Western countries, especially the UK, USA, and Canada, and many European countries, have very high homeownership rates, often 85 percent and above. In fact, in the 1980s, British PM Margaret Thatcher propounded the British dream of a property-owning democracy as a way of reducing the disparity of people’s social and political rights and their lack of economic assets.

In Pakistan, successive governments have tried to introduce low-cost schemes, often through government provision, but the involvement of the private sector was limited majorly due to the lack of mortgage financing available.

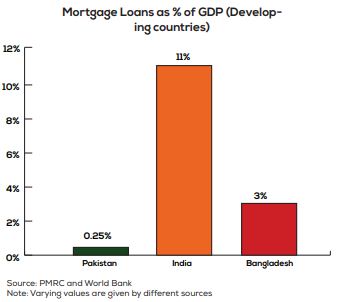

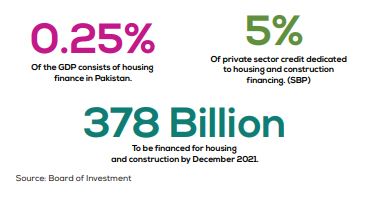

The easy access to mortgage financing drives people’s ability to buy houses; currently, in the United States, almost 80 percent of people construct homes through loans. It stands at 33 percent in Malaysia, 11 percent in India, and 3 percent in Bangladesh. By comparison, Pakistan has mortgage financing at 0.3 percent of GDP, which is way lower than its regional peers.

Read More: Importance of Mortgage Lending in housing market: Explains Fahad Siddiqui JS Bank

Banks have faced criticism for taking the easy route out and investing in government debt rather than, for example, helping people fund their own homes. Banks have protested in the past that the government has not done the necessary groundwork for enabling a thriving mortgage market.

Some of the major barriers, banks highlighted, include the country having weak and non-transparent titles on which banks were expected to give collateral, people’s income often not backed by documentation, courts issuing stay orders to people who were not making repayments to mortgage loans given, and since Pakistan does not have a strong capital market, there is generally a mismatch between tenure of assets and liabilities, which a bank faces when it gives long term loans out.

An attempt to address this last issue was made by the government through the PMRC which will be discussed in the following article. Well, things have finally changed, and one of the biggest drivers of this is that the government did substantial work with the State Bank of Pakistan and the courts on the foreclosure law, which now provides comfort to the banks that their loans are safe.

The Financial Institutions (Recovery of Finances) Amendment Act was signed into law in August 2016. However, it was taken to court to contest banks’ rights to take back property from owners who had reneged on their payments.

Last year, March 2020, a five-member bench of the Lahore High Court issued a 103- page judgment (Writ Petition 33872- Mohammad Shoaib Arshad & others vs. Federation of Pakistan) that decided that the 2016 law allows banks to auction the mortgaged property of loan defaulters without obtaining a court order first – is constitutional.

Alongside this historical court decision for the mortgage market, there was in the background, hectic work between government, SBP, and Banks on explaining the importance and workings of foreclosure law.

They also made further revisions, which the National Assembly approved ‘an ordinance to provide for the efficient recovery of mortgage-backed securities by financial institutions’ (Ordinance No. IX of 2019). Given one of the significant hurdles perceived by banks had been their inability to pursue non-judicial foreclosures.

Under section 3 of this Ordinance allows banks to recover their mortgage principal or interest without needing recourse to a court or tribunal for intermediary facilitation. The section states any legal right (including those created through the mortgage) relating to a property created in favor of a ‘secured creditor’ (financial institution) can be enforced ‘without the intervention of any court or tribunal.’

This could be done 60 days after the banks issue a notice requiring the defaulter to pay their secured debt or installments. The law also enables the banks to approach the state to ask for help to take possession of properties to recover their dues. The state authority will need to take the necessary measures to ensure compliance with such a request.

Most importantly, it also declares that no actions undertaken by the state authorities in compliance with this law can be questioned ‘in any court of law or before any authority.’ Section 14 states that civil courts will have no jurisdiction over any matters pursued under this Ordinance. Section 15 states that the Ordinance overrides any other law inconsistent with its legal provisions.

Read More: Why the Naya Pakistan Housing Scheme is a game changer

Legal action cannot start against a creditor for its activities taken in good faith under the Ordinance. Under the new law, borrowers may challenge the action relating to the sale or possession of their property by the bank only if they submit 75 percent of the payable amount to the court.

A small caveat is that this requirement only applies to the borrower; however, any other aggrieved person affected by the bank’s action can appeal without submitting the 75 percent deposit.

Additionally, section 9, law states that the court can only stop the sale of the mortgaged property if: There is no mortgage agreement in place, the mortgage has been paid back, the borrower, or any other person raising this appeal, has deposited the outstanding mortgaged money to the court.

Furthermore, for banks to feel comfortable lending to low-income groups where income uncertainty exists (therefore potentially higher defaults for the banks), in November 2020, the SBP announced relaxations to incentivize banks to lend for low-income housing.

Banks were encouraged to use alternative methods to identify income sources and the creditworthiness of borrowers and exempted them from requirements of using ‘verifiable income’ in calculating the debt to burden ratio (DBR). To increase mortgage lending, banks have also been exempted from the provision of following the DBR and the Internal risk rating system for low-cost housing finance until September 30, 2022.

Read more: Steel and Cement Cartels: Risk To Prime Minister’s housing Scheme

The State Bank has also mandated that banks make mortgage financing at least 5 percent of their loan portfolio. Digitalization of land records has been started for the past couple of years. The PTI government has also encouraged this – so hopefully, many of these will become electronically available in the near future. The road is slowly being paved to make Pakistan a home owning democracy!