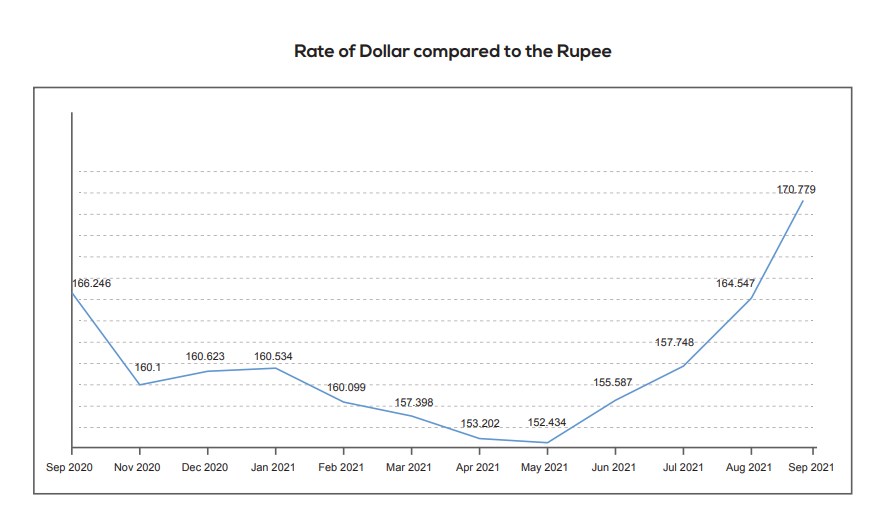

Pakistan rupee has depreciated 7.2 percent against US Dollar since June 2021 – being certainly not the only emerging economy witnessing such trend where likes of Thai Bhat, Philippine Peso or Turkish Lira also went under similar dynamics – due to strengthening of US dollar.

The dollar index is up 2 percent on account of US Fed announcing earlier than expected tapering of bond purchases and signaling commencement of interest rate hikes sooner than later. Additionally, the recent round of rupee devaluation is part of the market-determined exchange rate paradigm introduced in 2019 and a reflection of apprehensions over External accounts amidst expanding Current Account Deficit (albeit temporarily) and Afghan turmoil arbitrarily increasing demand for Dollar in the local market

Resultantly, in its recent Monetary Policy Committee meeting, the Central Bank increased the benchmark rate by 25bps to 7.25 percent, signaling further rate hikes aiming to discourage non-essential imports from bringing External accounts back in order and ease pressure on the currency. To highlight, currency devaluation exposes inflation to upside risks, being already under stress from higher commodity prices globally, where a 1 percent movement in exchange rate translates into a 30bps impact on inflation, as per studies.

However, tightening administrative price controls and subsidies on key items seems to have positive overtures in putting inflation on a decelerating path. The Current Account Deficit (CAD) for August 2021 was declared at US$1.5 billion compared to US$0.8 billion in July 2021 and a surplus of US$255 million in August 2020.

Read more: Pakistani Rupee: Best performer becomes worst performer

Cumulatively, for two months of this fiscal year, CAD stood at US$2.3 billion or annualized 4.1 percent of Gross Domestic Product (GDP) compared to US$838 million surpluses in the same period last year with trade deficit growing at a brisk pace, up 2x year-on-year to stand at US$6.8 billion.

The recent CAD release ignited concerns that at a similar pace, the deficit would well exceed Central Bank’s targeted range of 2-3 percent of GDP set for the fiscal year 2022, setting in apprehensions amongst market participants of a repeat of previous cycles of external account instability where the latest one in 2018 witnessed CAD exploding to US$19.8 billion or 6.3 per cent of GDP and sending rupee to a steep downward adjustment, down 31.7 percent one-year post-2018.

The notion of a return of 2018-like situation is unjustified where one needs to comprehend the factors that triggered those events – government of the time prioritizing short term consumption-driven growth and weak FX reserves position with import cover at 2.1 months which stands in stark contrast to swift action by authorities to contain non-essential imports and FX reserves indicating healthy import cover of 3.2x.

Saving graces

The swift action comes at a time when recent CAD release carries certain non-recurring items and positive facets in the form of Pakistan’s exports growing by 35 percent year-on-year (YoY) in two months of this fiscal year to stand at US$4.6 billion over an already high base achieved last year – 13.7 percent YoY growth was witnessed in 2021 with export proceeds at US$25.6 billion, highest in history – and remittances holding its base, +10 percent YoY to US$5.4 billion, reminiscent of the shift to official channels seen in the previous year at which time it stood at US$29.3 billion.

Pakistan’s most prominent export component, Textiles, has grown by 41.2 percent YoY to stand at US$1.3 billion, where market grapevine suggests an even more significant number as certain orders due to ship shortages were delayed.

Elaborating on non-recurring items included in import bill that grew 68 percent YoY to US$11.4 billion in two months of this fiscal year are vaccine imports that stood close to US$800 million, which were not present in the same period last year and with +10 percent of the population now completely vaccinated, the related bill should be clamped down shortly.

Read more: Pakistan’s economy moving towards growth?

Machinery imports – indicative of strong economic outlook with FY22 GDP growth targeted around 5 percent vs. 3.94 percent in FY21 – have grown 33.0 percent YoY to stand at US$1.3 billion, mainly attributable to investment in machinery under Term Economic Refinance Facility (TERF) of SBP and likely to normalize in coming months.

Moreover, the accretion in the import bill manifests increased global commodity prices with the TRJ Index, a global commodity index, accelerating 47 percent YoY, whereas FAO Food Index is up 33 percent YoY – a global phenomenon in recent times. Additionally, higher imports are also attributable to tighter border controls limiting smuggling in the country and improving prospects for local manufacturers.

The move by the authorities to curb non-essential imports such as that of transport, including autos which have grown 2.6x in the current two months owing to policy relaxations provided under Finance bill 2022, indicates achievement of sustainable growth to be the top agenda for the incumbent government as opposed to previous cycles of boom and bust.

The latest set of actions include, Central Bank increasing benchmark rate by 25bps to 7.25 percent and tightening consumer auto lending regulations while the government re-imposed duties on specific segments, even higher than in the first instance. Additionally, an increase in cash margin on imports which have been relaxed during the COVID period, is also on the cards to slow down non-essential demand.

Read more: Chairman AKD securities says economy heading in right direction

This has transpired into a confidence booster for many foreign investors, as indicated by venture capital raised by many of Pakistan startups to the tune of +US$200 million – higher than in cumulative six years ex-Daraz’s funding of US$55 million.

Importing trouble from across the western border

Lastly, Pakistan has also been most affected by developments across the western border, in Afghanistan, both at a social level and on the economic front. The recent round of devaluation has also been attributable to this factor where hefty US dollar buying in areas at close proximity to the border has put downward pressure on the rupee.

However, the Central Bank has been quick to stop illicit activity in these areas with assistance from law enforcement agencies which should have positive spillovers on currency going forward.

From the Stock market’s vantage, while currency devaluation does not bode well for most sectors amidst price controls by the local authorities, however evolving dynamics on the external front has sprung IMF back into the picture – a clear positive for macro sustainability and unlocking dollar inflows with the authorities now contemplating to meet prior actions.

Read more: The worst is over for Pakistan’s economy: AKD Securities CEO Muhammad Farid Alam

The current P/E of 5.5x compared to the historical avg. P/E of 7.5x has priced-in risks to earnings outlook, keeping downside limited with investor confidence improving on Pakistan’s economic fundamentals as opposed to previous regimes where economic numbers were artificially influenced for political gains putting long-term fundamentals at risks.

Hamza Kamal is Economic and Financial Analyst with AKD Securities, leading Brokerage firm in Pakistan.

The views expressed in the article are the author’s own and do not necessarily reflect the editorial policy of Global Village Space.