Shahid Sattar & Asad Abbas|

Textile exports have reached $11.35 billion in the 9MFY21 from $10.41 billion over the corresponding months of last year, showing a growth of 9.06 percent. This year, record textile exports of $16 billion-plus are expected thanks to the unprecedented Regionally Competitive Energy Tariffs (RCET) policy.

The support through energy support package was just 1.29 percent of total exports but has resulted in a substantial increase in exports and investment. This export momentum can be retained through the provision of RCET and a long-term textile policy.

These policies will put the country on track of export-led growth and Pakistan can explore the untapped export potential under China Pakistan Economic Corridor (CPEC) as China is willing to relocate its labour-intensive manufacturing to Pakistan.

To analyse the impact of RCET on exports, a study “Are Energy Subsidies Boosting Exports,” was carried out by International Growth Centre (IGC) under the directions of Ministry of Petroleum. The Petroleum division had cost concerns and wanted to understand whether RCET policy was boosting exports or not.

The report was factually incorrect and was based on a simple linear regression of the dollar value of exports compared with energy prices, which misled policymakers. Since economic analysis is only as good as the model it is based upon, the model’s focus should have been to regress the multiple variables present in real economic situations.

Any model must cater for other numerous variables impacting exports such as; relative energy price in competing countries, other comparative incentives, cost structure, and long-term stability of policies, etc.

Read More: Current RCET policy can lead to shutdown of textile industry: PIDE

Competitive energy costs

By comparison a model focused study with multiple variables presenting the real economic situation was recently published by the Pakistan Institute of Development Economics (PIDE), a government institute working under the Planning Commission of Pakistan.

The report has been compiled and peer-reviewed by renowned economists Dr. Hafiz A. Pasha, Mr. Shahid Hafeez Kardar, and Dr. Nadeem ul Haque. The report covered all the major aspects including cost structure, relative energy prices in competitive countries, value of exports, incentives and long-term stability of policies.

The key findings of the study “Regionally Competitive Energy Tariffs Textile Sector’s Competitiveness” rebutted those of the IGC report. The report showed that the leading cost component in textiles is energy, which accounts for 35-40 percent in conversion cost; as a consequence of RCET, both spinning and weaving subsectors recorded higher growth in exports than growth in local sales.

However, a reversal of this RCET policy would mean the spinning and weaving sector will become uncompetitive; downstream industry will lose international competitiveness and price rankings.

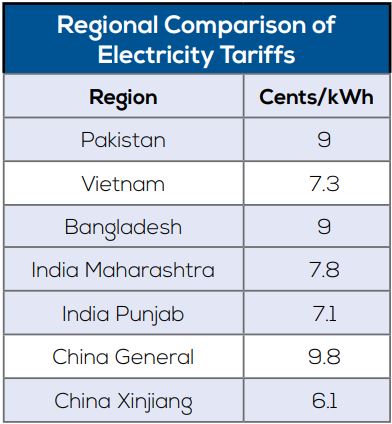

Energy tariffs in Pakistan are high due to governance issues, operational and commercial inefficiencies, lack of effective planning, flawed policies, distorted pricing strategy, irrational cross-subsidization, and most importantly sub-optimal energy mix. Moreover, the study finds that an electricity tariff above 7.5 cents / kWh is regionally uncompetitive.

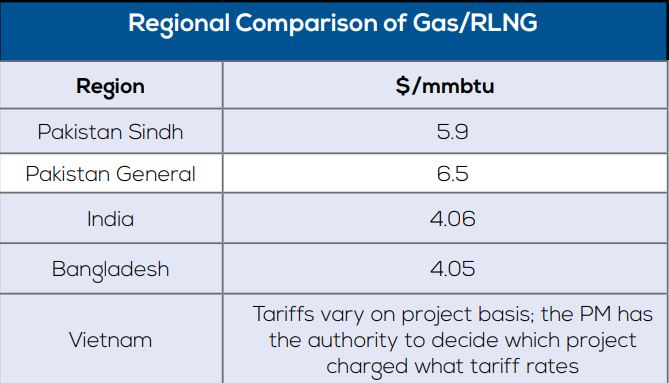

The industrial demand for providing electricity at 7.5 cents / kWh and Gas / RLNG at $6.5 / MMBtu is logical. For Pakistan’s economy to progress sustainably, it is essential that export-Led growth becomes the cornerstone of government policy and for this to happen, competitive energy costs are critical.

The table shows the detrimental position of Pakistan’s textile sector in terms of competitiveness in case of withdrawing the RCET policy. The table indicates that the average electricity price in the region is 7.4 cents /kWh.

Similarly, gas pricing showed the regionally disadvantageous position of Pakistan. The average regional tariff for gas / RLNG is around $4 / MMBtu. Pakistan’s textile sector in total cost is paying 2.4 percent more than India and 7.8 percent more than Bangladesh.

The major difference in share among Bangladesh and Pakistan could be due to the dynamics of the sector. Bangladesh operates at higher nodes of the value chain and is mostly engaged in garments that need less energy as a rule.

Snakes and ladders

The RCET is essential for the textile sector of Pakistan. Whenever the sector is poised to take off; we land on the proverbial snake and have to start from a much lower base. In line with our history of snake and ladders, it would be disastrous if the government withdraws the RCET, which has played a vital role in the current year’s export growth, employment, and new investment.

Read More: Why Regionally Competitive Energy tariffs are needed for textile sector!

This would be troubling because it will create the impression that the government has given up on the only sustainable solution of managing the balance of payments (BoP) and exchange rate. To keep textile products competitive in the international market, the availability of energy at regionally competitive tariff rates is indisputable.

The unit cost of service of power to B3 and B4 consumers is approximately Rs. 13.7 / kWh, and this includes energy purchase price, capacity purchase price, and allowed T & D Losses. However, the current NEPRA noticed that the unit price for the industry is roughly Rs 21.9 / kWh.

This is set to increase by a further Rs. 6 / kWh as reported by the press. The difference in the unit cost of service and unit price shows the cross-subsidization across sectors. Nevertheless, the unit price set by regulators tries to cover all the system’s inefficiencies and much higher than service cost for industrial users.

The first rule to export is to provide a level playing field at the domestic level as inefficiencies, as a rule, cannot be exported. Any change in energy tariffs impacts the competitiveness of products in the international market through the cost of power & fuel in conversion cost, and change in input price at spinning and weaving units across the TVC.

Protecting the local industry through RCET

Similarly, Temporary Economic Refinance Facility, which has shown significant growth over the last 12 months in approved financing, has reached Rs. 436 billion, out of which 60 percent alone came from the textile industry.

This SBP’s introduced scheme to boost the economic activity and exports, led to new employment opportunities and a sustainable balance of payment situation, have played a significant role in the overall economic situation of Pakistan.

This scheme has encouraged investment in the export-oriented textile sector that made huge investments under this scheme. Textile machinery imports showed an 8 percent growth in the first nine months of the current fiscal year indicating that the industry has started importing textile machinery as part of expansion and up-gradation in the sector.

All these achievements are a direct result of Regionally Competitive Energy Tariffs (RCET). Another proposal being considered is to offer RCET with a Drawback of Local Taxes and Levies (DLTL) package, but this is not a sustainable or implementable solution.

Only direct exporters will benefit from it, whereas 80 percent of the sector is highly fragmented with spinning, weaving, dyeing, finishing, and garments. The DLTL scheme will only help the direct exporters, and distort the rest of the market contributing 80 percent by value and 90 percent by employment.

Given the high energy tariffs, a domestic producer will not purchase from the local market while importing duty-free through duty and tax remission for exports (DTRE) schemes with far less capital. This DLTL policy, if implemented, will lead to deindustrialization and mass unemployment in the country.

Read More: APTMA warns any interference in free market mechanism will disrupt exports

Vertically integrated (big textile units) have marked systematic advantages. These textile units have access to credit, bonds & DTRE schemes, and exemption from turnover tax at multiple stages, which usually the SME sector cannot avail.

Overall, these units have an 8 percent advantage over the disaggregated SME sector, and restricting the energy subsidy to exporters will further exacerbate this market distortion. If the regionally competitive energy tariff is limited to these few companies, the rest of the textile sector will cease to be competitive.

This will lead to the closure of a substantial number of companies with an anticipated loss of over 2 million jobs within no time. Under these circumstances, the government needs to question, should the export energy tariff be restricted to direct exporters only?

Chinese FDI & GVCs: golden opportunity for Pakistan?

The government has proposed industrial cooperation under CPEC with China on various sectors, including textiles. Pakistan can capitalize on these opportunities by becoming an ideal destination for Chinese FDI and Global Value Chains (GVCs) and collaborating in joint development of raw material extraction, processing bases, and international marketing efforts.

For this to materialize, approval of the textile policy and regionally competitive energy tariffs for the next five years is absolutely essential. This indicates that the textile sector can put the country on track for export-led growth, while on the other side, withdrawal of regionally competitive energy rates will hinder the positive moves taken by the government.

Perhaps policymakers are not aware of the gains that are likely to be secured through textile export promotion and are not willing to capitalize on this opportunity unknowingly.

Through enabling environment, especially the provision of RCET, Pakistan can produce goods at a lower cost than many western countries and therefore is in a good position to explore the untapped export potential through CPEC.

Unlike many others that possess only the primary base or the finished base, a complete textile value chain exists in the country. According to a World Bank Report, CPEC can add 14 percent to the GDP of Pakistan in the next ten years. Moreover, China is willing to relocate its labor-intensive manufacturing to Pakistan.

This would help Pakistan to double its textiles in the presence of regionally competitive energy tariffs. The expansion and growth of the textile sector have been a direct result of the RCET policy.

Therefore, the unswerving execution of RCET policy is essential to remain competitive, attain sectoral expansion & modernization targets, and export-led economic growth. The only sustainable solution to Pakistan’s economic woes is export-led growth, which is only

possible with the continuation of RCET!

Mr Shahid Sattar, is the Executive Director & Secretary General of All Pakistan Textile Mills Association (APTMA), largest exporting group in the country, has previously served as Member Planning Commission of Pakistan and an advisor to the Ministry of Finance, Ministry of Petroleum, Ministry of Water & Power.

Asad Abbas Shah is a Research Economist and a professional employee with more than 3 years of working with APTMA.