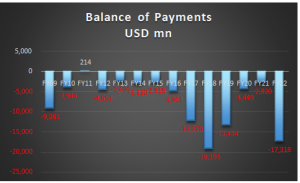

Pakistan is faced with an increasingly complex economic situation wherein the Balance of Payments crisis has spiraled out of control. The economy is fast deteriorating, with a highly devalued currency, inflationary pressure and a misplaced policy of high-interest rates creating even more cost-push inflation. This is in addition to structural issues in our import bill which need to be addressed, as well as a focus on consumptive rather than a productive use of resources. These issues can only be resolved through a government-backed strategy of sustained export growth and the development of an export culture.

The textile industry provides a reliable pathway to counter the crisis that has emerged from regressive policy measures and consecutive loans, as it comprises 66% of the country’s exports and is eager to contribute to its sustained economic growth through an influx of valuable foreign exchange. However, severe strains on liquidity and economic stability paired with the brunt of the climate crisis have stifled ease of doing business and made maintaining the current momentum of exports difficult.

Read more: Effective Energy Allocation for Export Growth

Understanding the matter better

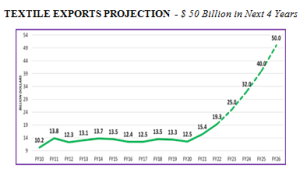

APTMA’s ambitious target of $50 billion in textile exports in the next 4 years is rooted in past success, predicated on the supply of regionally competitive energy. While the commitment of regionally competitive energy tariffs of 9 cents/kWh for electricity and $9/MMbtufor gas/RLNG for a year’s time has been an instrumental measure for exporters, the non-provision of competitive energy rates in the month of July had a major negative impact on exports which the industry is still reeling from, as confidence in policy continuity has been severely tested.

The existing capacity is not fully utilized at present, due to energy supply and quality constraints (especially gas/RLNG) over the last 6 months. This inability to effectively leverage full capacity has reduced Pakistan’s exports by approximately $800 million per month, or $10 billion per annum.

At present, competition in textiles is becoming increasingly fierce in the midst of the ongoing global recession. Inflationary pressures are increasing the price of inputs, thereby negatively impacting the competitiveness of exports. Price competitiveness and prompt delivery of quality products will therefore be increasingly instrumental in determining which countries are able to enhance or even maintain exports.

The government must explore avenues for sustainable gas supply to the export industry in order to sustain export volumes, adequate supply of energy at regionally competitive tariffs is a must, and this requires rethinking gas allocation priorities, adjustments, and a major gas conservation drive. It is of utmost importance to commit energy rates for the entire +year – if not for the full 4 years – as the current procedure whereby electricity rates are notified on a month-to-month basis is unsustainable.

Furthermore, the supply of Gas/RLNG to the exporting sectors in Punjab, hosting more than 50 percent of the total installed capacity in Pakistan, and requiring 200MMcfd gas/RLNG, must take precedence over other industries based on economic rationale. Given the quality of grid supply and the delay in the expansion of electricity connections, the supply of adequate gas/RLNG becomes critical. The government is urged to restore the priority of the exporting sector and to evaluate and ensure the best use of scarce resources for the economic stability of Pakistan.

Read more: Pakistan single window: A digital revolution

Despite the fact that our currency has depreciated by 60-70% within the last year, exports have become worth over Rs. 3 trillion, yet the working capital has not increased. In fact, 50% more working capital is needed to cover the gap created by exchange rate depreciation. The industry requires double the amount of working capital that is currently available.

The export cycle lasts up to 5-6 months wherein the liquidity of the sector remains tied up in the process of sales tax till refund (6 months). It would therefore be prudent to restore the SRO 1125 i.e., Zero Rating for the entire textile value chain in order to meet the working capital requirements. This policy measure in combination with the continuation of RCET would be essential in enabling the textile sector to continue on its journey to achieving its FY23 target of $24 billion.

For a strong export culture, imports of the export-oriented sectors must be allowed hindrance-free admission into Pakistan. In a recent circular issued by the External Relations Department of SBP, it is clearly mentioned that there are no restrictions on the import of raw materials and machinery/spare parts for export-oriented units. However, imports under Chapters 84 and 85 are restricted due to requiring prior approval for imports of export-oriented units against all economic rationality, and exporters have been unable to clear goods for up to 3-4 months. The country is resultantly suffering huge economic losses due to illogical delays in approval by SBP.

There are serious concerns over the delay in the opening of such LCs of machinery parts which are regular consumables of the textile machines essentially required to run and maintenance of textile machinery. Moreover, this allowance for imports under Chapter 84-85 only caters to direct exporters and indirect exporters are neglected which is a matter of grave concern as indirect exporters provide the intermediate goods to exporters. Further delays will severely affect maintenance and constrict the entire value chain, resulting in a production shutdown and irrecoverable export losses.

Read more: Economic growth amid political instability

Further restricting export growth is the absence of GSP+

Without this preferential status in trading with the EU, Pakistan would have to bear an MFN tariff of 12% under most traded chapters (42 and 61 to 63). For Pakistan to remain in the scheme for 10 more years, it must ratify and implement five new conventions in addition to the previous 27. Additionally, for a better approach, it must begin negotiations with the EU on tariff lines not falling under the GSP+ preferential status for the next GSP+ agreement.

The recent floods have wiped out much of our cotton crop, and the textile sector is seeking out strategies to buy cheaper cotton abroad, as it is crucial to arrange its raw materials and ancillary requirements at the lowest cost possible on an emergency basis for the sector to continue meeting the export orders.

Furthermore, there is uncertainty in Pakistan’s investment climate due to regressive policies as well as political instability – a serious impediment to economic progress. Not only does it shorten policymakers’ horizons leading to suboptimal short-term macroeconomic policies, but it is also the cause of frequent policy U-turns and leads to non-completion of ongoing projects. This scenario paired with mounting debt and continued reliance on foreign loans leaves Pakistan with a weak economy and a lack of direction.

Due to the uncertain investment climate caused by regressive policies and an unstable economic environment, any more delays or non-delivery of export orders will further worsen our Balance of Payments which is already under extreme pressure, and the industry is at high risk of losing valuable international clients. The development of a sustainable export culture has never been more critical – not only to protect our economic sovereignty but our very existence as a nation-state that is under threat in the face of this unprecedented crisis.

Written by: Shahid Sattar and Eman Ahmed

Mr. Shahid Sattar, now Executive Director & Secretary General of All Pakistan Textile Mills Association (APTMA), has previously served as Member Planning Commission of Pakistan and an advisor to the Ministry of Finance, Ministry of Petroleum, Ministry of Water & Power.

Eman Ahmed is a Research Analyst at APTMA.

The views expressed by the writers do not necessarily represent Global Village Space’s editorial policy