A few years back, when Pakistan was under the umbrella of the International Monetary Fund (IMF) program from the year 2013 to September 2016, there appeared to be some stability. The current account deficit of the time was manageable and not much more than 1% of the GDP.

Overall the position was fairly stable, our reserves went up and almost hit their peak at US$19 billion. There was a general degree of complacency that the economic situation is stable.

The possible negotiation would have facilitated the coming government to immediately take a step forward because every day counts now.

The rupee value remained almost unchanged, more or less of the same value. But given the difference in the rate of inflation and so on, our currency was becoming overvalued. And at its peak, its overvaluation had exceeded about 24%.

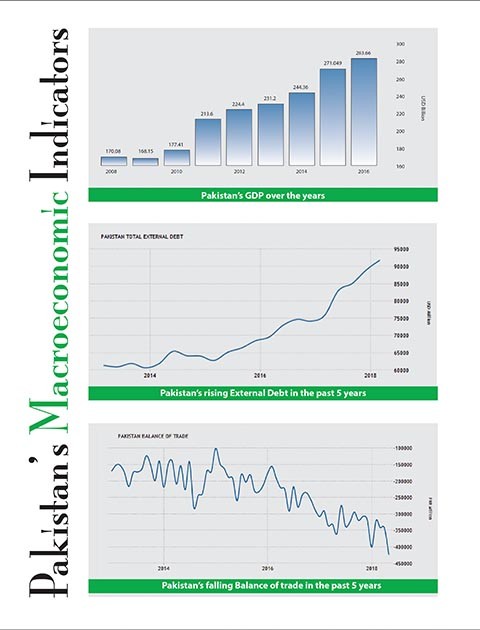

Once the process of unwinding started by the end of 2016, the current account deficit started widening and by the end of the period of 2016-17, it reached almost US$12 billion, which was well in excess of the previous year which was less than US$5 billion. Resultantly, we started borrowing massive amounts from commercial banks, particularly Chinese banks and floating bonds.

Hence, the bottom line is that the economic condition had changed fundamentally and in a sense, this change in response was inevitable. The second finance team under Miftah Ismail responded to the issues. One of the things left unnoticed during this period of apparent stability from the financial years FY 2014 to FY 2016, was the fact that exports were plummeting.

Read more: Pakistan Economy’s Progress Card

Meanwhile, the underlying pressure on imports was not observed because oil prices remained low until late 2015. They started rising afterwards and increased sharply in the last 6-8 months. This resulted in our imports going up by 16-17% and this year they have reached up to 18%.

Our exports are equivalent to hardly 45% of the imports; they must increase by twice as much in terms of growth. The end result is that your current account deficit has widened to a US$16 billion and by the end of the year, it will probably approach US$18 billion. In a nutshell, Pakistan is now in an extremely unstable and a very unmaintainable position.

Borrowing is being affected now because the multilateral will not lend us money unless we have a cover for at least two months of imports. The money in the coffers has now begun to dry up. Fortunately, Pakistan has China as a resource, which continues to extend money to Pakistan for infrastructural purposes under CPEC.

Moreover, Chinese commercial banks have lent as much as 60% of the borrowing this year, however, the bottom line still remains that all of this is unsustainable. In the short run, Pakistan has limits to how far it can increase its exports because of the limited base.

Some of the items should be exempted, such as some of the petroleum imports, the fertilizer imports, and medicines.

The way out has to be, unfortunately, a fairly significant contraction in imports. Now this year, Pakistan will close with the figure of about US$57 billion and exports with significant growth may hit US$25 billion. So, the trade deficit will calculate to be US$32 billion, which is completely unsustainable.

Now, what are the options available for Pakistan? What is the strategy to follow? With all due respect to Miftah, they moved in with small incremental moves, which openly fueled speculation. People and importers are now obligated to think of this incremental strategy, where the exchange rate will be allowed to decline three times.

So, despite the devaluation, imports have increased by 20% last month. This clear growth in imports is worrisome in the wake of devaluation and clearly reflects the element of speculation. This is a self-full filling prophecy. The stock market in the last few days has fallen by 2000 points or so because money is being taken out of Pakistan by mutual funds and investors.

About US$8-10 million is taken out of Pakistan daily. Secondly, multinationals have started repatriating their profits out of the country, because they want their reserve value intact in dollar terms. The third is the speculation which is already dealt with above.

Read more: Pakistan’s Economy may become worse under FATF’s grey list

Now we need to focus on the possibility that exporters may retain their proceeds abroad in the hope to secure a gain of 4-5% in the next few months and to maintain their reserve value intact in dollar terms. The story is of one incipient financial crisis. In fact, calling it incipient is a generosity – we are in a financial crisis.

Unfortunately, we have an interim government which is unwilling to take decisions, partly because of limitations to its constitutional mandate. However, this emergency situation calls for some decisions. Now, the kinds of decisions we can take are as follows. Firstly, our export relief package should be much stronger.

Basically, the condition should be ‘spend rupee in order to get dollars’. So, what we need to do is, raise our rates of duty drawback or export rebates. Bangladesh gives about 15% on some goods; we should do the same on some of our value-added goods, emerging goods and also emerging markets. These should be paid out of the banking system.

FBR should not be allowed any involvement, because they are the worst in terms of restricting the flow of the economy. Like in Bangladesh, export receipts should come quietly. This will increase the incentives to send the export rebate receipts back to Pakistan.

Our exports are equivalent to hardly 45% of the imports; they must increase by twice as much in terms of growth.

You automatically get the duty drawback through the commercial banking system and it gets reimbursed from SBP. This is the way of spending rupees to get dollars, something which Pakistan clearly needs to do. Secondly, we should remove the perch of energy inputs included in the electricity taxes, to make the industry competitive.

Thirdly, revenue should be used to raise it through enhancement of duties on imports. If the caretaker government is worried about raising the taxes, it should ask the SBP to introduce cash margins across the board to prevent speculation. It should introduce 30% of the cash margins on all imports.

Currently, they have a margin of 8% on non-essential items. I did it when we had to manage the economy after the sanctions. Some of the items should be exempted, such as some of the petroleum imports, the fertilizer imports, and medicines.

Read more: Pakistan economy set to record fastest growth in 13 years

Cash margin requirement prevents speculation. If you [commercial importer] want to speculate, use 30% of your own money. These big moves need to be taken now, we don’t have time. With all due respect to the caretaker government, it is only hiding behind the constitutional limitations. When I was part of the interim government on two occasions in 1996 and 2000, I actively negotiated on IMF loans.

Though, the amount back in those days used to be much less than the current amount at hand. Since Pakistan is in a very difficult situation, the interim government could have at least invited the IMF for normal article four consultations. That would have set the process going.

Now, without any exchange of negotiation, they would have arrived at some understanding of the reform package which is immediately required. The possible negotiation would have facilitated the coming government to immediately take a step forward because every day counts now. The rupee is depreciating, money is going out of the country, the stock market is plunging and we are in crisis – whether you like it or not.

Dr. Hafeez Pasha is a distinguished Pakistani economist. who is the Chairman of the city’s Panel of Economists, an independent advisory committee for the government. He is the Dean of the School of Social Sciences at the Beaconhouse National University, Lahore and also the Vice Chairman of the university’s think-tank, the Institute of Public Policy. Pasha has also served as Minister of Finance, Education, and Commerce in three different governments.