Both the developed and developing countries saw an active period of privatization – called the ‘golden age of privatization’ – during the end of the 1980s to the middle of 2000s. It happened at the back of the rising Neoliberal wave, which inherently saw the little role of governments in the economy or regulation of markets. During this era of privatization, such activities were mostly pursued by offering shares as the primary method of sale, and predominantly to the domestic base of retail-investment, which formed the primary source of proceeds.

Even at the peak of the privatization drive, research indicated a mixed result whereby privatization succeeded in countries where economic institutions were already strong, among other things. Stability meant an environment where ruleof-law was strongly functional, competition and enforcement were robust, and the budget was kept under hard constraints with the sound practice of regulation and overall governance.

In the absence or lack of the pre-requisites mentioned above, if the wave of Neoliberalism-led privatization happened in an environment of weak checks and balances, especially, on the deregulated or privatized financial sector, commercial and investment banks, and other financial institutions, It further perpetuated the unstable environment, ultimately leading to the Global Financial Crisis (GFC) of 2007/08.

The presence of SOEs in the global economy has grown strongly in recent years. Today they account for over a fifth of the world’s largest enterprises as opposed to 10 years ago where only one or two SOEs could be found at the top of the league table.

This in turn also increased income inequality and poverty levels, even in developed countries. On the contrary, countries where such drastic moves to Neoliberalism were not adopted – including China and Scandinavian countries among others – the gradual move to opening up of the state-owned enterprises (SOEs) sector paid dividends, both in terms of muted impact of the 2007/08 crisis in these countries, and also on income inequality and poverty levels.

Post GFC 2007/08 marks the second period of privatization, where learning meant that this time state retained significant hold over SOEs. By listing large SOEs on stock exchanges or selling shares to strategic investors, the state in both cases remained a majority holder of shares or retained minority shares of significant nature that kept it in the driving seat in terms of overall decisions about a specific SOE.

According to an OECD’s (Organization for Economic Co-operation and Development) policy guide on privatization (2018), ‘These partially state-owned enterprises benefited from performance and efficiency improvements through the discipline of stock market listing or private ownership. On the other hand, mixed ownership allowed the state to maintain strategic participation in companies for which there remained a rationale for continued state ownership.’

Read more: MPCL holds forum on sustainable energy, future privatization

Sucess of Privatization

The advice given based on the experience of the last three decades or so should become the basis for a developing country like Pakistan, which is looking to improve the affairs of its around 170 SOEs (or Public-Sector Companies). For many years, many of these SOEs have been entailing losses, which have fed heavily into keeping the fiscal deficit on the higher side as a percentage of GDP (gross domestic product), mainly through the build-up of contingent liabilities.

At the same time, outright privatization is likely not to succeed in Pakistan, given the pre-requisites essential to its success are not much there. Moreover, there are already issues of transparency, fair distribution of profits, and quality of service from the privatization drive during the first phase or the golden age of privatization, especially concerning entities privatized in the energy and banking/financial sectors.

Moreover, the enthusiasm for privatization highlighted by the EFF (Extended Fund Facility) negotiated program document, ‘Jumpstarting the privatization process’ – as part of the overall structural policies being pursued in the program with the IMF – should be reined-in to internalize the thought-process indicated earlier. The program document also suggests the government’s intentions to create a holding company – details of which have not been given there – to increase the level of efficiency and independence of SOEs.

Read more: Is PIA’s restructuring a gimmick used to kick-start privatization?

Therefore, as the government initiates the muchneeded reform effort and possible privatization drive for at least some of the SOEs, consequently it necessitates highlighting some necessary thought-process that could strengthen the whole working about this effort. The roads to privatization and lessons learned have already been indicated in the paragraphs above, so it makes sense to bring a greater understanding of SOEs and reforming them.

The importance of well-functioning SOEs could be gauged from a flagship OECD publication (2018) titled ‘Ownership and Governance of State-Owned Enterprises: A Compendium of National Practices’. It has highlighted that the ‘state-owned enterprises (SOEs) are an essential element of most economies, including many more advanced economies.

SOEs are most prevalent in strategic sectors such as energy, minerals, infrastructure, other utilities and, in some countries, financial services. The presence of SOEs in the global economy has grown strongly in recent years. Today they account for over a fifth of the world’s largest enterprises as opposed to 10 years ago where only one or two SOEs could be found at the top of the league table.

It means that high standards of corporate governance of SOEs are critical to ensure financial stability and sustain economic growth. Well-managed SOEs have been the primary vehicle of fast-paced performance of countries like China, Singapore, and Indonesia, among others. Also, the above indicates the importance of significant hold of the state over SOEs, especially in the strategic sectors.

Chinese experience of Mixed ownership Enterprises

At a time, when the world, in general, was being swept by the Neoliberal wave, China held on to its SOEs and reaped enormous benefits of high-paced development with equitable distribution of the fruits of overall economic growth. Even when they have opened it to the private sector, they have done by remaining mindful of the strategic value of a particular SOE, and that too in a gradual manner to make the right calls.

China allowed greater participation of the private sector by adopting a Mixed-Ownership Enterprises (MOEs) framework after the other elements of strong economic institutions and higher capacity of the state to regulate the private sector were established on firm grounds. So, what is an SOE? OECD defines SOE as ‘any corporate entity recognized by national law as an enterprise in which the state exercises ownership’.

It includes joint-stock companies, limited liability companies, and partnerships limited by shares. Moreover, statutory corporations, with their legal personality established through special legislation, should be considered as SOEs if their purpose and activities, or parts of their businesses, are primarily economic.’ Similarly, in Pakistan, the Public-Sector Companies (Corporate Governance) Rules, 2013, as amended up to April 21, 2017, identify Public Sector Companies (PSCs or SOEs) and their functions.

It states that PSC or SOEs means ‘a company, whether public or private, which is directly or indirectly controlled, beneficially owned or not less than fifty one percent of the voting securities or voting power of which are held by the Government or any instrumentality or agency of the Government or a statutory body, or in respect of which the Government or any instrumentality or agency of the Government or a statutory body, has otherwise power to elect, nominate or appoint majority of its directors, and includes a public sector association not for profit, licensed under section 42 of the Ordinance.’

In a report titled ‘State-Owned Enterprises in Asia: National practices for performance evaluation and management’ (2016), the OECD highlighted that the PSCs are joint-stock companies of the nature of limited liability in Pakistan, with state holding a significant position in it. The organization compiled the report after it received responses to a questionnaire from the relevant authorities of a select group of countries.

It is not to say that the private sector is not in somewhat good shape overall, but to understand significant shortcomings about its capacity and the need for improving the economic environment, including initiating substantial reforms for the private sector by the government.

As reforms for SOEs are underway and the enabling environment – improved economic institutions – is approached, it, therefore, could make sense to exploit this avenue further to allow greater participation of private sector, including adopting MOE framework. It would also mean the need for more significant reform of stock-exchanges and overall reducing market failures in the country, especially, those that do not allow a muchneeded reduction in information asymmetry and transaction costs.

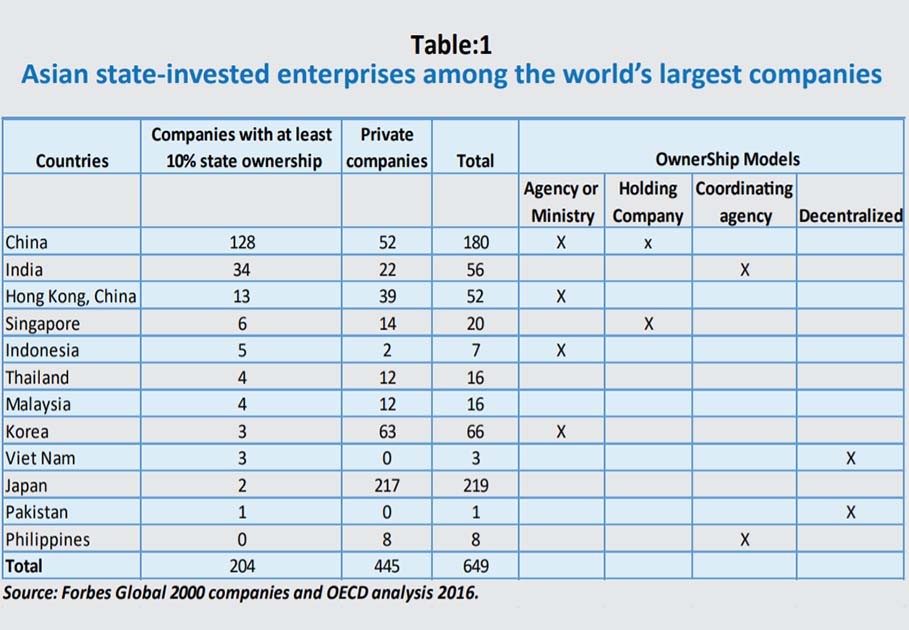

The same report highlights (see Table 1) that ‘among the world’s 2000 largest companies, 644 are located in Asia, of which about one third have at least 10% state ownership’. Currently, Pakistan follows the ‘decentralized’ SOE ownership model, whereby only the respective ‘line ministries’ are responsible for exercising ownership of SOEs, and include among others, Ministry of Petroleum and Natural Resources, Ministry of Finance, Ministry of Water and Power, Ministry of Railways, and Ministry of Ports and Shipping.

Read more: Privatization of PIA and PSM: significance for Pakistan

Although Pakistan intends to create a holding company to improve the efficiency of SOEs, the table shows that China, Indonesia, and Korea – all performing a lot better than Pakistan in terms of SOEs performance – have adopted a very centralized model. Hence, Pakistan should look into the practices of these countries in this regard. In Pakistan, the table also shows, the private sector/companies have also not performed as well as they should have.

Not a single company made it to the list of top 2,000 largest companies globally as against 8 in Philippines and 12 in Malaysia, which among other reasons regarding the availability of finance to the private sector, could be the result of negative fallout of the lack of presence of pre-requisites – strong economic institutions and all. Hence, the capacity of the domestic private sector is also not that convincing as may be trumpeted otherwise when euphoria is whipped-up in media and scholarship; it may be grounded more in idealism than ground realities.

It is not to say that the private sector is not in somewhat good shape overall, but to understand significant shortcomings about its capacity and the need for improving the economic environment, including initiating substantial reforms for the private sector by the government.

In China for example, under the direct leadership of the ‘State Council’ – headed by the Prime Minister – a single agency called the State-Owned Assets Supervision and Administration Commission (SASAC) is mainly responsible for regulating/ supporting around 110 non-financial central SOEs, spread over a diverse range of sectors, including among others, machinery, metallurgical, petroleum & petrochemical, electronics, electricity, construction, communications & transportation, and telecommunications. Pakistan may also want to research further on the lines of establishing such an agency, placed directly under the PM, for reforming and regulating SOEs; preparing among those, where need be, for possible privatization.

Even in terms of the extent of oversight, India – which has 34 SOEs in top 2,000 largest companies globally, against only one in Pakistan in 2016 – has a coordinating agency model. In contrast, Pakistan has only respective line ministries exercising ownership. In India, the responsibility for this is with Department of Public Enterprises (under the Ministry of Heavy Industries and Public Enterprises) along with other institutions, including the parliament, the government via the relevant ministry, the planning commission, and the comptroller and auditor general, among others.

Read more: PTI decides to prepare new privatization policy

Pakistan could approach China to negotiate technical assistance in developing an agency on the lines of SASAC. Similarly, it should also seek technical support from the extensive work of the ‘OECD Working Party on State Ownership and Privatization Practices’ which ‘facilitates policy dialogue and information exchange between OECD-member countries and key partners on improving corporate governance of stateowned enterprises and implementing privatization policies’.

In case, Pakistan wishes to pursue the path of formulating a holding company as the ownership model, then, among other places, it could learn from the ‘Temasek Holdings’ in Singapore, which works under the purview of the Ministry of Finance. Moreover, Kazakhstan and Bhutan also have holding companies – ‘Samruk-Kazyna’ and ‘Druk Holding and Investment Limited’, respectively – from which lessons could be learned.

Other specific issues with SOEs in Pakistan have aptly been highlighted by OECD, in its (2018) report titled, ‘Managing risk in the state-owned enterprise sector in Asia’, whereby a) there is no explicit requirement for SOEs to ‘establish an internal risk management function or to employ risk officers or other staff specialized in risk management’, b) there exists lack of any specific maximum leverage ratio, c) no linkage exists between risk-taking and SOE executive remuneration policy, and d) while ‘the Auditor General of Pakistan is responsible for undertaking performance audits of most SOEs, but does not appear to have an explicit responsibility for reviewing SOEs’ risk management practices’. Another crucial area of concern is a weak risk management performance.

These and other issues – especially about bringing the technically expert and independent board of directors of SOEs, and strengthening mechanisms for holding sound internal and external audits of SOEs – should carefully be focused upon by the Committee tasked with reforming SOEs in Pakistan.

Dr. Omer Javed is an institutional political economist, who previously worked at International Monetary Fund, and holds PhD in Economics from the University of Barcelona. He tweets @omerjaved7.

The views expressed in this article are author’s own and do not necessarily reflect the editorial policy of Global Village Space.