Pakistan is taking some desperate measures to prevent its economy from collapsing. Pakistan has listed the property at its embassy in Washington for sale due to the severity of the crisis. Every citizen now carries a frightening 21% greater debt burden than they had in June 2021 (Rs 179,100 vs. Rs 216,708).

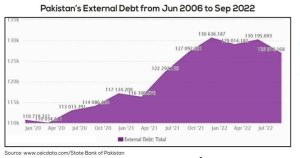

Pakistan’s public debt, which represents around 97 percent of its GDP as of January 2023, is estimated to be around PKR 62.46 trillion (USD 274 billion). In the first quarter of 2023, Pakistan must repay more than $8 billion in debt, while it now has only $3.4 billion in foreign exchange reserves. Hence, Pakistan may default on the repayment of its foreign loans or even go bankrupt.

Read more: Pakistan caught in a serious debt trap

Due to the continual borrowing of money to pay off previous debts, the state’s financial dilemma is deeply ingrained. A crisis has been brewing for quite some time as a result of the economy spiraling into a vicious cycle of debt and partial payments. The debt issue is growing, and as a result, the strain on the economy is increasingly affecting the general public at large.

In an effort to address the issue, the government has now turned to small-scale solutions like limiting imports and the early closure of malls, markets, and wedding halls. A significant portion of Pakistan’s economy depends on imports, and as the financial crisis worsens, the country has been subject to a number of import restrictions. Economists worry that ultimately there will be a lack of food and other essentials for the general population. To top it all off, foreign investors are attempting to liquidate their domestic holdings in Pakistan, which will worsen the unemployment crisis.

Over the past 75 years, Pakistan has seen numerous bouts of near-crisis situations where it has had to deal with the tremendous strain on its fiscal imbalances and balance of payments. The IMF has repeatedly given assistance to Pakistan to prevent the economic collapse of the country and to use conventional economic stabilization measures to restore short-term economic stability.

Pakistan tried every avenue to secure loans and financial assistance, turning to commercial banks in friendly countries, foreign lenders, and multilateral organizations. Resultantly, the country has turned into a rent-seeking economy, extracting rent in an inefficient way rather than repairing the sector structurally. Even though doing so requires Pakistan to take on additional debt and increase borrowing, the country’s financial elite nonetheless devotes the majority of its time to securing various subsidies.

Read more: Pakistan’s economy in ‘collapse’ as IMF visits

With so much debt, Pakistan has long struggled to attract investment and foster innovation. The effectiveness of macroeconomic policy for the entire economy is constrained by underdevelopment and vulnerabilities in certain regions. The neglect of the agriculture sector is also one of the major causes of the nation’s balance of payments crisis.

Pakistan has begun importing wheat and cotton in recent years, which has increased pressure on the nation’s import bill. The main policies that focused Pakistan’s attention on areas that were not beneficial for the economy are to blame for the chances squandered in agriculture. Pakistan must devise and implement long-term sustainable policies if it wants to escape the vicious cycle of borrowing money to repay debts.