that hamper the development of affordable housing stock in Pakistan. At present, there is a big knowledge gap in this space.

Main support will be provided for the establishment of an Urban and Housing Policy Unit under the Ministry of Planning, Development and Reform. Support will be directed toward increasing the institutional and technical capacity of the Urban Unit and other stakeholders such as the Prime Ministers Housing Task Force.

According to the population census of 2017, the housing stock is now 32.2 million, of which 39 percent is urban.

The primary beneficiaries of this project will be households in Pakistan. (A household, as defined by the Pakistan Bureau of Statistics, may be either a single-person or multi-person household). The national average household size is 6.35 members. A male head of household is typically the mortgage loan borrower.

The project will make a specific effort to cater to female-headed households by providing price incentives, in addition to encouraging co-borrowing and co-ownership by husband and wife. The project also aims to foster more environmentally sustainable housing constructions through financing incentives.

Read more: Pakistanis robbed of billions by Housing Societies: Where are authorities?

The Following Indicators will be Used to Measure the Achievement of Project Objectives

(i) Number of total mortgage loans refinanced by PMRC

(ii) Number of total outstanding mortgage borrowers

(iii) Percentage of outstanding women mortgage borrowers refinanced by PMRC

(iv) PMRC bond issuance volume

In addition to this active World Bank project, the World Bank Group is in dialogue with the PM’s Housing Task Force to help instil international best practices in the Naya Pakistan Housing Scheme.

The World Bank Group is planning a Pakistan Housing Conference in the first quarter of 2019 to bring in global experts (from the World Bank, IFC & other international practitioners) to share international best practices in land markets, developer finance, low-income housing, mortgage finance etc.

This forum will help showcase global best practices in supporting the housing sector; this can help to inform policy in Pakistan as the new government tackles this very important and challenging agenda. Everyone has a fundamental human right to housing, which ensures access to a safe, secure, habitable, and affordable home with freedom from forced eviction.

It is the government’s duty to try to ensure that everyone can exercise this right to live in security, peace, and dignity. The new government is to be congratulated for taking this agenda forward and making it such a prominent part of their reform agenda.

Namoos Zaheer is a Senior Financial Sector specialist with the World Bank’s Finance, Competitiveness & Innovation Global Practice. She is the task leader for the World Bank’s Housing Finance Project in Pakistan.

The views expressed in this article are author’s own and do not necessarily reflect the editorial policy of Global Village Space.