When Imran Khan assumed office on August 18, 2018, as Prime Minister, he was aware that the country faced an economic crisis that would be greater than any challenge he had undertaken in his career. However, the enormity of specter that haunted Pakistan became fully apparent in the following weeks, as the PTI government faced the possibility of economic implosion, as a result of unsustainable current account imbalances, fast disappearing foreign exchange reserves, and potential default situation on external debt obligations.

Epic incompetence by the previous PML-N government had ensured that the country was engulfed in a severe economic crunch. The coterie of the incompetent had left behind a financial time bomb, such that the people of Pakistan would have to bear the burden of significant rupee depreciation, steep energy price hikes, rising inflationary pressures, high-interest rates, and low economic growth.

The PTI government had no option, but institute some of the reforms, such as a sharp depreciation of the currency and energy price hikes.

In its May 12, 2019, Press Briefing, the IMF acknowledged that the current economic crises were largely a “legacy of uneven and pro-cyclical economic policies in recent years aiming to boost growth but at the expense of rising vulnerabilities and lingering structural and institutional weaknesses.”

The PML-N government’s penchant for borrowing, to spend on grand infrastructure projects such as metro buses and expensive power generation units, might have helped temporarily boost GDP growth for the short-term, but did little to structurally enhance productivity by directing investment towards much needed human capital development and export-oriented industries that would ensure sustainable economic growth.

Read more: Failure in the conservation of water will make Pakistan a failed state

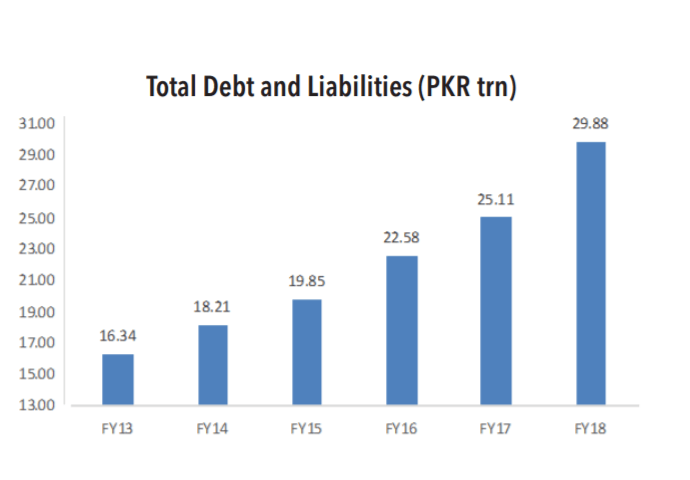

The zeitgeist to borrow, spend and let the devil take the hindmost, led to total public debt and liabilities increasing from Rs16.3tr in June 2013 to Rs28.9tr in June 2018, which breached the mandatory limit of 60% set under the fiscal responsibility and debt limitation act. The Spending Sultans took total public debt and liability to over 86.8% of GDP by June 2018.

Having already dispensed with the fig leaf of fiscal prudence, PML-N Finance Minister Ishaq Dar made the maintenance of Pakistan Rupee parity at 104 against US dollar a primary indicator of economic strength.

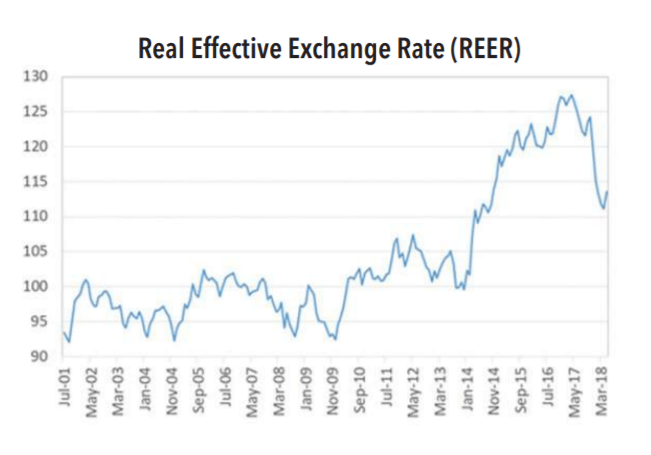

This absurd almost Freudian obsession with vitality meant that the Real Effective Exchange Rate (REER) rose from a near fair value of approximately 104.37 in July 2013 (as published by SBP) to a massively overvalued 127 by April 2017. Such gross overvaluation not only stimulated demand for imports but also ensured the decimation of Pakistan’s export competitiveness.

IMF reveals the responsible for Pakistan's dismal economic and structural state, and its not Pakistan Tehreek e Insaaf (PTI)#Pakistan #PTI #PMLN #NawazSharif #IMF #taxes #Economy #Government #PMKhan #ImranKhan #MaryamNawaz #ThirdWorld #Hope #Newsnight https://t.co/0EwYK0Nzlc

— GVS (@GVS_News) July 15, 2019

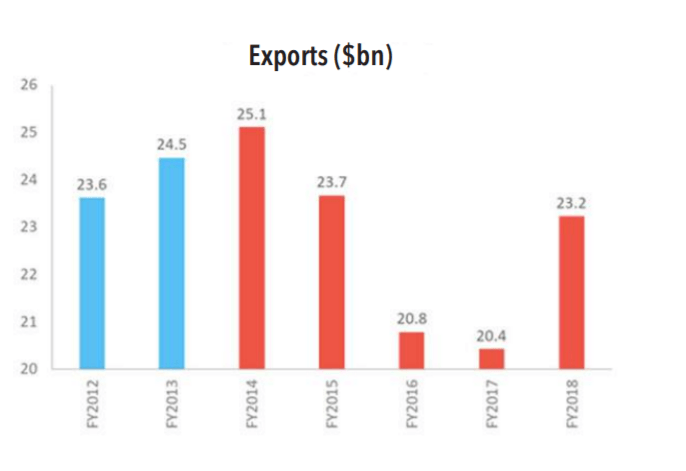

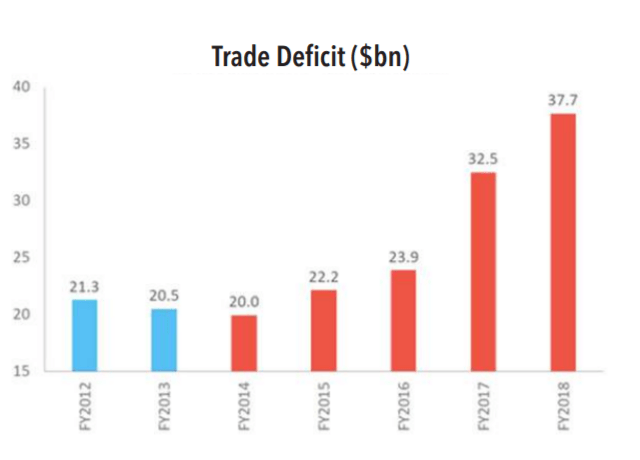

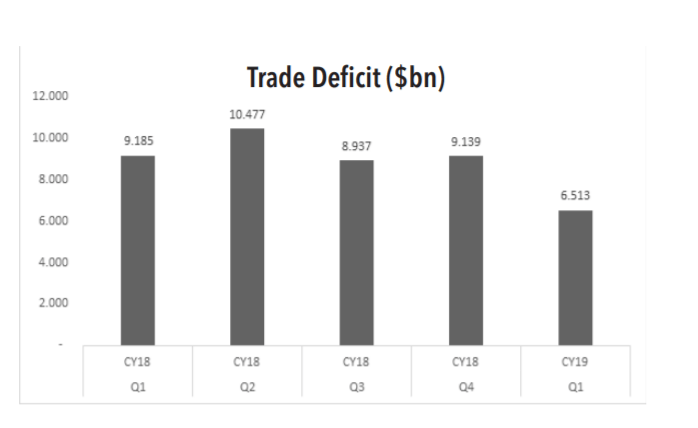

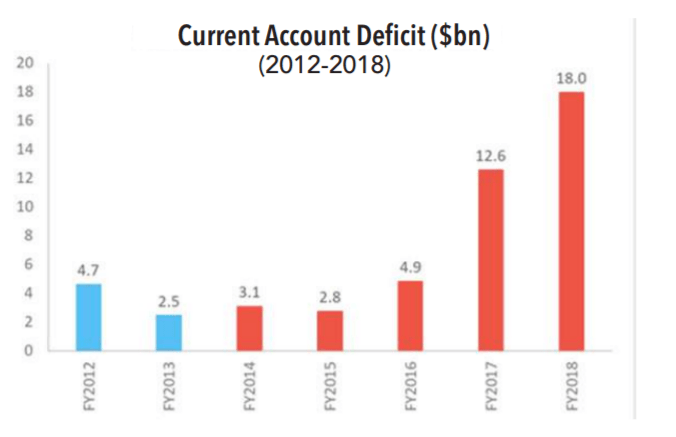

Consequently, the country’s imports ballooned from $44.8 billion in 2013 to $61 billion in 2018, while exports fell from $25 billion in 2014 to $20 billion in 2017, only to recover in 2018 to $23.8 billion. The external current account deficit, which stood at $2.5 billion in 2013, the last year of PPP government in office, exploded to $18 billion in FY2018 (5.8% of GDP) – over seven times greater than under PPP and the highest ever in absolute terms in the history of the country.

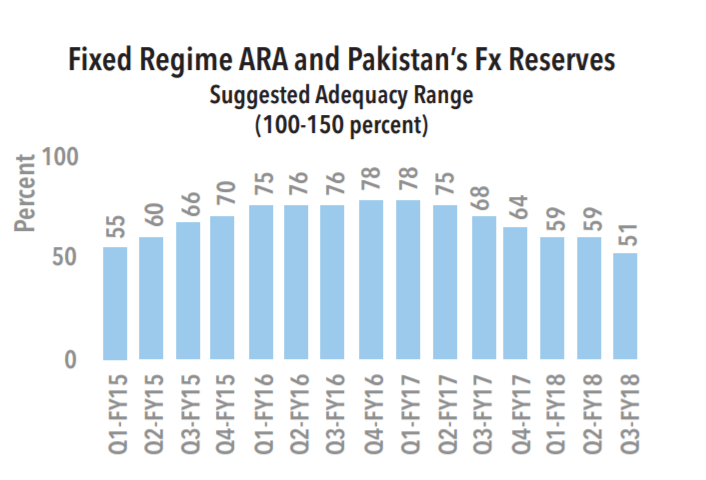

Record trade deficits resulted in a surging external current account deficit and rapid depletion of SBP’s FX reserves to around $9.8 billion or equivalent to less than two months of country’s imports. The ARA (Assessing Reserve Adequacy) metric, as published by SBP, dropped from 78.0 percent in end-June 2016 to only 51.0 percent in end-March 2018, clearly indicating that the foreign exchange reserves were wholly inadequate to meet short term debt obligations and three months import cover.

The coterie of the incompetent had left behind a financial time bomb, such that the people of Pakistan would have to bear the burden of significant rupee depreciation.

This decline in reserves took place despite the PML-N government’s attempt to bolster them by borrowing heavily internationally. Therefore, external debt increased from $61 billion in 2013 to $95 billion in June 2018. The strategy appears to have been to maintain an overvalued Rupee by borrowing externally. There seemed to be little policy concern about the impact of overvalued domestic currency on the competitiveness of the export sector.

While knowing perfectly well that they were taking the country into a debt trap, little was done to mitigate associated risks. PML-N’s policy decisions post-2015 not only set the path towards burgeoning current account deficits, a hollowing out of the domestic industrial base, but more egregiously, there was ever-increasing dependence on international lenders credit lines to sustain economic activity.

Read more: PML-N’s misaligned economic policies put Pakistan in trouble: IMF

PTI came to power just when PML-N’s consumption/import-led economic growth had exhausted itself and was coming to its logical outcome. The depletion of the foreign exchange reserves reached a point where there were inadequate funds to meet debt obligations or to cover imports for the next three months.

Given the massive external borrowing, there was only a limited capacity to do so further. Thus, the new PTI government faced a situation of a current account deficit running at more than $1.5bn per month, and as much as $7.5bn payments of debt and interest due over the next nine months.

PM Khan stepped up to the plate and against his nature, embarked on a whirlwind round of trips to friendly nations, to whom he humbly sought help, to navigate the country out of the dangerous swirls of imminent crises.

International debt markets and multilateral lending agencies were circumspect about providing further funding, given Pakistan’s track record of repeatedly failing to follow through on implementing structural changes as envisaged in IMF structural adjustment programs. That might have been one reason why it was made clear to the new government when it approached the Fund in autumn 2018, that this time around the lender of last resort would expect many of the tough restructuring measures to be taken upfront.

A situation, which was in sharp contrast to the conditionality, offered the PML-N government when it had gone to the Fund in 2013. Much of the reform measures with the PML-N were phased in throughout the facility. By contrast, the PTI government had no option, but institute some of the reforms, such as a sharp depreciation of the currency and energy price hikes – which were anyway an imperative – ahead of the IMF facility being made available.

Read more: Pakistan economy set to record fastest growth in 13 years

Given the state of the economy inherited by Imran Khan and his PTI team, they could have drawn the combined wisdom of some best global economists to guide their economic policies, but the economy would not have fared much better than it has over the last ten months. The Rupee had to depreciate sharply for REER to come closer to 100 or near fair value and energy prices had to be hiked to control a runaway circular debt.

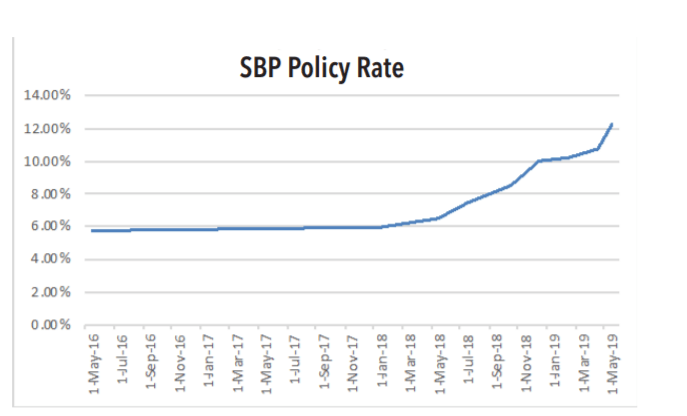

The rapid depreciation of PKR, by almost 30 percent, inevitably created inflationary pressures – core inflation jumped from below 6 percent in July 2018 to 9.55 percent and is expected to exceed 10 percent in the full year 2019. To contain inflation SBP has adopted a policy to maintain real interest rates around 3-4 percent, to contain inflationary expectations.

The depletion of the foreign exchange reserves reached a point where there were inadequate funds to meet debt obligations or to cover imports for the next three months.

There has been much criticism of the PTI government for not having concluded the IMF Extended Fund Facility earlier, in the first few months of the government assuming office. Critics argue that by doing so would have eliminated business uncertainty and restored market confidence, which in turn might have lessened the PKR depreciation and the stock market slide.

Such statements are entirely conjectural, and it is difficult to see how just a few months earlier agreement on fundamental long-term structural changes would have resulted in any significant difference to the trajectory of the economy.

Tax reforms, brought by PTI’s government, is a step towards Naya Pakistan #BePakistaniPayTaxes pic.twitter.com/xW56bnYiA0

— PTI (@PTIofficial) July 15, 2019

On the contrary, the recent revelation by the ex-Finance Minister of PTI Asad Umar suggests that the terms put forward by IMF when first approached were much more stringent than what was finally agreed in EFF in May this year. Umar has hinted that the Fund had initially demanded a free float exchange rate policy, SBP policy rates to be set at as high a level as 18 percent, and electricity tariffs to be hiked by 90 percent.

Arguably if these set of demands had been accepted the country would not only see a greater PKR depreciation, much higher inflation levels than it stands currently, and borrowing rates for business at around 18-20 percent would have not merely slowed down the economy, but potentially resulted in recessionary contraction.

Critics argue that by doing so would have eliminated business uncertainty and restored market confidence, which in turn might have lessened the PKR depreciation and the stock market slide.

Given the perilous state of forex reserves, and monthly bleeding of almost $2bn, as well as $7.5bn loan and interest payments due over next 9-months, Pakistan might have had to accept IMF’s initial cripplingly stringent terms unless it could garner loans from friendly countries. To do so, PTI’s PM Khan stepped up to the plate and against his nature, embarked on a whirlwind round of trips to friendly nations, to whom he humbly sought help, to navigate the country out of the dangerous swirls of imminent crises.

Read more: Imran Khan: Pakistan will soon emerge as the leading economy in the region

Here was a leader who was willing to swallow his own considerable pride to save the nation. If it meant an admission of the truth that the country was desperate for a cash injection to secure us some breathing space, PM Imran Khan was willing to admit that to his friendly host nations, who responded to such sincerity with a cash injection. Through his efforts, he managed to secure the country as much $9bn lifeline in the short-term loans and delayed oil payment facilities.

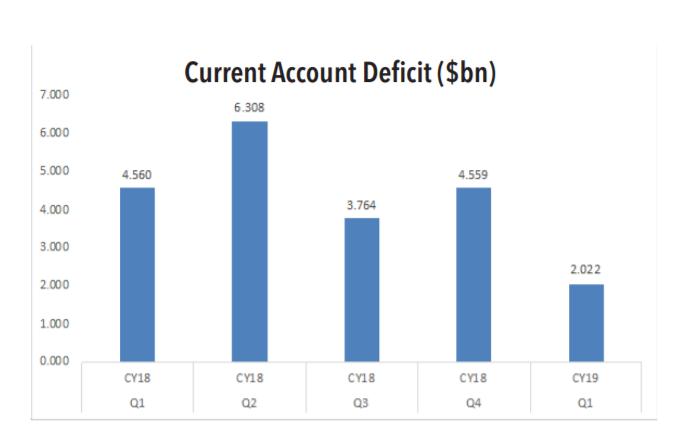

At the same time, PTI’s ex-Finance Minister Umar took necessary corrective measures such as a sharp depreciation of the currency and tariff hikes on non-essential imports to contain the trade deficit. The average monthly current account deficit has contracted sharply from greater than $1.5bn per month in 2018 to less than $0.75bn per month in the first quarter of 2019, which indicates that the strict policy measures are starting to work, in terms of containing imports at least.

Umar has hinted that the Fund had initially demanded a free float exchange rate policy, SBP policy rates to be set at as high a level as 18 percent, and electricity tariffs to be hiked by 90 percent.

It is expected the full impact of depreciation in terms of export expansion will happen with a lag of 9-12 months. There are no magic bullets in economics and indeed no miracles, but recovery is only possible through toil and tears. Accepting IMF terms earlier would have made little difference to the tough reforms that the country has to endure for its long-term good. After the wild party of consumption-driven economic growth fueled by binge borrowing by the previous government, a period of sobriety to put the house in order was almost inevitable.

It is the people who are paying the price for earlier rulers caring little to invest in their populace or building a robust export base. Few stock market analysts, who rejoiced at every uptick of the index as it rose to new peaks during the spending spree of PML-N, rarely warned punters of the sea of troubles that was about to come crashing on the economy. Few are willing to hear the simple truth that borrowed prosperity almost always ends in tears, and almost none celebrate the significant structural change of the economy that entails considerable hardships.

Read more: ‘Naya Pakistan is a Pakistan of a common man’: CM Buzdar

It was never going to be an easy journey to a Naya Pakistan after decades of sustained decay in almost every sphere of public policy. The necessary reforms might mean that conditions get worse in the short term. However, there is little choice but to act. Hopefully, the government is successful in its efforts to minimize the burden on those least able to bear it. PTI’s Finance Minister Hafeez Sheikh and his team must do more to explain to a shell-shocked nation of the causes behind the dramatic reversal of economic fortunes in the country.

The heavy burden of previous governments’ follies has to be carried on the shoulders of the people of Pakistan. They will yet again have to demonstrate their infinite resourcefulness to meet tough challenges ahead. The nation requires competent and transparent governance. The government, in turn, has to have the people’s support in carrying through the many stringent reform measures necessary. Only that will steer the nation to renewed and sustainable growth such that it never has to go to IMF again.

Javed Hassan is presently Chairman NAVTTC. He is a graduate of Imperial College London and an MBA from London Business School. He tweets: @javedhassan. The views expressed in this article are author’s own and do not necessarily reflect the editorial policy of Global Village Space.